Disclaimer: This is not a recommendation to Buy/Sell/Hold. This is just for the sake of discussion here. I am posting my own analysis and views here to initiate a discussion. Needless to say, I could be wrong.

MT Educare, is one of the largest coaching institutes in India. It is an undisputed market leader in the Mumbai market and is slowly expanding into adjacent markets of Maharashtra, Karnataka & Andhra Pradesh in an asset light model. It provides coaching for Science, commerce, Engineering entrances, CA and MBA entrances. The company has 128 coaching locations in 7 states and has serviced ~ 82,000 students in the FY gone by.

Coaching business has strong economics and MT Educare has executed very well in the Mumbai market. This expansion in Mumbai is driven largely through standardizing its teaching methodology and not on ‘Star teacher’ concept. The sector in general has not seen many scaled up players owing to lack of standardization and low entry barriers leading to local players becoming leaders in their respective markets.

MT’s strategy of slowly expanding outside Mumbai is an interesting one in our view, they have executed well in Karnataka with revenues reaching ~10% of the overall pie in two years. Further they have walked their talk on selling their PuC college in Mangalore which they had bought to establish credibility in the market.

In our view the approach (asset-light, variable cost model) taken by MT to expand in new markets is a low risk high reward model. Company has recently also expanded in Andhra Pradesh in this similar fashion by partnering with an educational institute which has around ~35K students under various PuC colleges.

The business has an attractive profile with strong pricing power, improving profit margins and negative working capital. All these points coupled with the positive management feedback through scuttlebutt and initial success in Karnataka give us comfort that MT can expand beyond its ‘home-turf’.

We like MT Educare because of the following reasons:

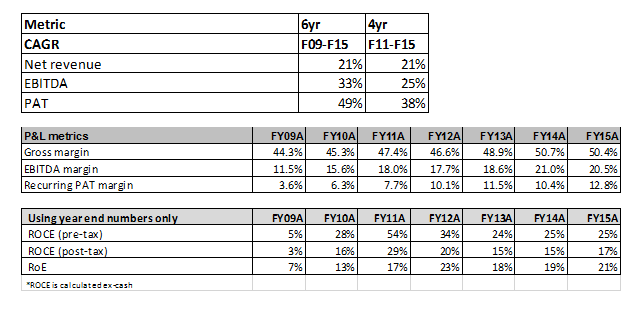

Strong position in Mumbai- MT Educare started in 1988 with a single class has expanded to ~ 90 centres in Mumbai in 2014-15. This is noteworthy, especially, given the scalability issues in coaching market. Other dominant local players such as Sinhal, Kalra Shukla, and Thakkar Classes haven’t been able to scale up as much as MT has. The brand MT is extremely strong in Mumbai with huge network advantages through coaching centres across length and breadth of the city. This is very difficult to replicate for a competitor. We believe that the company will continue to hold its market position in the Mumbai market. The company also has strong pricing power, evidenced by strong increase in ARPU/student of 15% CAGR over the last 5 years (FY10-FY15). We attribute the strong position in Mumbai market to successful execution by the MT team. The school segment is highly fragmented and largely an unorganized market. MT has used a standardized approach for delivery and has used extensive teacher training to reduce reliance on key/star teachers. This hasn’t been the case for competition which has affected their scalability

Strong financial performance – MT Educare has demonstrated strong growth in both top-line and bottom-line. It has grown its revenues and PAT at a CAGR of 24% and 37% over FY11-FY14. Company has generated >20% return ratios over the last 4 years. The company also works on a negative working capital model with students paying fees in advance. As utilizations levels has improved at its various centres its operating profit margins (EBITDA) have also increased from 11.5% in FY09 to 20.5% in FY15.

Expansion in adjacent markets in an asset light model- MT is looking to slowly expand into Karnataka, Andhra Pradesh and other regions in Maharashtra. After its successful expansion in Karnataka through the asset-light model, the company has further used a similar model in A.P through its partnership with Sri Gayatri Education Society (SGES). In addition to being asset light, the model is also variable cost driven with PU colleges taking a share of the revenues. This will limit losses on fixed costs such as rent etc for MT as it expands in new geography. We believe that a large part of the future growth for MT would come from non-Mumbai markets. Below is a brief on the model adopted by MT in each market

- Karnataka: The company first expanded in Karnataka in 2012 through its own PUC college. The company subsequently expanded in this market by partnering with existing PUC for premises. The company in FY 15 sold its college premises as they feel they have now got a foot hold in the market. Partnering with PUC college is an asset light model and completely on variable cost as MT doesn’t own any asset and only pays a share of the revenues in lieu of the premises. The company has 14 tie ups in Karnataka and plans to reach 30 colleges by FY18. Karnataka at the moment contributes ~ 10% of revenues for MT

-

Andhra Pradesh*: MT has recently partnered with Sri Gayatri Eemphasized textducation Society (SGES), which has 35,000+ students in its junior colleges. Under this partnership, MT would provide coaching to the students under SGES. MT would provide coaching for 4 courses. This is again an asset light model wherein MT hasn’t done any investments in real estate and would share a portion of the revenue with SGES. SGES in return will provide real estate and a captive audience for MT

-Other markets: MT through its acquisitions of Lakshya has presence in Punjab & Haryana. Further, MT is looking to leverage this brand by expanding in its other established markets viz- Mumbai, Karnataka. It plans to leverage its strong brand in Mumbai in other parts of Maharashtra. It has also made TN a hub for CA coaching centre

Risks

-

Unsuccessful expansion in non- Mumbai market- We believe that a large part of the future growth for MT will come from its expansion into non-Mumbai market. If the company is unable to successfully expand in these markets, growth will be a challenge. Coaching in general is a highly fragmented, localized market with many local leaders in each city/region. Further, MT/Mahesh brand is still largely a new name in its new regions such as Karnataka & A.P and thus may find difficult to compete with established players. In the event of no/low growth from these new markets, MT could become a value trap

Regulatory issues – Any changes in the regulations may impact the company negatively. For example, CBSE has made board exams optional for 10th standard students. Further many competitive examinations have undergone change in pattern for e.g.- In 2012 IIT JEE exam under-went a major shift from a paper pencil model to an online model and competitive exams frequently see a change in pattern and are also moving to an online model

Concentration risk in Mumbai- Mumbai contributes 80% of the revenues and 66% of the centres are in Mumbai. Any change in exam patter or any adverse regulation against coaching institutes in Mumbai/Maharashtra can adversely impact MT. - Threat from online test prep players – With many competitive exams such as CAT, IIT-JEE etc. moving online, there has been a surge of online test-prep players over the last 2-3 years. As students become more adept with technology and with increase in mobile and internet penetration, online only players could pose a threat to offline players such as MT. MT with its ‘Robomate’ offering is trying to counter this threat by offering its digital solution on mobiles and tablets to MT & non MT students. It has tied up with local coaching classes in Tier 3 & Tier 4 towns in Maharashtra & Gujarat for sale of Robomate. In FY15 Robomate did revenues of ~ INR 3 Crs

Valuation & Upside

As mentioned above in the note, MT Educare has an attractive business profile with expanding margins, negative working capital, high return ratios and pricing power. The business is facing growth challenges as it looks to expand beyond its core market of Mumbai. We believe that the strategy adopted by the company is both scalable and economically prudent.

Company is currently trading at P/E of ~15-16 and an EV/EBITDA of 8.5

If the thesis of expansion outside Mumbai plays out well, we expect the company to increase its revenues and earnings at a CAGR of 25% over the next 3-4 years. In the event of that happening, we feel the business will also get re-rated as it will allay the investors’ fear of being a non-scalable business. A business with such a profile (High ROCE, negative working capital etc) and similar growth (>20%) should command an earnings multiple of greater than 20X (P/E)

Revenue Mix

About the Industry

Market size & Growth drivers – Non -School education is a large market in India. According to CRISIL estimates, the Indian coaching industry is expected to clock 17% CAGR (over FY2011-15E) from 40,187cr to 75,629cr. Bottom up estimates also suggest that IIT JEE & Medical test prep itself is a 5,000 crore industry. This market would continue to grow driven primarily by rising disposable incomes, increasing household spend on education and higher private sector participation.

Competition – Coaching Industry in India is a highly competitive market. With low entry barriers the market is highly fragmented with very limited pan India players. Some of the key players in the coaching/test prep market are outlined below:

Key Metrics to track

- Volume & value growth in Mumbai & non Mumbai markets

- Revenue contribution from non Mumbai markets

- ARPU & EBITDA per student

- Attrition of teachers

- Revenue from Robomate and Lakshya

You can read the same here : MT Educare: A play on For Profit Education in India | Armchair Investing

Disclaimer: This is not a recommendation to Buy/Sell/Hold. Safe to assume I have vested interest in the company as I am a shareholder in the company.

Registration Status with SEBI:

I am not registered with SEBI under SEBI (Research Analysts) Regulations, 2014. As per the clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”