MPS acquires Magplus

3 Likes

No financial details provided yet…??

Here’s an article on this in vccircle http://techcircle.vccircle.com/2016/07/02/mps-buys-digital-platform-magplus-to-boost-mobile-publishing-play/

Looks like a cheeky acquisition but nothing transformational…(Mag+ has est.revenues of ~$3-5mn)

Will wait for more commentaries from the management…

Some excerpts of Mag+ as a product…

-

Mag+ is considered a direct competitor to Adobe DPS, as it is one of the few products that does not optimize PDF files for digital editions but rather uses the solution to create specialized files for digital editions or mobile apps.

-

In addition, the entirety of the Mag+ platform is 100% in the cloud, using a SaaS based business model. Mag+’s customer base is in enterprises that are using the solution to publish nonconsumer based mobile apps that are available in Google or Apple app stores, or via internal company portals.

-

Mag+ also allows has robust analytics capabilities, e-commerce capabilities, and support rich media. One challenge to Mag+’s growth is its geographic reach; the solution is mostly known in North America and lacks the channels in other countries that would allow for increased expansion and user awareness.

-

The Mag+ payment model is based on monthly payments. The basic model is a fee of $500 per issue on a monthly contract. The customer can choose to host the data themselves or pay an additional fee for Mag+ to do this. Mag+ hosts the content on Amazons servers and 250GB worth of customer downloads is included in the monthly fee. Above that, Mag+ charges the customer $0,17 per GB of customer downloads. Hence the cost depends on which type of content is included in the issue. In the $0,17 per GB charge, Mag+ have added 10% to the amount Amazon charges.

-

The possibility for customers to handle their own hosting differs Mag+ from Adobe which does not allow the customers to opt out of Adobe’s hosting service.

Mag+ as a product

Mag+ mobile development application:

Regards

Sreekanth

4 Likes

If one goes through the past two years ARs and quarterly concalls, one notices that the company has been putting lot of emphasis on the technology platforms like Digicore and its allied tools. Magplus acquisition seems to be a step in that direction. As per Owler, the company has revenue of USD 2.70 million and around 46 employees (https://www.owler.com/iaApp/166306/mag--company-profile?onBoardingComplete=true). The company’s website is pretty interactive and gives lot of information about the company. It basically has two tools:

-

Disignd: It is a digital publishing software and covers every part of the e-publishing process. One can use Disignd using Adobe InDesign plug-in and build own mobile app. The key applications of the toll is in digital magazines, catalogues, brochures and corporate communication. It also offers other features like analytics, push notifications, web export etc. They have different payment structures ranging from one time fees to monthly subscription fees as given in the link - https://www.magplus.com/designd/pricing/. Came across an interesting article which says that they compete with Adobe and instead of charging fixed pay per download, they charge a subscription fees (link - http://www.mequoda.com/articles/digital-magazine-publishing/top-digital-magazine-publishing-software/). A look at the clients of the customers (https://www.magplus.com/designd/clients/) reveals that most of the them are corporates and not publishing houses.

-

Semble: It was just launched in November, 2015. Semble is a tool used to design mobile apps. The demo on their website - https://www.magplus.com/semble/, gives a good view about how to create your own app. The app tool is free for download. However, they do charge for branded app development - https://www.magplus.com/semble/pricing/.

Magplus website is pretty seamless and gives lot of case studies about its client base as well as videos about its applications. For MPS, it gives them an entry into new areas of corporate publishing and brochure development where they don’t have a significant presence currently. Would be interesting to hear about the management’s view on the acquisition.

11 Likes

Another usefull info

-In 2009, Bonnier’s Research and Development unit starts a project to investigate how tablets will change the magazine industry. - In April 2010, Popular Science iPad App, created by the project team, is presented by Steve Jobs on stage during the launch of iOS 4 and the company is starting to offer it’s software.

-

In January 2011, the company Moving Media+ AB is formally founded. - In september 2011, the company changes name to Mag+ AB in Sweden and to Magplus Inc in the US. The name Mag+ has since the start been used for their software. The name Mag+ originate from Magazine and the + character represents an enhanced magazine experience enabled by the interactive multi media possibilities that tablets and smartphones offers compared to print media.

-

In september 2012, 600 iOS apps has been built on the Mag+ platform.

-

In march 2013, 1000 apps has been built on the Mag+ platform. Among the clients are:

Bloomberg Markets - British Journal of Photography - Chicago Sun-Times - I’m Zlatan - Investment Week - Macworld - MAD Magazine - Maxim - Popular Photography - Popular Science - RedEye - Symbolia - The Next Web Magazine - The San Francisco Chronicle - Victoria & Albert Museum - Web MD

Super Clients…  … Can give lot of growth…

… Can give lot of growth…

2 Likes

Tried digging deeper into Mag+…

Financials :

As per AR of Mag+ AB, financials are available upto FY14 (December-ending so in a way our MPS’s FY15 barring one quarter) :

INR converted revenues are 14.89 cr., 12.94 cr., 6.33 cr. and 4.64 cr. for Dec’14, Dec’13, Dec’12 and Dec’11 respectively.

INR converted EBITDA Loss are -(6.98) cr., -(18.63) cr., -(22.56) cr. and -(27.74) cr for Dec’14, Dec’13, Dec’12 and Dec’11 respectively.

This is typical for initial phase of a product development company. Majority of the cost is Personnel costs wherein salary seems average ~INR 0.70 cr. p.a.

Another Notable thing is – starting November’2013, all selling and marketing functions are handled by Mag+ Inc based in US, so, whether the numbers include this entity’s nos. or not that is unclear. However, that should be material post Dec’13 nos. as the entity didn’t exist before that.

My Take on Acquisition :

Company has good platform in hands and its target seems to be small magazine publishers and Corporate SMEs. The company reminds of the previous big acquisition done by Mr. Arora that of MPS from Macmillan – here we have the legacy of Bonnier as also a first mover in the space having launched ‘Popular Science’ concurrently with IPAD launch in 2010.

However, similarities end there as financial history of the company is not as strong as MPS had under Macmillan, as also connection with the parent is also not as strong as we have Bonnier removing its titles from Mag+ to Adobe DPS starting mid-2014. This is really surprising as we don’t often see any organisation putting more trust on a peer platform than inhouse developed platform. How much Bonnier contributed to Mag+ that only Dec’15 results can tell which we don’t have.

Another aspect to note is, with this acquisition, MPS gets scope for a non-linear revenue stream. However, it has not came ready-made and MPS will have to work really hard to develop this stream if past financials of Mag+ is anything to go by. Still, MPS is not having any strength as far as sales & marketing goes and that is what is critically required by Mag+. With a good investment, Mag+ could become a good BU of MPS but ‘initial good investment’ is what is required.

Its like acquisition of a good potential startup. If we are thinking of considerable improvement in profitability of Mag+ like Mr. Arora did with MPS or Element or will do for TSI, then that might be quite difficult with Mag+ as its a product/platform business and not a services business. This is not to say that such high reported losses of Mag+ will remain under MPS too as the losses that we see were in development phase and if the platform is fully developed, what might be required will only be investment in marketing and technology upgrade. But, this acquisition is definitely not a play on Mr. Arora’s strengths.

Lastly, in addition to its future performance, it all depends on what price is paid for this acquisition to judge whether its a good, bad or ok acquisition from shareholder point-of-view.

– If Mr. Arora has clinched this acquisition at a bargain price like he did for last three acquisitions, then its a great acquisition as it opens up good opportunity window at just a small cost (like say 0.5x Mag+ sales).

– If this acquisition is done at reasonable price ( say 1x Mag+ sales) by utilizing company’s internal accruals minus QIP funds, its an ok acquisition from shareholder point-of-view as it will require still further investments by MPS to make this acquisition a success and risk-reward in that case is 50-50.

– If QIP funds in anyway are used for this acquisition then its a really bad acquisition unless the company has turned profitable in Dec’15 results which is highly unlikely or when combined with Mag+ Inc USA, the results look considerably different than we actually have.

I am surprised at the silence of the acquisition price as otherwise on past occasions, MPS has been quite forthwith and fairly transparent on that count (if we remember, in case of last acquisition which was TSI – first acquisition post QIP-- management came immediately with a separate Q&A in addition to press release in which revenue, profitability and acquisition price was mentioned). However, there might be some form of NDA signed with Bonnier because of which for a certain time-period, financial details might not be disclosed. We might have to wait for Q1FY17 concall for any clarity on this front. If anyone is attending AGM on 19th July, then it might be a good platform to answer some of such queries.

Rgds.

Discl.- Negligible Holding.

12 Likes

Apart from the analysis, one fact pointed out by somebody on MControl Board, is that Ramesh Damani, one of the most astute investors worth about 6,000 crs. is one of the top 10 investors in MPS - this is disclosed in the Annual Report. Also, in the AR is that Goldman has increased stake while HDFC has reduced their stake during the year.

Q1FY17 results on 19th July…date is as usual with AGM date but no interim dividend is a surprise…either it signifies the company closer to a big acquisition or the price paid to acquire Mag+ seems to be higher than I expected.

Rgds.

Discl. - Negligible Holding

Board Meeting Intimation for Results

MPS Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on July 19, 2016, inter alia, to consider and approve Un-Audited Financial Results (Standalone and Consolidated) for the quarter ended June 30, 2016.

Hi Mahesh,

Thanks for the information. Does the information on dividend generally come on the date of announcement of intimation for results. Is there a possibility of announcement of dividend on the day of AGM or before that?

Thanks,

Kunal

Discl: Invested in the company

Hi Kunal,

Normally if Interim Dividend is to be considered in a board meet, it’s clearly stated in the announcement. Whereas board can take a matter which is not in advance set out clearly in the agenda and therefore the announcement, however, with the standards set by MPS management on all previous occasions, possibility of such event occurring seems rare.

Rgds.

1 Like

I will be at AGM tomorrow.

Regards,

Raj

Hi Raj,

Good to hear that you will be attending the AGM of MPS…If possible, do try to extract following info :

(1) 27 % of company’s billing is done in GBP and 2 % in Euro, so it is clear that Europe contribution must be more than 25 % to company’s revenue. Does the company foresee any impact of recent developments on existing or likely contracts.

(2) Clarification regarding recent acquisition Mag+'s revenue and profitability.

(3) What is the price paid for the acquisition…if exact amount can’t be disclosed then atleast clarification asto whether QIP funds are atall used for acquisition. Also, what sort of further investment company is likely to make in the acquired entity.

(4) For the first time, company has ventured outside educational publishing space …slightly into magazine space but more into corporate and institutional communication space. So can this be considered the beginning of company likely to pursue other areas for growth than company’s traditional stronghold segments.

Do update your feedback/takeaways from the AGM in the thread.

Rgds.

good to hear that Raj…

please try to get answers of Mahesh’s questions…

mag+ price and what are expected revenues/profits are very important

Bad Results… definitely not looking good

Results are out. came out about an hour ago. 5% tanking speaks volumes of where the expectation and actuals are.

PS - invested and cringing

Q1FY17 results out :

Prima facie, results look very disappointing with yoy standalone cc degrowth of - (6.4) %, ; such a massive cc degrowth was last seen in FY13 (last in Q3FY13 of -(5.88) %) when post acquisition from Macmillan, many contracts were restructured and company had to resort to severe pricing cuts. EBITDA margins at consolidated levels have suffered ~80 basis points yoy despite profit at subsidiary level. This doesn’t include the effect of Mag+ acquisition related expenses (since it was acquired in July’16) as also Mag+ losses if any.

More surprising as also disappointing is the fact that from this quarter’s presentation, $ revenue figure is missing which is not expected from a credible management like MPS has…Management should very well be aware that as members of knowledgeable investors’ community, such figures can be easily derived by us via putting some efforts…Consolidated USD Revenue of Q1FY16 was 9.483 mn. on USD-INR average Q1FY16 conversion rate of 63.64 — whereas for Q1FY17, consolidated USD revenue comes to 9.253 mn. on USD-INR average Q1FY17 conversion rate of 66.88 – a cc degrowth of -(2.42) % at consolidated level…I would have preferred management accepting this fact by disclosing $ revenue figures in presentation as was done in all previous occasions when there was positive consolidated cc growth.

Mag+ acquisition cost including further immediate investment is INR 23.72 cr. ; no revenue and profitability figures of Mag+ are announced yet. Also, Dec’15 results (so almost FY16 for MPS’s Mar-ending fiscal) of Mag+ AB are out and INr converted revenue is INR 15.83 cr. with a EBITDA loss of 2.64 cr…do note here that these numbers doesn’t seem to include Mag + Inc numbers so its only MPS management that can provide accurate revenue and profitability figures of Mag+. However, in case total revenue and profitability of Mag+ is nearby Mag+ AB reported numbers then the price paid for acquisition seems 50-50 risk-reward situation for shareholders.

Also, this MAg+ acquisition is said to be done via QIP funds.

Rgds.

Discl. - Negligible Holding

6 Likes

To add, Europe is still contributing 40 % + to company’s revenue and 28 % of the billing is done in GBP…so, in case GBP remains at current level for the whole of Q2FY17, then Q2FY17 will be very interesting to watch as although brexit impact, if any, might have its effect in medium term, but GBP depreciation could have an immediate impact.

GBP-INR average for Q1FY17 = 95.88.

GBP-INR average for July’16 so far = 88.21.

USD-INR average for Q1FY17 = 66.88.

USD-INR average for July’16 so far = 67.17.

Rgds.

1 Like

Updated statistics post Q1FY17 numbers :

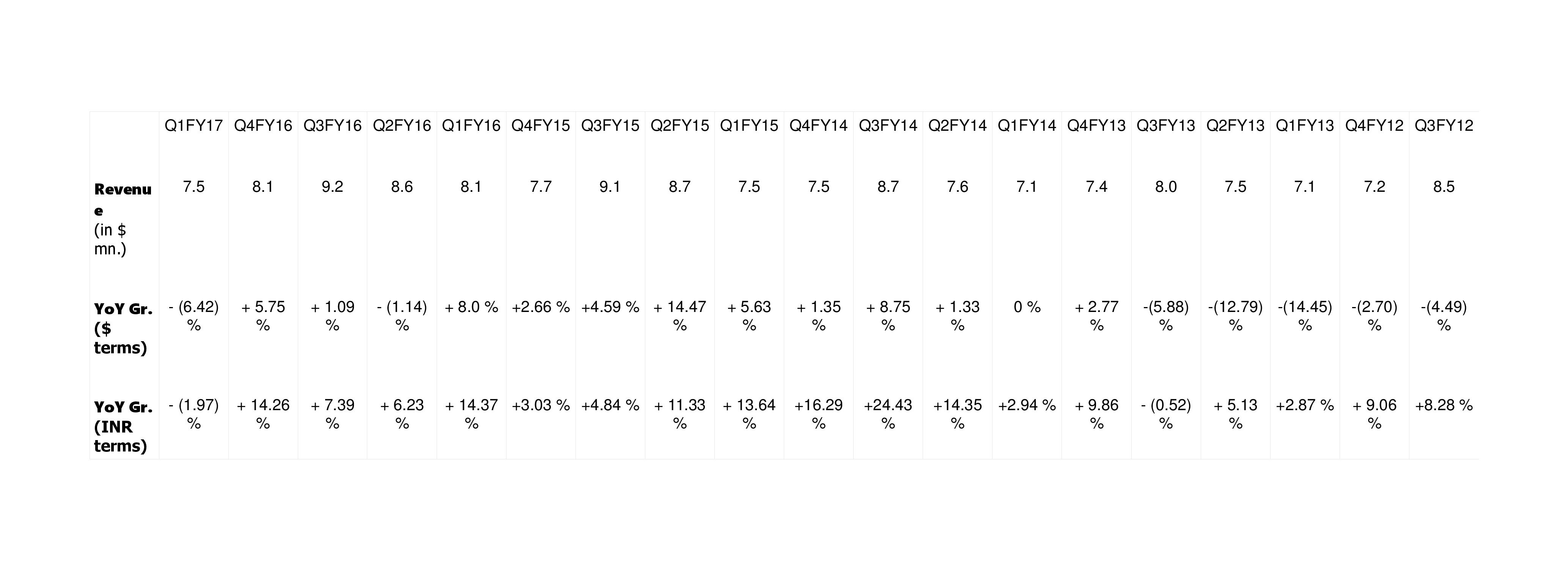

Standalone Quarterly Revenue growth trend in both $ terms and INR terms of MPS post acquisition by Mr. Arora :

– As stated before, in $ terms, this is the first time company has witnessed more than 5 % YoY degrowth post Q3FY13.

– In INR terms, Q1FY17 has witnessed the highest degrowth YoY post acquisition by Mr. Arora. It was only one time before, in Q3FY13, that company witnessed a -(0.52) % YoY INR degrowth in standalone revenues.

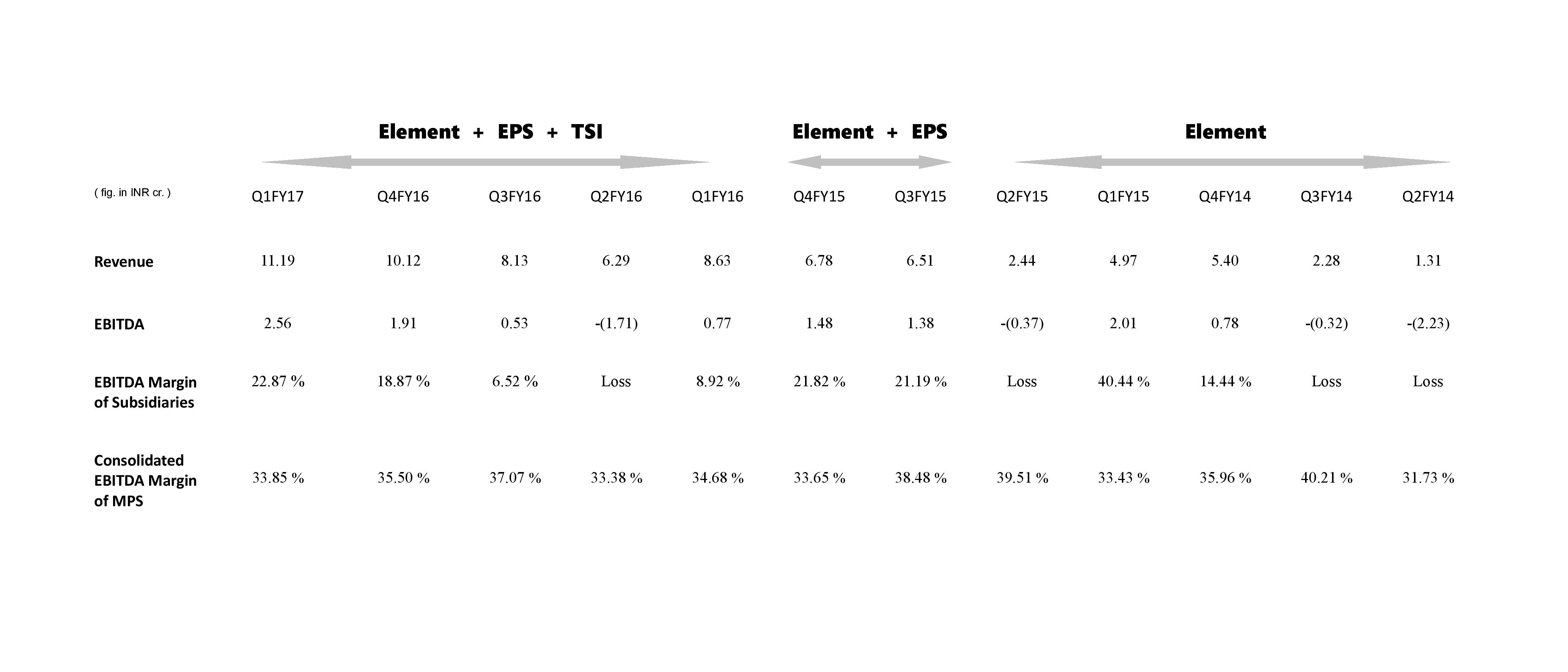

Performance trend of MPS North America since its existence :

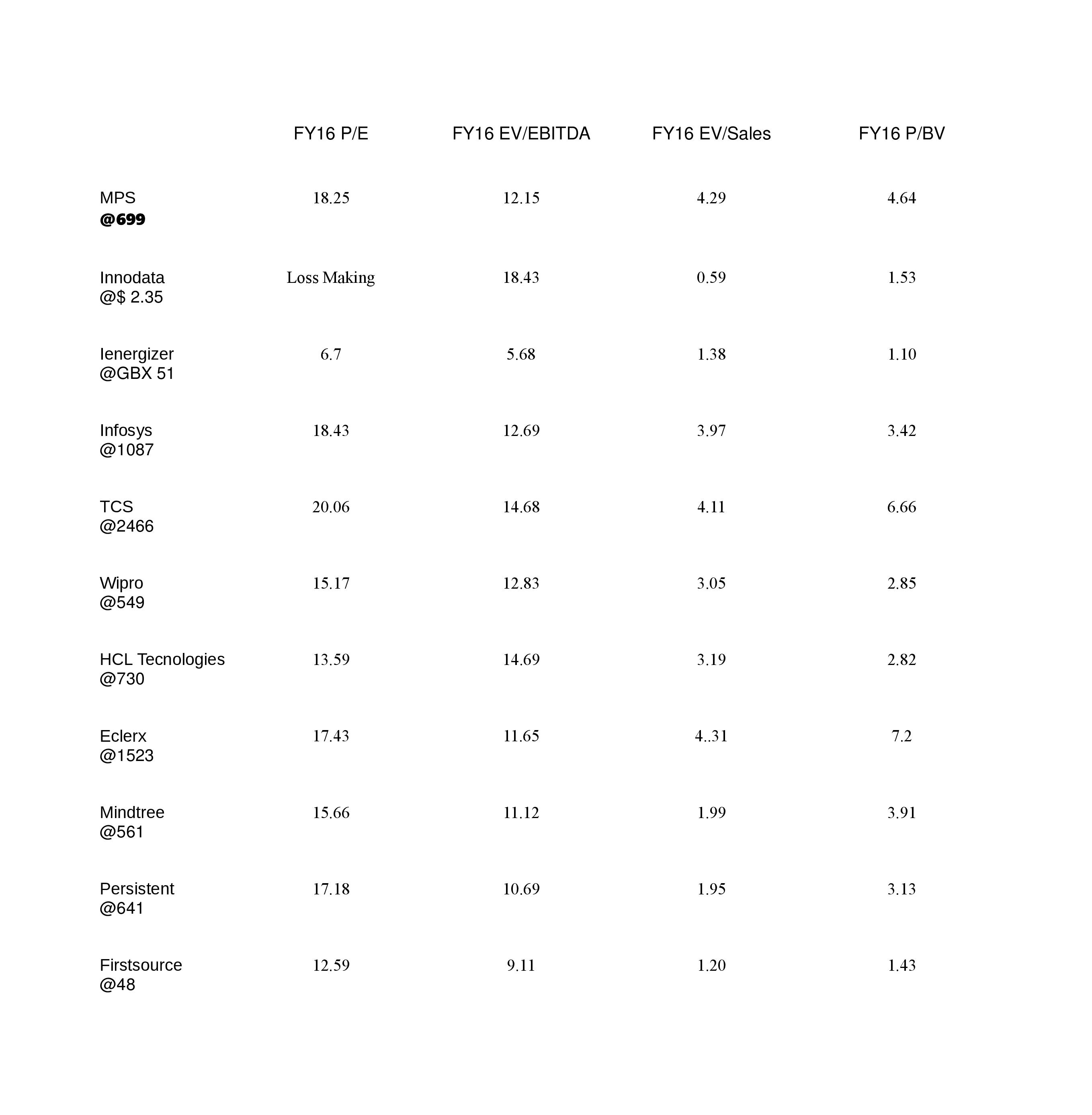

MPS current Valuations v/s Its own larger international listed peers as also Major IT players :

– Ienergizer (Aptara), the largest player in the industry of our concern and MPS’s largest peer, even after recent significant run-up in its share price is trading at just 6.7 P/E and 5.68x FY16 EV/EBITDA. Company has registered ~24 % EBITDA margins in FY16.

– MPS at CMP is trading at a premium or at par (on majority of the valuation multiples) with most of the big IT players of India which include Infosys, Wipro, HCL Tech, etc… It is notable that when these Indian IT majors were reporting high single digit cc growth, MPS was reporting low single digit cc growth but when in Q1FY17 we are seeing major IT players struggling and posting low single digit cc growth, MPS has reported cc degrowth. Whether this is coincidence or not that only time can tell but my long-standing concerns still remain and are becoming more pronounced.

No interim dividend is declared this time alongwith Q1 numbers.

Tomorrow’s concall commentary will be interesting to watch so will be today’s AGM feedback.

Rgds.

3 Likes

Mahesh… Thanks for your analysis.