People immigration related to Germany to USA only. I just missed mentioning.destination country.

Mohnish Pabrai recently gave a lecture to the students of Peking University (Guanghua School of Management). In it, he talks about his meeting with Mr. Vivek Chaand Sehgal and then goes on to explain the ingenious acquisition strategy of Motherson Sumi Systems. Very important video to watch, if you are a investor / interested in this company:

I have captured the YT link at the exact moment he begins to talk about the company. So you don’t have to navigate anywhere… just hit the play button and enjoy the talk.

10 Likes

Thanks for sharing the video!

Would take Pabrai’s words with a pinch of salt as some of his statements don’t fall in place.

The rear-view mirror acquisition he is referring to is the Visiocorp acquisition.

- It was not $100 million deal. It costed Motherson Sumi around 25 Million Euros.

- Again, wouldn’t trust that BMW had written a check to Motherson Sumi to buy Visiocorp.

One can verify my comments with 2009 annual report’s cashflow numbers i.e. 171.6 crores of Motherson’s cash gone into acquisition.

1 Like

True. I found it very hard to believe that BMW would fund Motherson Sumi’s purchases. If it did, where is the cash flow to show for it? But the speech does alleviate the question of whether Motherson Sumi is doing ‘diworsification’. It’s clearly not, because the take-overs largely happen after an indirect confirmation that they will be a profitable ones (More or less).

1 Like

I am not saying or confirming whatever Monish is saying is true or false, but in case it is true, it will not reflect in cash flows, reason being if BMW writes a cheque to Motherson, it would be advance from customer / reduction in debtors and not an interest bearing finance payment, which a cash flow (from financing activities) typically shows.

So, if you check the cash flow from operating activities, cash outflow in working capital changes for year 2008-09 & 2009-10 is surprisingly much less than year after (2010-11).

Another way to judge this, I see for adding around Rs 4000 cr sale (158% increase), receivables rose just Rs 150 cr (or 25%) in this case… or 26 times debtor turnover ratio (for incremental sales) compared to 4.22 times the previous year.

However, when they made another acquisition in 2011-12, receivables rose by abt Rs 2000 cr (200%) compared to sale rise of 80% (Rs 6500 cr). This looks reasonable at 3.5 times debtor turnover ratio (for incremental sales)…

So, it looks to me that their might be some truth about the statement regarding visiocorp acquisition but has the trend continued? I can not be sure…

Disc: Not invested… Not planning to add either.

1 Like

With all due respect to Mohnish Pabrai and his investing skills and returns he generated for past 20+ years, I find him as a great marketer of his own stock picks. He tend to give lot of lectures to various universities around the world where he openly take names of the companies where he invested.

Few years back, after reading his “Dhandho investor” book, I was impressed by him and bought South Indian Bank and J&K bank after listening to one of his videos. Stock lost more than 50% of its value within one year of my investment and went further down for many more years.  It was clearly my naivety to copy him after listening to his idea of copying Warren and Charlie… Now a days when I come across any such videos, I take those with fistful of salts…

It was clearly my naivety to copy him after listening to his idea of copying Warren and Charlie… Now a days when I come across any such videos, I take those with fistful of salts…

10 Likes

Except Mr.Kedia, I have not found anyone who are true to his beliefs. Still one should not copy him blindly

1 Like

Firstly, Mr. Pabrai mentioned how Motheson Sumi only works with a few major automakers. Not true, they work with almost everyone out there. So, reliance on a major carmaker is out of the picture. This will be clear to everyone who has seen Motherson’s last investor presentation.

Secondly, he is using Motherson Sumi as an example to clearly show how Rain Industries is an even better proposition. He is making up Motherson Sumi as one of the best company out there and then announcing how his investment in Rain is even better.

BMW is already working with 1000’s of major players out there. Force Motors makes engines for them for e.g… Lack of a part from one company might delay BMW’s production at best.

Mr. Pabrai probably knew his video will be on YOUTUBE. Follow it at your own risk. (With all due respects to Mr. Pabrai and his funds.)

Disc: Invested. This is not a suggestion to buy/ not buy/ Sell any stock.

1 Like

short video to understand the basics about the company and the recent issues affecting the company.

1 Like

FY19 Annual Report is out.

Management has come with the theme of “Do not lower your goals to the level of your abilities. Instead, raise your abilities to the height of your goals”. They better be really confident of achieving their FY20 target ![]()

As usual very clear on what kind of acquisition they want to pursue. Check below snip.

I believed that only SMR was their top acquisition, followed by SMP. And PKC, Reydel are not that great acquisitions after all. One can go through the acquisitions slide in the PPT I have shared above to check the same. Looks like management deep inside believes the same as they always keep referring to SMR instead of the latest acquisitions when they want to quote their previous successful acquisitions. See below snips where management refers to SMR.

If management does PKC / Reydel kind of acquisition, I’ll stop tracking this company and divert my energy to something else. However, having build some conviction on the management, I have a strong feeling that Sehgal is going to come up with SMR like acquisition. Current anticipated global slowdown should hopefully help him achieve that.

Other notes from the AR include:

- SMR’s new plant in Yangcheng, China to manufacture complex modular subassemblies for mirrors

- Supplying wiring harnesses to electric truck by one of its global customers in Japan

- Focus of Motherson Innovations (MI) on the interiors business to build ‘Empathic Cockpit’. Other focus projects for MI are future interior of 2025 and beyond, such as active surfaces, smart materials, ambience and comfort features, plus intuitive user-interface tech

- Diversification of the business can be a key element of the company’s strategy, supporting the work they are doing towards other industries such as medical, aerospace and defence, which might become a more significant part of the Group in the future (Is this a red flag?)

Discl: No holdings. Waiting for acquisition. Please do your own research.

4 Likes

Sometime back the management said they will do better when EV cars become common in the market. The reason cited was more wiring harness for an EV.

However we can now see the patent filed by Tesla for their new wiring harness system. This is expected to be used in Model Y. Also we can expect Tesla to donate the patent to the auto industry as they have done in the past. This wiring system will reduce the amount of wiring harness used in a car and save huge amount of weight.

What is the new wiring harness?

Think of it to be something like POE (power over Ethernet). We would have used Poe cameras at home to save on wiring cost. We use a single Ethernet cable to pass electricity as well as data. This saves cost on wiring.

Similarly, Tesla’s new wiring harness will allow sharing of cable between all devices and equipments. The data flows like an Ethernet wire carrying data and power across devices.

What are the advantages?

- Reduction in amount of wiring harness as you don’t need separate wiring from battery. One can tap the wire from nearest hub (think of a router/ access point).

- Reduced weight of car

- Reduction in cost

- Plug and play upgrades. One can change discrete components without adding/replacing expensive wiring harness.

- Robots can install the wiring instead of current human labour. Saves money and time. makes it much more robust and consistent.

Impact to Motherson:

If future cars start utilizing this process, there may be possible impact to Motherson even for ICE cars. This new technology can be used even for ICE cars.

Possible impact to wiring harness business in the next 1 to 3 years.

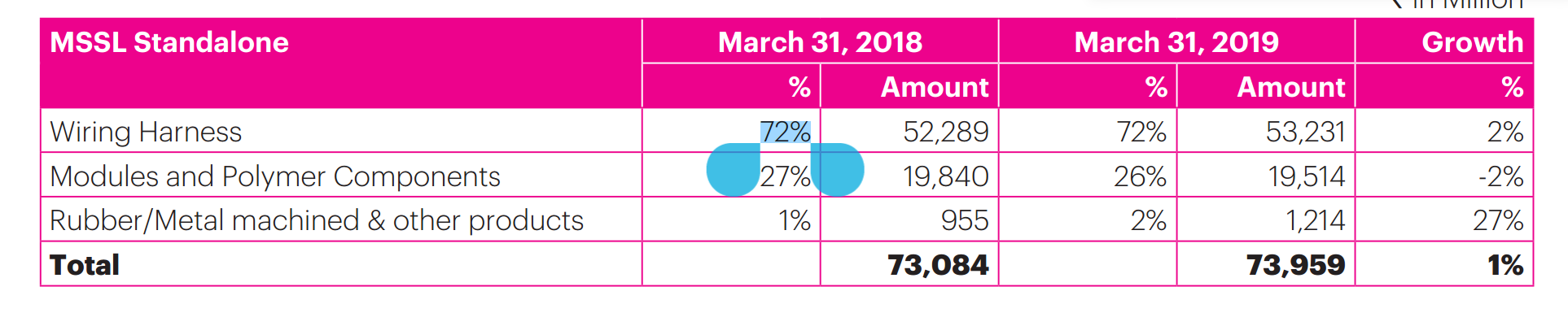

72% of MSSL standalone is from wiring harness

Reference:

Disclosure:.

No holdings now.

14 Likes

This is a very interesting development. If someone is already a shareholder here, can you please write to the CS asking for a comment from the management on this?

I don’t think MSSL conducts concalls, do they?

1 Like

they do conduct concalls

Motherson Sumi AR & Q1 FY20 Result Update!

https://drive.google.com/open?id=1VGVVI3RMbT1MZFlnoUAYwfAmWSoo0DgF

(Will Update Q2 soon)

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

4 Likes

Motherson Sumi Q2 Results!

https://drive.google.com/open?id=1EpkqfjZ7YlY7iq0A_g9mK9-8zN7lNsbo

(Disclaimer: Not an Investment/Trading Recommendation)

2 Likes

Restructuring

1 Like

The proposed restructuring and recent performance indicate the end of the 5 year planning era which had worked well for them for many years. This also questions their revenue growth target for 2020, geographical and custmomer diversification strategy. On the outset this looks like the story that the markets were hoping for is not playing out and the management has recognized this and taking corrective action. Just my opinion.

2 Likes

Conference call Highlights on recent crisis

- Plan on proposed de-merger: De-merger would go on as scheduled.

- Current status of production:

- SMP and SMR: Customers have announced plant shutdown. Europe is impacted. Car maker’s plant shutdowns have started. US plants are still running. Current plan of car maker’s is to shutdown plant for 15-30 days and if required extend it to 45 days. They can prepone some of the holidays coming in next week.

- Wiring harness (both domestic and outside): US not impacted much. Volume drop can happen though. But their plants running fine. China plants who were shutdown has come back now. Except one facility in China, all others (26 others) are working normally (with 70-80% workforce attendance). South America plants running. As long as OEM plants work, they would continue to operate. India operations running fine till now.

- Is there any stress on supplier side, vendor side, supply chain situation? Most of the components are coming from big companies like in wiring harness, supplies are from Sumitomo mostly, Polymers come from Reliance. So they are strong supplier. 90% of other child parts used to prepare module is made by MSSL. At the same time, there might be some issues here and there. Part of their 3CX15 has helped them because mostly they source locally, supply locally and procure locally. Hence reduced impact of supply side problem. Motherson sumi won’t fall short of OEM’s demand due to this. OEM might face issues due to other manufacturers. But if the plants are running, MSSL would do fine.

- Any credit stress? No banker approaching us for this issue.

- Liquidity issue of SMRPBV, if plants had to run on low utilization level? How are we placed on cash position? Have we arrangement to get additional credit line as and when required? Enough liquidity both on cash on balance sheet or the unused credit lines. Consider group for all such issue. Group will support SMRPBV, if at all required. Government is also coming up with support for this time.

- Will there be any breach of credit in dire situation? Will creditor take a lenient view in such scene? If required, both MSSL and SAMIL can repay then loan. We have enough cash

- SAMIL has share pledge of MSSL of about 6%. Vivek stressed that they can pay the debt now, if required.

- What Motherson is doing to ensure that once production starts after shutdown, that we don’t see 2nd round of infection? No case till now for MSSL employees.

- As stock price has significantly corrected, would you consider buy back? No buy back. We want to conserve the cash so that we could ensure smooth operations across the globe post this situation. Our share price had corrected significantly in last crisis, went down till 38 but we did good. So not worried about stock price.

- What is the worst case scenario you are considering? It is the length of the duration of the stoppage which we are thinking as worst case. Supply, Manpower and Financing are within our control, the problem is how long the customers (OEM) want to keep the plants shut down, that is the only issue. Fortunately as this was last year of our 5 year plan, we had done cash conserving from last year to increase ROCE at the end of 5 year plan. Also capex cycle has ended for us and so good financial cushion for us. We are expecting worst case plants to be shutdown for 30-45 days. Because of china example, all plants were shutdown and now they started again in a normal way. We repaid some of our loans as well, actively looking into cash position.

- Can there come any major off expenses due to this recent issues? Like increased expense and all? Mostly the impact on this Financial year should be muted, because plants are only closing now, with just 11 days left for year end. No further comments on March Numbers for now.

- There would be ways and means that OEM would try to cover this lost time of production, once the issue becomes normal.

- What would be the Capex in 2021? Not disclosed, but numbers would be way reduced as per current market situation. We had sufficient investment and the order book we have can be handled by existing plants. So not looking for much capex. Details at quarter end.

- We have a track record of acquiring company at great valuations at distressed time and this is very tough time. Comments on this front? Global valuations have come down dramatically and we are much better off as terms of valuation than a month ago. A lot of the companies need help and more than the companies the customers are telling us to go and have a talk with them. We are not giving up on the very clear target of 18 Billion with 40% ROCE. If ROCE is not there, we won’t do the acquisition.

- Any impact on the order book from OEM side in last 1 month? Noting as such.

- What can be the new trends emerging post crisis, do you see that export would go down and more local to local transactions would go up? Not actually due to this virus, but this issue has been present for some time due to Trump. Showing that production has to go local. Some importance given to local industry than export. It is better for MSSL because of local production. Had we had concentration in production in 10-15 plants, we had had huge issues. We will keep adapting whatever be the situation post this scenario.

- One of the thing Vivek has been mentioning throughout the call that there would be a rethink in the thought process of shared mobility which has been going around for some time. Even Diesel and petrol prices coming down to their lows, people might have second thoughts about a lot things. There is a lot of steam left in the business MSSL operates.

16 Likes

Thank you very much for sharing and provides a good insight. May be good time to start accumulation in SIP for next 3 -4 months

I have tracking position