@pikrohit has already summarised key takeaways from concall very well…just to add few minor takeaways :

– Company is likely to report “constant currency” numbers starting next FY (for better assessment) rather than plain converted USD numbers.

(Even we can carry out such approximate exercise via currency billing % but how this will be much different than USD converted cc growth numbers that I doubt as 69 % of company’s revenues are already billed in USD and its only other 31 % that are billed in other currencies.)

– Employee count as at Q4FY16 is 3001 v/s last year’s 2858.

– Company’s strategy for organic growth is –

(a) Identify new outsourcing areas, in close association with clients, where company is not present currently., and

(b) In traditional areas, enter into long term volume arrangements with clients.

– Company’s Acquisition preference is

(a) Acquired company should be a premier brand., and

(b) Acquisition should be blessed by existing customers.

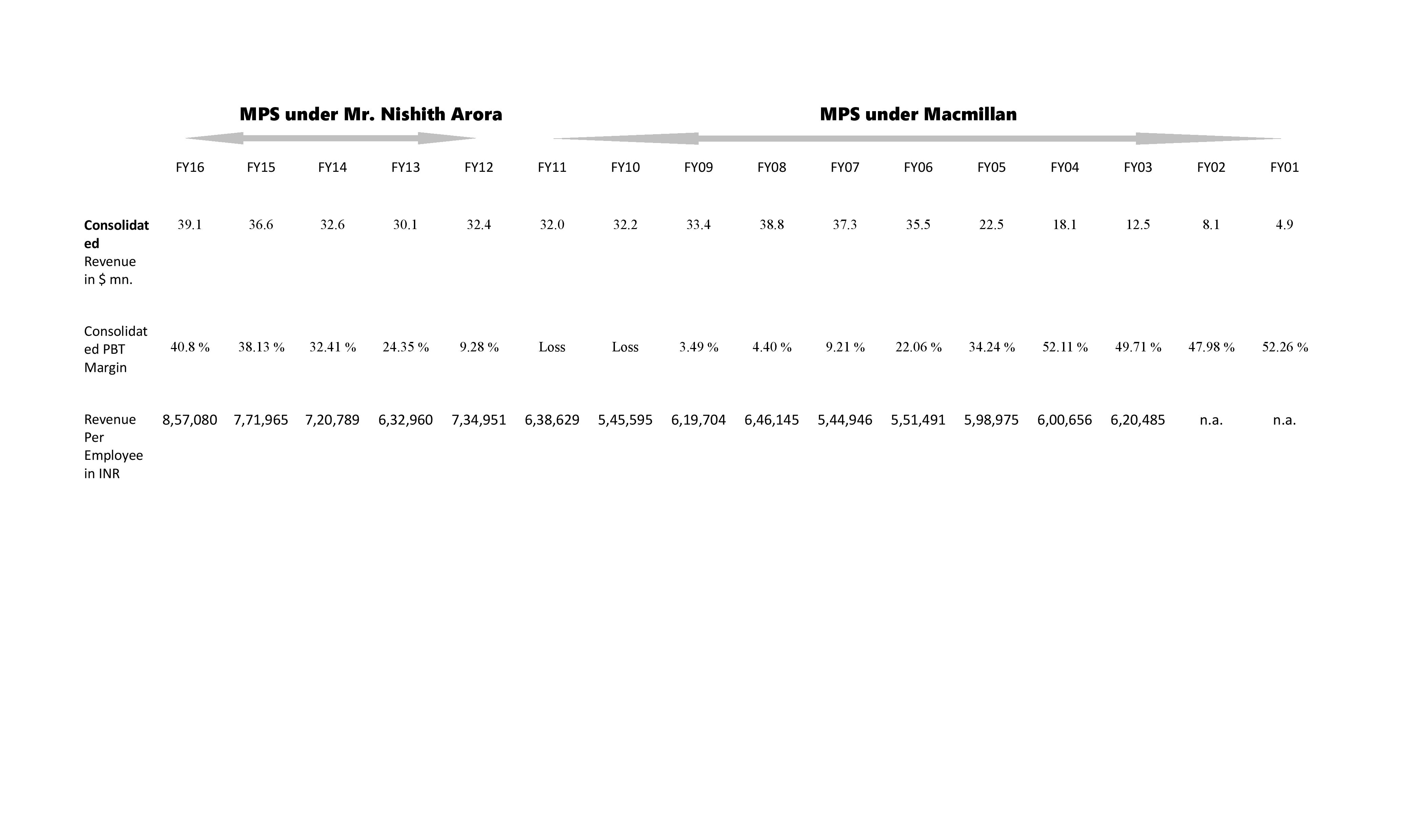

– Company stays committed to its aspiration of doubling revenues by FY18 (although timeline not stated clearly but recalling original statement of management given in Q4FY15). However, management doesn’t want to atpresent think of “USD 200 mn. revenue by FY20” aspirational guidance provided during QIP roadshows as its first goal is to double its revenues.

My Personal Positive/Negative Notes post Q4FY16 Results & Concall Commentary as well as Other Allied Events:

Positives :

– Company standing by its first aspiration of doubling revenues is the major positive takeaway for me and if it sticks by the given timeline too, then acquisition might not be too far away as already we are sitting at the end of Q1FY17.

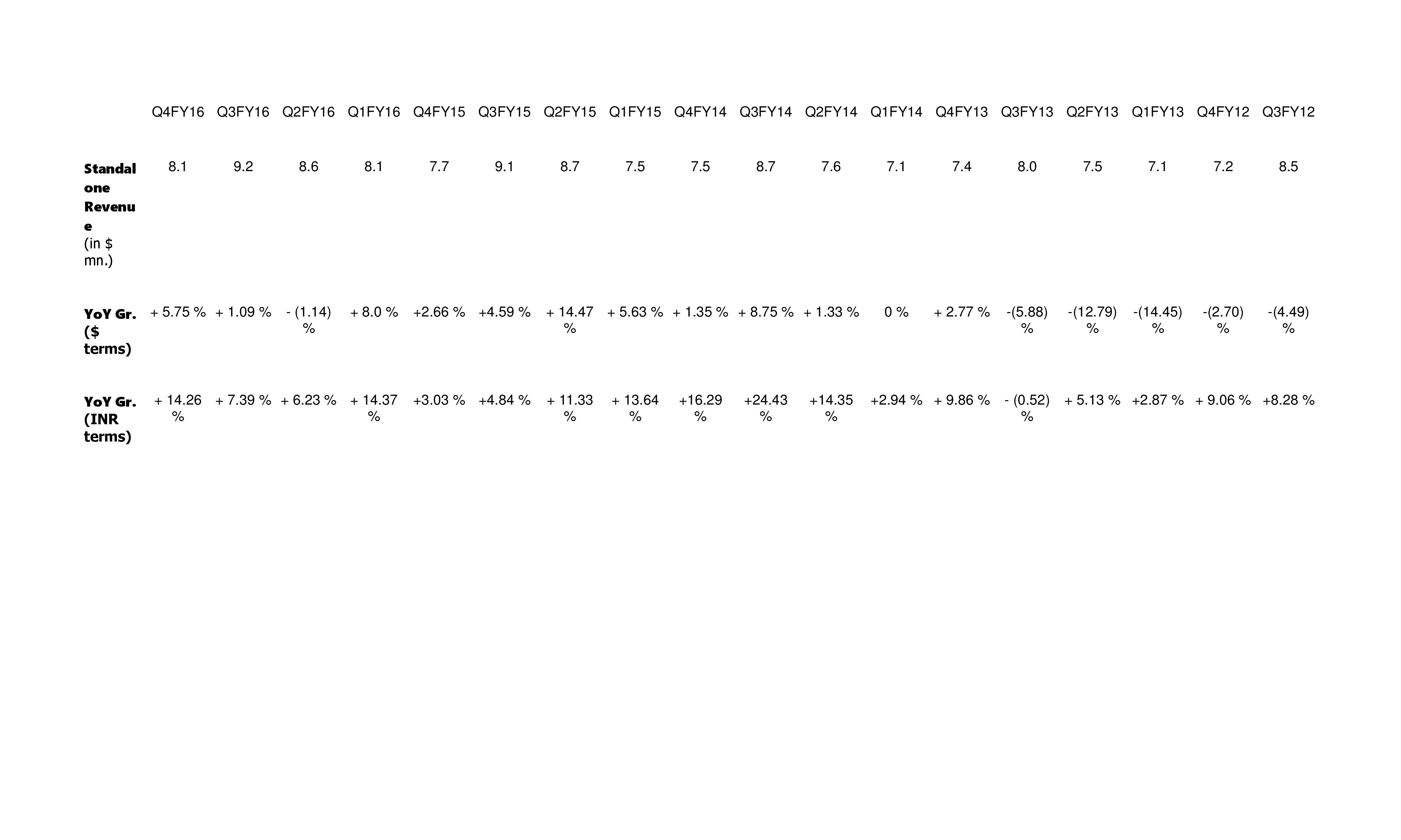

– A 5 % + cc standalone revenue growth in Q4FY16 is the second positive that I see as atleast company has ended the year on a positive note.

– Company’s strategy for achieving organic growth seems reasonable as now it seems to be reconciling with ground realities and looking at new allied outsourcing areas where company is not present currently. An acquisition could give a good headstart to this strategy as otherwise building an entire practice from scratch could be difficult.

If we do a ground check, company seems to be moving in right direction by building a strong front-end client-facing team –

John Sollami – who was VP Operations North America under Macmillan-era comes back in same position now,

John Martel – who has a two decade career in Publishing industry comes as Director Business Development MPS North America

Jamie West – who again has an almost two decades career in publishing industry in organisations like McGraw-Hill & Houghton Mifflin comes as SVP Product Development

Marie McNamara – who again has more than two decades career in publishing industry now comes as VP New Business Development (this is because of the acquisition of TSI)

Raghavendra Pratap Singh – comes as AVP Product Development & Marketing from Aptara

Satya Pal – who was incharge of MPS Technologies since Macmillan-era and who left to join Woolters Kluwer, again rejoins as VP & Business Head of MPS Technologies.

– In addition, it was satisfying to see Yamini Arora (wife of CEO & daughter-in-law of Nishith Arora) leading MPS’s presence in recent IDPF Conference – I like those companies where promoter family members are not only recruited at senior management positions for namesake but also put-in efforts themselves to grow the business of the company.

– To add, company seems to be awakening to power of social media marketing as we see its twitter account getting recently reactivated with few posts. Although its nowhere near the likes of Aptara or even smaller player like Hurix in terms of both quality, quantity as well as followers gained but atleast some start is made.

– Rahul Arora seemed completely under control this time and answered most of the queries quite well (reminded of Nishith Arora’s initial concalls) without any fumbling.

– Besides this results and concall events, two positives can be picked up from industry developments :

Innodata, the third largest player of the industry, in its last week declared Mar’16 quarterly numbers, registered higher than guided revenues in its Content Services division (business comparable to MPS). In earnings call held post the results, management stated, “revenue in the Content Services segment was $13.6 million which was about $0.5 million higher from the top end of the guidance we provided in our last earnings release. By having exceeded guidance by this much, resulted from higher than forecasted requirements from several customers and highlights are difficult that can beat a forecast revenues from quarter to quarter in our content services business.”

In a similar development, Ienergizer, Apatara’s parent, last month said in a filing to exchanges, “iEnergizer is delighted to announce that the company expects to report a significant increase in EBITDA for the year ended 31 March 2016. This out turn is likely to be above the company’s original target and budget and has resulted from the combination of renewed business momentum, contract wins and the successful implementation of the transformation plan.” The said transformation plan included consolidation of its content services division (Aptara) into its operations centre in Noida, India, and rationalising selling, general and administrative costs.

Negatives :

Biggest negative for me remains my old reservation of the way funds were raised ahead of time. This time we are hearing a hilarious (if not ludicrous) statement from Mr. Nishith Arora who states “We continue to evaluate opportunities, we looked at many in the past, just when we felt we were getting close to something, more better comes along and then we say we take a closer look at something else…” (exact statement reproduced in quotes almost as it was said, still one can check concall transcript in case of any mistake on my part).

This is like, you are a prospective groom in the best age suitable for your marriage and are looking for prospective brides and you are close to finalising proposal with one girl which you felt is good, some other girl comes along exactly at that time which you feel is better and then you start going after her and its when you are close to finalising your marriage with that another better girl then some other more better girl comes your way and you go after her…If you are a “Salman Khan“ then one day you might find the best match as perceived by you (remember, even Salman Khan is unmarried till now) but if you are an above average or even a good common man type prospective groom, there is high probability of your suitable age of marriage passing away and finally you being compromising on a sub-standard (relative to previous proposals) prospective match or not marrying atall.

I really pity institutional investors who lent their support during QIP (HDFC & Goldman). After 14 months of their investment what they are getting is 2.63 % return (via dividends) on their investment and a notional loss of 20 % + on capital invested. They don’t have a choice but to stay with the company as its an illiquid share and no other institutional investor is going to come at current juncture into the company. Management’s statement that they have discussed with QIP investors and have full support of them doesn’t match as if they were in support of management’s unreasonable delay in deploying funds, they would have increased their exposure to the company by buying more at 22 % lesser price or atleast some other institutional guys would have come in.

Those who are in support of this fund raising ahead of time and then not deploying funds for this much time, just think if these funds were raised by the company via IPO and retail investors were involved where in “Objects of Offer” inorganic purpose was written…if such IPO company would have not deployed funds for 14 months even after raising funds from the public, i.e. us, what thought would have gone on the back of our mind ??

I am severely criticising this “raising of funds ahead of time and delay in deployment of funds” policy as be it be any management whatsoever, no one has right to take any form of investors for ride. If its money generated via internal accruals and you are keeping it as cash without deployment (like most of the IT guys like Infosys, TCS have), its completely fine, but, if you are raising funds by diluting equity because of some purpose, you need to have concrete proposals inplace as fund-raising from any form of investors brings with itself commitment and huge responsibility.

I sincerely hope that this delay in acquisition is perfectly justified by the management by doing a great acquisition and it silences critics like me completely. On my part I will be more than happy and I want that I get silenced as I am surprised by this one bad move by otherwise a great management led by Mr. Nishith Arora.

– Second key negative is only 3 % YoY standalone cc growth in FY16 v/s FY15. However, this is understandable and not a surprise and we need to look at what future brings, especially FY17.

Valuation :

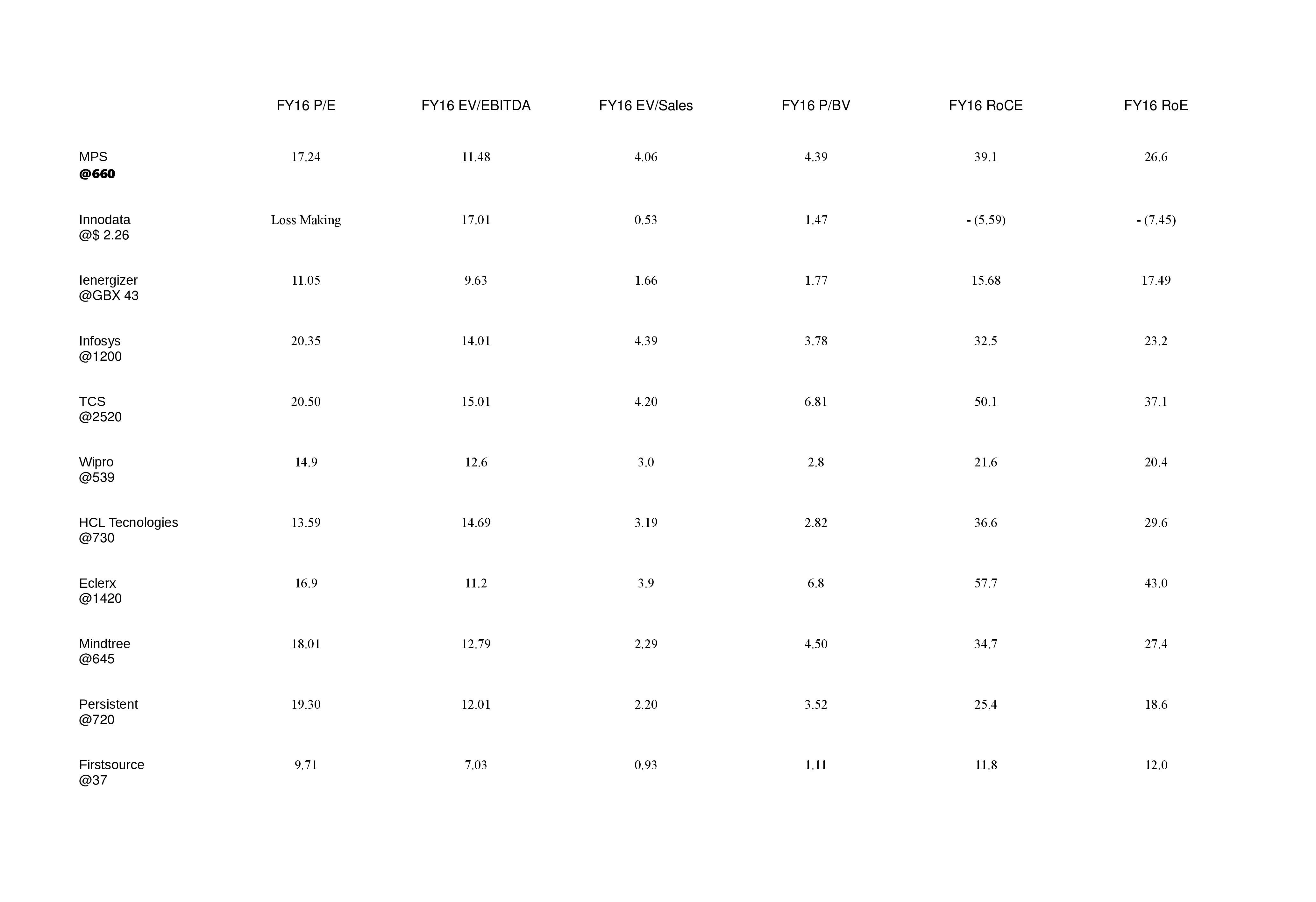

@srnarayan asked before regarding my view on valuations. Just refer the table below :

in above table only Ienergizer valuation multiples are based on FY15 numbers.

– Based on the valuations commanded by major peers of MPS as also other Indian IT players, I personally feel 10-12x FY16 EV/EBITDA should be the bottom for MPS if EBITDA margins can be sustained at even 35 %. I am not considering here P/E as it will include effect of other income because of huge cash company has. Although at just 11.4xFY16 EV/EBITDA it is attractively valued right now as no positives seem to be priced in, but, its only acquisition profile that could provide trigger as in financial circle that I talk to, I clearly see brand image of MPS going down and frustration getting into even the most loyal MPS shareholders.

While saying all these, it is also equally important to state that Q4FY16 results are not that bad or cash available with the company is not burnt in anyway to warrant a massive 11 % correction post declaration of results.

Note – Despite my negligible holdings of less than 1 % of my pf, I have tried to be as unbiased as possible while stating positives and negatives above. However, these are my personal views and no conclusion should be derived out of that as I can be wrong.

Discl. - Negligible Holdings. Less than 1 % of pf., Bought in last three days post results. Planning to buy more next week if valuation permits.