Post Concall – My Understanding & Personal View :

Mag+ :

Whereas management preferred not to disclose any sort of financial details of Mag+, we got two confirmations from the management side with this regards :

(1) Mag+ had 20 employees.

(2) Bonnier has so far invested 20 mn. USD in Mag+.

Now, based on these two confirmations, the numbers we have from Mag+ AB Annual Report seem more or less correct and the actual numbers might not be much different than that. This is because :

(1) In Annual Report, employee strength of 18 is already mentioned.

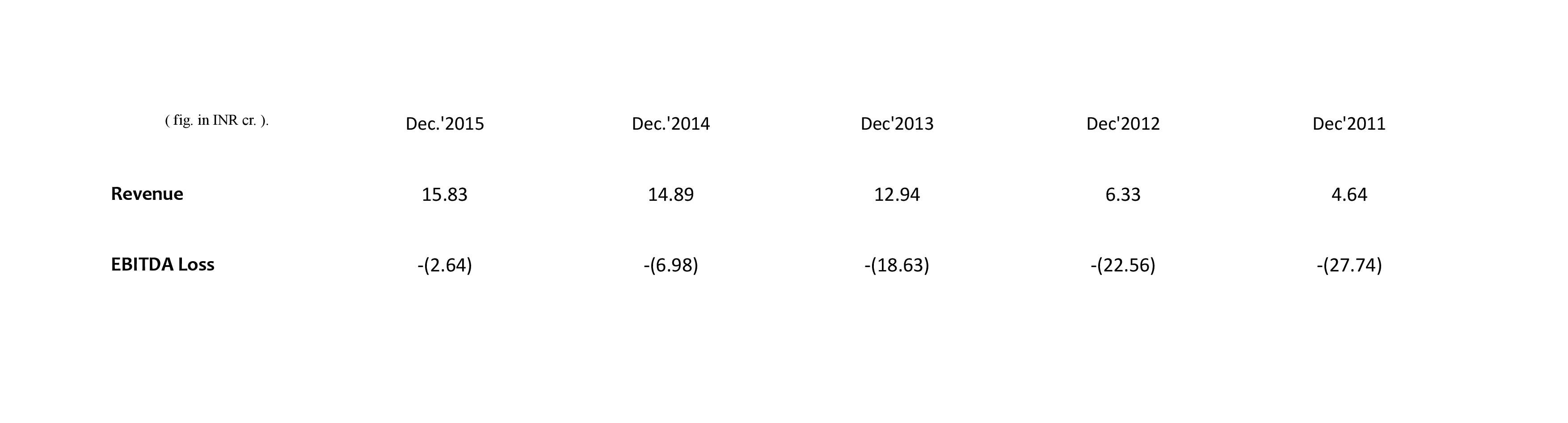

(2) If we add the EBITDA losses posted by Mag+ since inception uptill now, they add up to ~15 mn. USD which again matches with the said 20 mn. investment of Bonnier in Mag+.

So, final updated INR converted (w.r.t. currency conversion rate SEK-INR of the respective year) Mag+ numbers since inception uptill CY15 (only one missing quarter of FY16 of MPS) are as stated below :

Regarding the point that MPS acquired only some parts of Mag+ — it seems quite impossible as far as Mag+ core business goes as its not a services business where you acquire some practices/centres and leave others…If we refer press release of MPS, and also refer Mag+ CEO’s communication in respective company’s blog, it is quite obvious that entire IPs/products are acquired by MPS. Yes, there could be some hard assets involved which Bonnier might have kept with itself or likes but otherwise this seems highly impossible. The numbers we have seems to be of core business of Mag+ where personnel costs account for ~76 % of the costs involved and employee count is already confirmed by the MPS management.

Few things require attention with regards to this acquisition :

– With MPS acquisition from Macmillan in FY12 for a consideration of INR ~45 cr., the company got a readymade revenue stream (of 32 mn. USD) and it had to turn it around and improve on margins which went into negative over a five year period before acquisition. 5 Years before acquisition by Mr. Arora, MPS was already consistently operating at average 40 % PBT margin under Macmillan.

– With Mag+, what MPS has got is – for a consideration of almost half the amount paid for MPS acquisition (INR 23.7 cr.), company has got a revenue more than 10 times less than that of MPS (at the time of acquisition from Macmillan) with no trackrecord of profitability.

– Another key difference is – when MPS was acquired by Mr. Arora, he was in a dominant position to take every decision as he understood the business exceptionally well because of his previous ventures (International Typesetting & Composition as well as ADI BPO). MPS was in the same field in which Mr. Arora had experience of more than one decade and he dealt with similar clients over these many years. To add, business model was also same.

– With Mag+, it is Staffan Ekholm (the CEO of Mag+) who will call the shots and Mr. Nishith Arora’s role might be more of an advisor, mentor and facilitator. Majority of the client profile is completely different as also the field and business model and therefore the market understanding seems different. Mag+ focus is corporates and its target field is internal communication of corporates.

– Hence, with MPS, Mr. Arora was able to take the risk of cutting costs even by taking drastic steps such as completely putting to an end the existing sales channel of MPS at that time in Europe since he had good access to the key clientle and was a known figure amongst them. With Mag+, such drastic steps are impossible as otherwise they could severely backfire.

– Mag+ revenue needs to be built in order to turn it around and make it a robust profit-making entity ; and revenue-building needs investment, significant investment in Marketing & Support– a thing MPS has lacked so far. It is also not that MPS has such clients which offer a direct cross-selling opportunity for Mag+ — both’s clientle as also offering profile itself is quite different with Mag+ 65 % clientle being corporate entities who might not have anything to do with academic/educational publishing and MPS’s majority of clientle being academic/educational publishers who might not have anything to do with Mag+ offerings.

– Also, existing marketing personnel of MPS in NA might not be well equipped to effectively sell Mag+ offerings as majority of them come from educational publishing background with the experience to handle publishers.

– Hence, this is a reverse situation, wherein, after acquiring MPS in FY12 for 45 cr., management had to cut costs and resort to asset sale and all to make it profitable (and this it was able to do so even after haircut suffered in topline ; – post acquisition, MPS revenue declined by 7 %) whereas with Mag+, after acquiring it for 23.7 cr., management might have to incur further expenses to make it profitable and this it has to do by ensuring that it doesn’t suffer a haircut in topline right from the beginning.

– Management is right in its saying that Bonnier has so far invested almost 20 mn. USD in building Mag+, then, the question arises asto why Mag+ was sold in totality to MPS for ~3.5 mn. USD – its not that Mag+ didn’t fit its previous parent’s strategy and was non-core to it as Bonnier Growth Media is actually a VC arm of Bonnier and even today it is investing actively in many high potential ventures. Also, Bonnier was in no need of meagre ~3.5 mn. USD also as its a cash-rich entity.

– Then, why Bonnier incurred this significant loss on its investment if, by just tweaking of slight strategy (by appointing VARs, as is said), and without significant further investment, Mag+ can be made successful into a robust profit-making entity ?? Why Bonnier even didn’t keep a minority stake to ensure that its significant investment gets paid back to a certain extent (although such minority stake might not have appealed MPS as its not Mr. Arora’s style of acquisition) ??

– Is Bonnier unwise enough to let go a venture which is on verge of turning profitable within 1 year and in which it has invested 20 mn. USD over last 5 years just as it is, by getting just ~3.5 mn. USD ?? Even Macmillan had enjoyed hefty dividends (and therefore cash generated) by MPS over more than 10 year period so the sell-off to Mr. Arora was just exit from a business for additional 45 cr…

I am just putting here the valid questions that are arising as its impossible to digest the saying that without any further significant investment, Mag+ could become a growing profitable entity.

Having said all these, I must admit that Mag+, prima-facie, seems to be the most interesting acquisition done by MPS so far with a great future prospect but if there is reluctance to invest significant further amount in the entity, it might very well go MPS Technologies way. Remember, MPS Technologies was one of the most innovative and high potential entity when it was launched but it somehow lost its way in the middle and never got its deserved success because of relatively more focus on services as also not able to capitalise on first-mover advantage it had.

Dividend Policy Change :

In my 22nd January 2016 post in this thread, in reply to a fellow member, I quoted following :

“Generous dividend policy till today was the need of the promoter as they wanted to repay external debt worth 25 cr. and payback themselves 26.4 cr. they spent from their own pockets for MPS acquisition as well as make return on that amount…all that is done… and a good manager like Mr. Nishith Arora might be the first one to curtail this generous dividend policy in case he makes a loss making acquisition or debt-laden acquisition (even he is on record saying this on concall).”

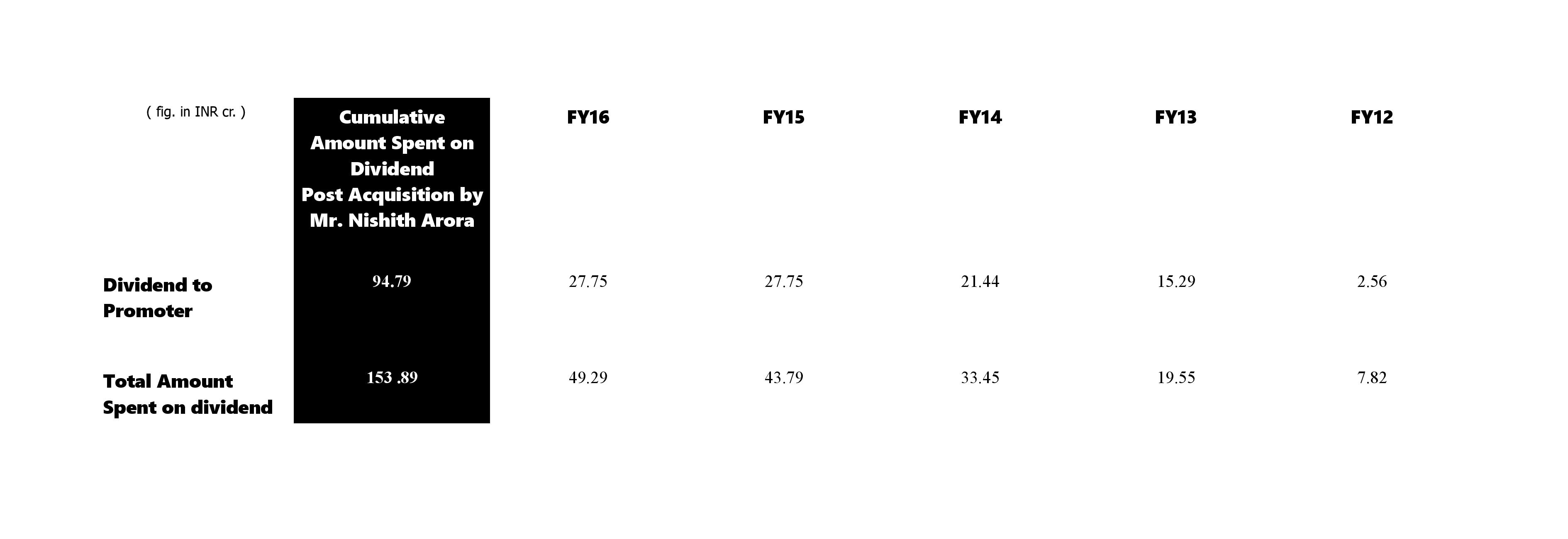

Hence, the change in dividend policy was anticipated – the latest updated statistics on dividend (till FY16) in follow-up to my old posts are :

Total Amount spent by the company on Dividend payment post acquisition by Mr. Arora, including dividend tax) = 153.89 cr.

Promoters’ got total Dividend = 94.79 cr.

Government got Tax on Total Dividend Paid = 23.79 cr.

Minority Shareholder i.e. all of us, got total Dividend = 35.31 cr.

So, for a payment of 35.31 cr., we got a equity dilution of 10 % worth ~150 cr…

For a payment of 113.14 cr. (94.79 cr. as dividend + 18.35 cr. as salaries, rents, etc.,) promoters enabled an equity dilution worth 150 cr…

Who got a better deal ??

Promoters spent 45 cr. for acquiring MPS (50 % via external debt and 50 % via internal funds), so, a payback of 90 cr. – the double the amount they spent – is reasonable and so, it was widely anticipated, atleast by me, that dividend payment will be curtailed from now on. However, the straight effect of this will be on dividend yield of the stock.

Secondly, such dividend policy change has to be short-term and not long-term (unless management can consistently generate compensatory high ROCE) ; otherwise if it is for need of consistent further investment or if the cash is burnt (unintentionally ofcourse) in any way then it will be gross injustice done to minority long term shareholders wherein in the best cash generating period, promoters’ took maximum cash out of the company, then diluted equity and then because of persistent investment in business, cash distribution is curtailed. This is only a fear and with the way Mr. Arora had handled the company affairs post acquisition of MPS, this scenario is highly unlikely.

Likely Big Acquisition & post-acquisition Consolidated Margins :

Current Q2FY17 or Q3FY17-beginning might very well see the much awaited big acquisition finally taking place. This is because, current Q2 might very well prove to be one of the toughest quarter as far as organic growth goes. The reasons for this are :

– GBP has already depreciated by 12 % against INR this quarter if we take the base of average GBP of Q2FY16.

– USD has appreciated by only 2.5 % against INR over Q2FY16 and

– Europe’s 40 %+ contribution doesn’t augur well for the company.

– Also, dividend is curtailed and part of the bangalore asset is sold-off.

– To add, CEO is now putting a firm INR revenue figure of INR 400 cr. to achieve in coming two to three years.

– Lastly, Mag+ details are not disclosed with a promise to disclose them in October’16 (as it was actually not much to disclose in past financials of Mag+ which could have worked in a positive way for the company and it would be logical to club the figures of to-be-acquired entity and then disclose the combined numbers).

– Mag+ acquisition expense as also Mag+ operation loss might start hitting from Q2FY17 onwards. (although it might very well be taken care of at net level by exceptional gain from property sale).

All these point to the big acquisition finally taking place in next few months. However, I see that many are building expectations of 40 % EBITDA margins on a 400 cr. scale. I will also point out here that it is actually the MPS management which has given breeding ground to such expectations while stating that they want to optimise margins even from here on and have enough levers left.We need to be realistic in our assessment and think logical amidst all these hoo-ha.

– A company with a revenue of 100 cr. + which is operating at 20 % + margins and is not having significant debt on its books will never sell out so cheap at the level Mr. Arora might be comfortable with, evenif such company is not able to grow as a standalone entity. A normal minimum EV/EBITDA for such deal will be 9-10x provided growth scenario is as it seems currently for the industry.

– With Mr. Arora’s style of acquisitions, a 100 cr. + company which is facing growth and margin issues both might only get acquired.

– Even a company which has the visibility of operating at 8-10 % EBITDA with a (-1)-(-5) % p.a. topline degrowth and has certain debt on its books might only sell out at minimum 8x EV/EBITDA.

In first case, which is the best case of 20 % EBITDA margins with no significant debt, MPS will have to shell out minimum 180 cr. for acquiring the entity and still EBITDA margins of consolidated entity will come down to 29 % (assuming FY16 EBITDA margin level for existing business of MPS with no growth, 15 cr. topline contribution from Mag+ with 1 cr. loss and 20 cr. EBITDA of newly acquired entity).

In second case, which could be more realistic case of 8-10 % EBITDA margin with negative growth visibility and a certain debt on books (say 10 cr.), MPS will have to shell out minimum 80 cr. (70 cr. cash to sellers and 10 cr. debt repayment) for acquiring the entity and EBITDA margins of consolidated entity will come down to 26 % with likely cut in future topline or stagnant growth. (same assumptions as done in previous case except acquired entity’s 10 cr. EBITDA).

Here we have not considered any entity which is operating at 30 %+ EBITDA (as excpet few, all larger players are operating at sub-25 % if not at loss or single digit EBITDA) as also not considered any loss-making entity (which actually might be the case). Hence, we have considered here two best possible scenarios and still EBITDA margins of consolidated entity comes down to 26-29 %. Ofcourse, it could be possible that cost cutting exercises are undertaken and margins are improved of the acquired entity, but, realistically speaking, in the present sluggish industry scenario, it is highly unlikely that at closer to 400 cr. scale, MPS will keep operating at 30 % + margins even after all measures.

Also, I notice here that many are calculating P/E or EPS based on reported PAT numbers — if one needs to arrive at core business EPS, one has to deduct ‘Other Income’ from PBT and then apply tax rate of that year and arrive at PAT and then calculate EPS…Consolidated Core Business EPS for MPS in FY16 stands at INR 33.1 and even in the best possible above considered scenario (of 29 % EBITDA on 372 cr. topline), it comes to INR 39.4.

Concluding Remark :

In the same reply I cited above (in dividend section) to one of the fellow member on Jan’22 2016, I also quoted following thing :

_“Till today the major factors supporting MPS valuations were : _

– 1-- excellent turnaround made possible within a short time which signified Mr. Arora’s managerial strengths,

–2-- Sustenance of high 35 % + EBITDA margins,

–3-- Generous dividend policy which when combined with robust cash generation could do wonders for minority shareholders.

Without these factors, there is no reason for MPS to trade at par and even on some multiples richer valuations than IT biggies like Infosys.”

The third pillar of the story i.e., ‘Generous Dividend’ payment seems to be shaking and if any of the other two pillars gets broken, the story stands a chance of breaking down. If proper support is not given in the form of great acquisition, story stands a chance of meeting an anticlimax. Don’t take me wrong in my saying as even I want this story to reach its deserved destination but there are few questions that continuously bother my mind :

– Why management is so reluctant to admit that there is problem in organic growth and is going to the extent of brushing aside most valid basic concerns too — “brexit and currency movement will not have any impact on the company” — with this saying of the management in concall, what should investors interpret :

-

is the demand scenario so strong in the industry that come what may it will not have any impact on the company then why other players in publishing outsourcing industry are facing pressure ??

-

or is it that company’s positioning in the industry is so strong that it will not impact the company even when most of the other Indian IT and other segment companies who are exposed to Europe are so apprehensive about ??

-

A company with 45 % exposure to Europe (as at FY16) is not feeling or is not fearing any likely impact of circumstances which have made UK’s currency fall 8 % QoQ and 12 % YoY even when the company itself has 27 % of its billing done in that currency ??

– If demand scenario is so powerful or company’s positioning in the industry is so powerful then why since last two fiscals, in company’s previously talked about largest quarter (Q3), management had to give the excuses like – first time – “base of last quarter was higher so we are seeing muted growth” and – second time, “the business has shifted to Q4”.

– Why even simple addition is not working wherein three companies were acquired which had combined topline of 8.7 mn. USD before acquisition (Element = USD 3.5 mn., EPS = USD 2.2 mn. TSI = USD 3.0 mn.) and still we have a shortfall of USD 1.6 mn. as at FY16 (MPS topline in FY11 before acquisition = USD 32.0 mn. + USD 8.7 mn. of acquired entities = USD 40.7 mn. ; MPS FY16 actual topline = USD 39.1 mn. with one acquired entiy having completed 3 fiscals, second acquired entity having completed 2 fiscals and third acquired entity having completed 1 fiscal under MPS).

– Will the shocks in case of this company come with a prior warning like we had with many companies like KPIT, Infosys, etc. or is it that no guidance is given so whatever end-result comes is acceptable under norms. A 6.4 % cc standalone degrowth for the first time in last 3 fiscals and a 2.4 % cc consolidated degrowth for the first time since MPS started acquiring companies under Mr. Arora came without any warning (in Q1FY17) and infact is presented in the presentation by disappearance of USD figure of revenue which was otherwise provided in all presentations done post QIP-- is it the correct practice ?? Why investors are not given opportunity to see converted $ figures in a quarter when consolidated degrowth has happened whereas for each of the previous occasion when addition theory was working (with results having presence of newly acquired entity TSI), converted consolidated $ figures were provided (instead of separate standalone and consolidated $ figures even at that time) ??

– With dividend payment most likely to be curtailed and simple addition theory also not working on inorganic route traversed so far, am I not betting too much on only one man, Mr. Arora’s, talent ??

– I am betting on Mr. Arora by looking at the history of the way he acquired MPS and turned it around exceptionally well, but when all the other acquisitions done post MPS by Mr. Arora himself are showing muted performance and Macros seem to be extremely difficult for the company, if the much awaited big acquired entity is a USA-based services entity (in the similar space as MPS) which is loss-making and there also addition theory doesn’t work as also significant margin improvement theory doesn’t work, what will happen ?? Is entire investment thesis on only inorganic growth (and that too falling inorganic growth where 1+1 is not equal to 2 but is equal to 1.6-1.7) is correct ??

– Should I turn a blind eye to the fact that post acquisition of MPS, Mr. Arora acquired companies carrying 27.2 % of the topline of standalone MPS and even after 3 complete fiscals, forget the topline growth but the EBITDA margin performance of MPS NA (under which all the acquired entities reside) has been Loss in first fiscal -FY14, 21.73 % in second fiscal-FY15 (in FY15 a company which was carrying 18.3 % PBT margin before acquisition was acquired) and 4.52 % in FY16.

– What if the acquisition is in unrelated area like, in one specific question on Q3FY16 concall, management replied that they are looking at only Academic/Educational Publishing segment for evaluating acquisition opportunities, but, we have had acquisition which is not related to academic/educational publishing ?? No doubt Mag+ acquisition is an interesting one but is it a play on the strengths of Mr. Arora on whom I am betting on ??

– If there are opportunistic acquisitions which are in allied areas where Mr. Arora doesn’t have experience or strength, are we betting on PE-, VC- type story ??

– What if tomorrow because of one big acquisition, company loses net cash status in anyway (as is indicated in AGM feedback), even for short-term ??

– If inorganic growth is the only story left and, in all probability, we are likely to see consolidated EBITDA margins post acquisitions settling at where Indian IT-majors are working on and majority of the cash on BS getting used up for acquisitions, does the company working at miniscule scale compared to IT majors and exhibiting relatively inferior organic growth with leftover cash on BS, if measured w.r.t. Operating scale (even post acquisitions) at relatively miniscule levels post acquisitions and the current cash-level (of 180 odd cr.) only likely to build-up over atleast minimum three year period post all the acquisitions in absence of equity dilution (provided consolidated entity works consistently at 30 % EBITDA for three years), is the company justified in trading at the multiples assigned to IT majors and even at a premium to some of the IT majors ??

Here, this recent 21 July 2016 report by Emkay is a must read…

http://www.emkayglobal.com/Uploads/EmkayResearch/IT%20Services%20Sector%20Update_210716.pdf

Although I don’t give much credence to any brokerage report, but, we can’t deny the fact that Q1FY17 has been one of the first quarter where we have seen a generalised trend wherein almost all the IT companies (barring couple odd), whether big or small, facing pressure on both cc topline and margin growth. This is the same quarter where we have seen MPS exhibiting one of its historically highest cc degrowth.

– Now, if there is such deterioration in fundamentals of IT majors, can the company remain immune even after resorting to inorganic growth ??

– If there is such said valuation correction in IT majors as well as Tier-II IT companies, can the company remain immune with now dividend yield also likely to fall inline with IT majors as also cash levels on BS likely to be considerably reduced relative to IT majors ??

If one refers my posts in this thread, I have been consistently stating that absence of organic growth is a concern for this company and it has to start somewhere to let this story reach its deserved destination. However, Q1FY17 has seen one of the biggest organic degrowth as also consolidated degrowth in the history of the company. Although one quarter performance should not be taken as the direction and I concur with management in its saying that we need to check for YoY performance for the entire year. But, if that is going to mean that we again bring into work addition theory wherein Mag+ will add 15-20 cr., another big acquisition will add 100 odd cr. and then we say for the fiscal we have grown by 40-50 % YoY and you only look at consolidated results and not standalone numbers, this is a dangerous game wherein on one wrong step, entire calculation will fail one day. That one wrong step if comes with a warning sign like company losing its debt-free status (even for the short term) coupled with consolidated EBITDA margin fall to 25-28 % levels then it will be great for shareholders ; but, if it comes without any warning sign then its not good atall for investors.

There is difference between good oratorship and a real robust financials/story that every investor needs to understand. Whereas a good orator can, for the short-term, make the audience turn a blind eye towards apparent negatives, finally, the numbers need to catch-up otherwise such negatives will make their appearance with a pronounced effect. A management which frankly accepts the facts without worrying about its impact on its company’s share price makes shareholders far richer in the long run than managements who just say nothing will have impact on our business and margins (eventhough it is evident that they are unable to grow and infact are showing relative degrowth v/s others muted growth in the same quarter) and also indirectly make everyone believe that even at double the scale they will try to work on similar margins…in such companies, when shocks come, investors will never be prepared for that…one wrong step from the management and complete wealth of shareholders gets depreciated

Pardon me for my blunt writeup. If management would have accepted certain apparent facts then I would have not been this much harsh in my understanding. Brexit a non-event for the company, significant GBP depreciation no worry despite 27 % billing done in that currency, 45 % Europe business not a concern, a platform/product based acquisition with no common client profile unlikely to require significant investment to turn it profitable, Q1 cc degrowth, both at standalone and consolidated level, not a concern despite last year’s muted standalone growth with haircut in acquired entities, etc. seem good but seem too good to be true.

Having said all these, let me admit frankly that if MPS can enable a good big acquisition and make the consolidated entity work at even 30 % EBITDA margin consistently without having much suffering on consolidated topline, with no debt on books and WC cycle remaining as it is then it might become one of the only few companies to do so and therefore might deserve rich multiples. However, whereas I thoroughly enjoy watching Super-Hero Movies but my mind is not that great enough to let me believe that Super-Heroic stunts shown in the movie will have no impact on me if I attempt them.

I am talking these in general and not regarding any specific company as I hope and I am sure MPS will repeat its glory as it had done post change of management in FY12 and Mag+ acquisition is a real high-potential acquisition which if handled well can do good to the company.

Discl. - Negligible Holding

Note – This is part of a general discussion with presentation of facts and statistics as is available publicly via varied sources. This is not a Buy/Sell/Hold recommendation and should not be considered in that way by anyone reading this.