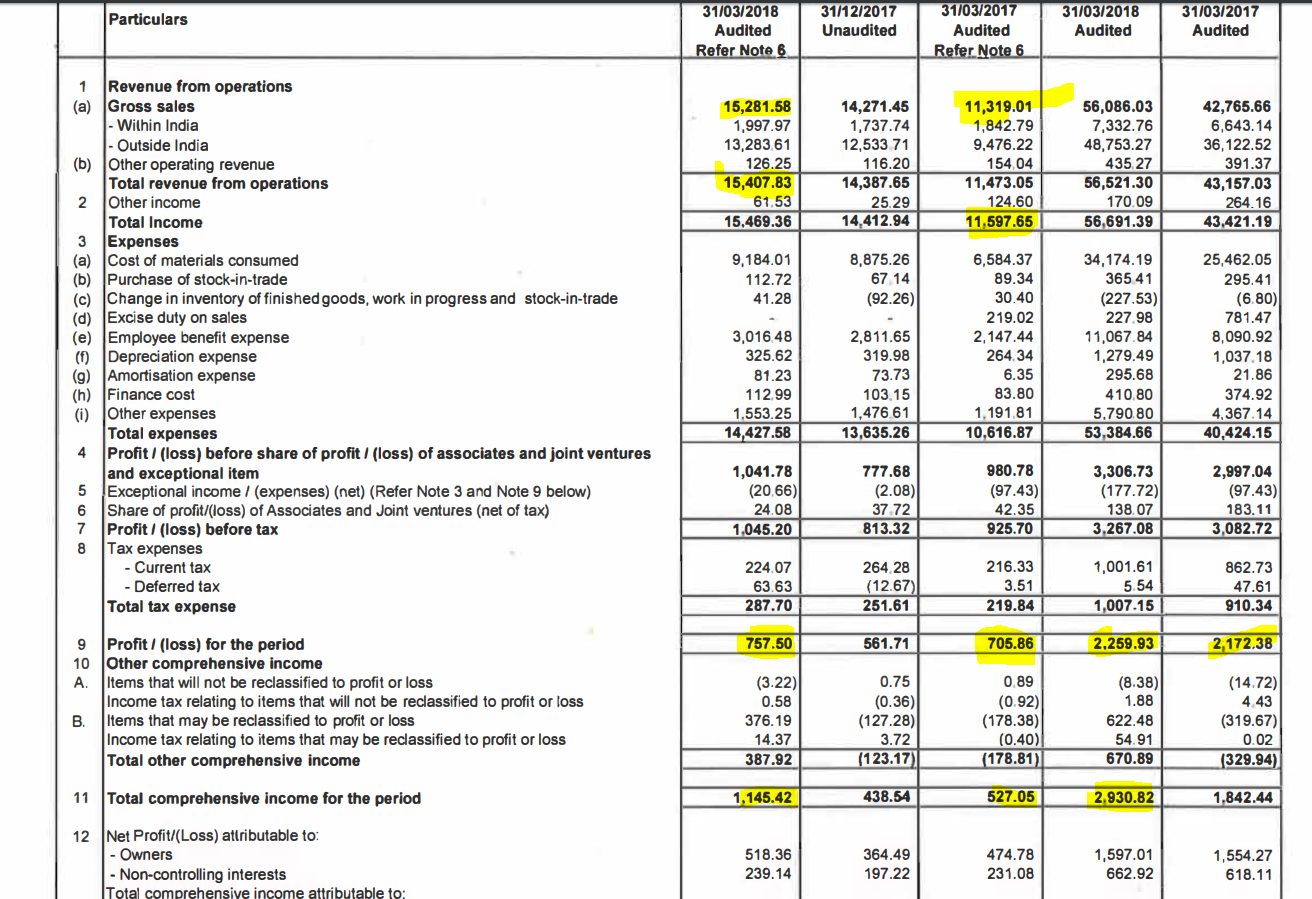

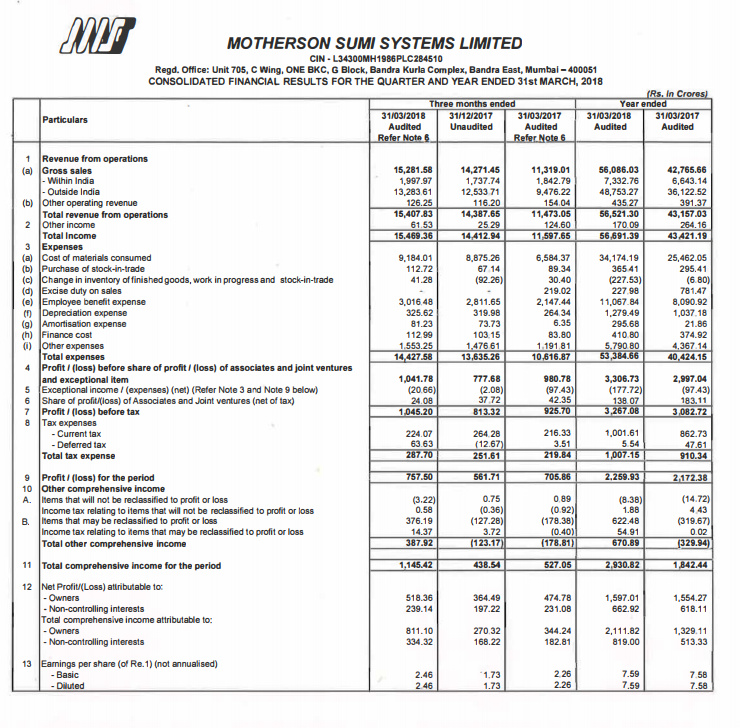

In the attached results , I can see quarterley Profit as 757 crores , while in the presentation it says 590 crores. Why this discrepancy ? Also the yearly no.s Profit figures do not seems to match (1939 crores in PPT vs 2930 crores in results)?

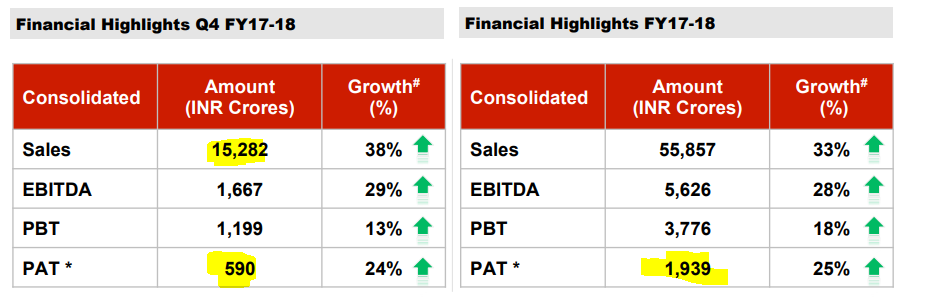

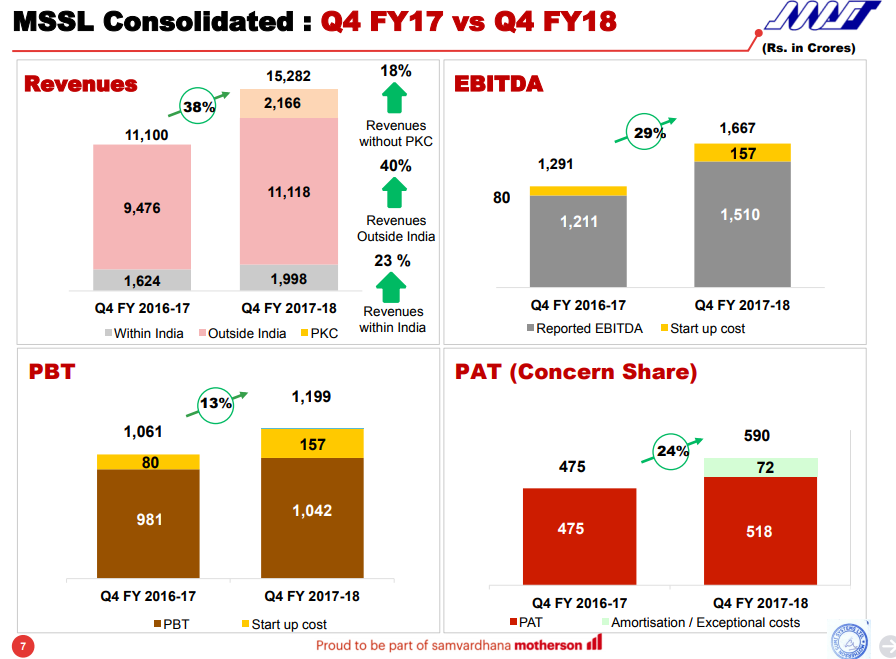

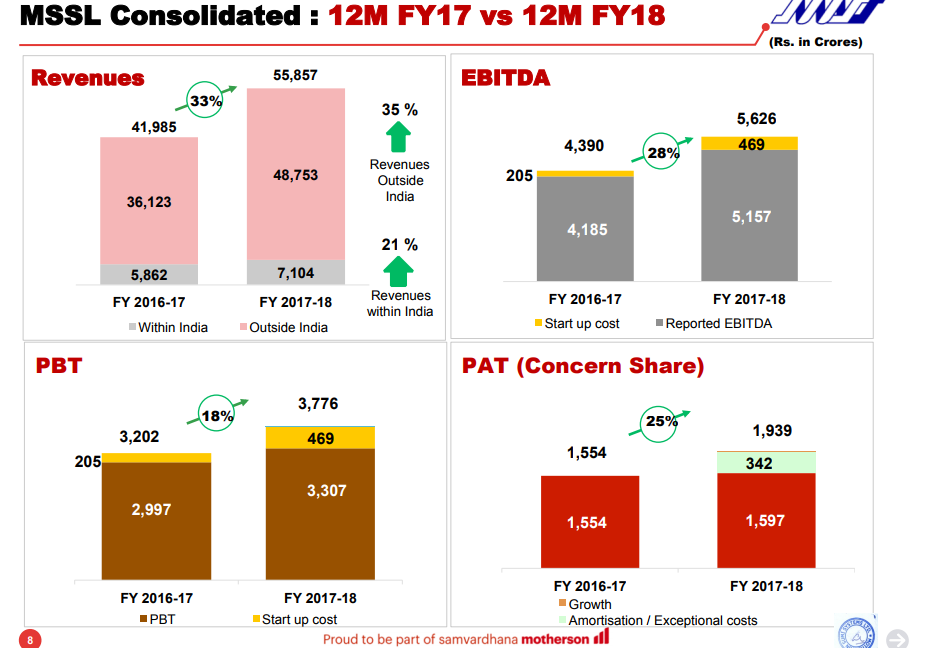

These are the right images to compare on the consolidated level.

Note that INR 518Cr PAT Matches (1597 for FY’18)

1 Like

First Quater Q1-2019 Results presentation:

1 Like

Recommendation of bonus issue. I believe its one of the all weather stock in my pf. Top holding.

1 Like

How does the bonus issue matter? In fact, I would treat it as a negative, a useless & irrational move.

Irrational of the market too, for the price to move up on the news.

Disc: Invested

1 Like

Absolutely agree.it has been announced only to prop us the share price as it is languishing around 300 for quite some time

1 Like

May be i have made very good money in the counter so i am biased. To make retailer react you have to think what matters to them and not to analysts like you, that is what i believe that this mgt thinks. I am invested from long past and know this strategy has worked well for the co.

very best, mukesh.

https://www.motherson.com/investor-overview.html

25 years of journey. Worth watching this video whether you hv invested in the co or not.

I am an investor and not an analyst.

5 Likes

https://news.yahoo.com/exclusive-motherson-sumi-early-stage-talks-leoni-over-153530971--finance.html

Another of those Technically sound European companies going under for an Asian company to buy. Motherson is a behemoth in its field and knows its business well. It will be a thumbs up for the investor.

Out of the 15000 Cr for value for 33 % stake , they have pledged for 240 Cr which is 1.6 % of the total promoter market value.

Some Red Flags

IS CHICKEN IS GETTING READY FOR SLUGHTING … ( I don’t know )

increase in number of shares ( Equity Dilution )

second last bonus Bonus 1:2 on 05-Jul-2017 Last Bonus 1:2 on 30-Oct-2018 ( What has company done in one year to facilitate the retail investors . This move is to increase Promotors stack only (I may be wrong )

Negative Free Cash From Last Three Years

Increase in Debt ( almost double n last three years)

TOO Much in News …

Aggressive Company Acquisitions ( 21 Company Acquisitions in short span of time )

As @S_Banerjee ( Could you please point out he source of information )pointed out Pledge of 1.7 Cr shares Pledges However I haven’t find any Corporate Announcements to intimation by company to NSE/ BSE

Disc; I haven’t invested in the company I am not any SEBI approved Analyst .One must do his own research before investing

1 Like

Sir, That is not equity dilution ! Bonus and splits don’t really change ownership.

1 Like

you are right sir but my sole purpose that investor must find out the reasons why they issue bonus What is the cooking behind the scene The Company hasn’t Run extra mile and won some accolades so that they should issue .

" Bonus issues are given to shareholders when companies are short of cash and shareholders expect a regular income. Shareholders may sell the bonus shares and meet their liquidity needs. Bonus shares may also be issued to restructure company reserves. Issuing bonus shares does not involve cash flow. It increases the company’s share capital but not its net assets." from Investopedia

Cost of administrating bonus share is higher than issuing the cash dividend However By no means It is the criteria to judge the future of the company

Regards

Motherson Sumi has been facing a lot of profit booking in recent times. But many fail to see that the whole auto industry is in turmoil globally.

I am getting a little uncomfortable with the increasing pledge of shares but studying the acquisitions gives me little comfort at the same time. Motherson Similar has diversified and holds a reputation as a quality manufacturer.

Most major investors would prefer to watch if the pledge of shares was worth the acquisition. Let’s wait and watch.

5 Likes

Surprised to see that this company is not very well discussed on the form. This was one hell of a wealth builder over couple of decades! Hats off to the management.

Motherson Sumi has corrected by more than 50% from its top now.

Checking if it is attractive at current PE ratio of 20-25.

Historically, the range of PE ratio for this company is from 20 to 50. So we are at the bottom of PE Ratio (not necessarily price).

What could be the reason?

- Falling Margins: If one goes through the conference calls, this is due to the SMP plants’ startup costs being accounted into PnL statement and also due to recent acquisitions like PKC & Reydel

- Falling behind in revenue target for FY20: Management assures in almost every conference call that they are confident of achieving it. Sehgal suggests they are very much on track in organic growth. And for inorganic growth, they are talking to lots of people and are confident of achieving their target.

What is the company’s next focus on? What are the opportunities which are opening for the company?

- Acquisition: As discussed above, a huge ticket acquisition is going to come up. This is going to be a distressed asset as that’s their style. Their focus would be to make this company efficient and integrate into the Motherson group.

- Technology: Motherson Innovations, a new wing is being led by Laksh Vaaman Sehgal. They also opened a new office in SF Bay Area. They are going to focus on tech-oriented value-additive products for the car.

- Polymers: SMP is the biggest business for Motherson. Most of the company’s growth is being driven by SMP. This also has bright future as manufacturers are focussing more and more on manufacturing fuel efficient cars. Even EVs are anticipated to replace more of metal with polymers aka Engineered Plastics.

- Wiring Harnesses: Penetration of wiring harnesses is going to increase in standalone earnings due to BS-VI transition. In cars, it is going to increase by 10% to 15%. But in 2W, it is going to increase by 2.5x to 3x. EVs in Western countries will also be a big opportunity here.

Management:

I love people who are target-oriented, number-oriented and growth-focused. Motherson’s management exactly fits into the picture. The management always speaks in terms of numbers instead of using simple adjectives which can be easily played around.

The company also doesn’t have succession risk as junior Sehgal is super-trained by his dad with the risky Visiocorp acquisition + turnaround lead by him during the financial crisis. One should read through the Visiocorp acquisition story to understand the commitment and capability of the management!

Working Capital Cycle:

Consistently shortening over the years.

Almost close to zero days.

| 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Inventory days | 25.8 | 25.8 | 42.4 | 39.0 | 38.9 | 37.0 | 55.0 | 44.9 | 35.0 | 80.9 | |

| Receivable days | 36.2 | 39.1 | 32.6 | 31.3 | 38.4 | 41.8 | 73.6 | 41.4 | 39.8 | 81.1 | |

| Payable days | 58.3 | 61.3 | 52.4 | 50.6 | 48.5 | 45.2 | 75.7 | 48.5 | 67.7 | 163.9 |

This speaks of the company’s product quality and its bargaining power.

Risks:

- A huge acquisition is coming up.

Management targeted revenues of $18 billion for FY20 and this year, they just achieved $9 billion. Going by organic growth, they might reach $10-11 billion next year. So a huge acquisition of $7 billion is going to come up this year. Though the company has excellent track record of acquisitions, one still needs to be careful as management might take some wrong decision in a hurry to achieve its revenue target of 18 billion USD. Well, ego can come into picture! However, declaring a dividend yield of 1+% with such huge acquisition coming up also gives some comfort that the management can handle it. They also declared dividend during their Visiocorp & Peguform acquisitions. - Margins might fall further.

If Motherson buys a company which is almost 50% of its size (in revenue terms), I’m sure it is going to be a distressed asset. And distressed assets take a toll on margins. However, if you look at Motherson’s track record, they have always managed to increase their margins back to 5% over the years after acquisitions. After acquiring Visiocorp in 2010, margins fell to 3.2% but however they regained margins to 5.2% in just an year. Similarly after acquiring Peguform in 2012, margins fell to 1.3% but again margins were regained to 5% by 2017. It is important to note that 4x improvement in margins => 4x improvement in EPS. - Poor growth in car sales.

This question is repeatedly asked by analysts during the conference calls and Sehgal repeatedly replies that their focus is on increasing content-per-car. - Very complicated to understand the company.

Lots of businesses. Lots of acquisitions. Lots of plants. Complicated holding structure. Easy for the management to cook the books. However, trust on the management comes from Sumitomo Wiring Systems being a secondary big shareholder. They have also recently increased their stake in the company via Preferential holding. This gives more comfort. Mr Sehgal is a self-made adamant billionaire. You can’t really be adamant if you are a cheat / crook.

Discl: Interested but not invested. Might start a position. Not a buy / sell recommendation. Not a SEBI registered analyst.

15 Likes

I think one big negative for this company is - it is in auto component sector with hardly any aftermarket sales. This means company only deals with large OEMs and hence do not enjoy any pricing power (like all other auto component companies).

Hence I prefer to stay away from auto component companies unless they have huge technological moat like Bosch or have substantial (25%+) aftermarket sales like tyre or filter companies.

Please find my presentation on Motherson Sumi at ValuePickr Chintan Baithak 2019.

We might have a huge compounding opportunity depending on the acquisition they are going to make in this FY.

1 Like

Good presentation

Couple of Points in Risks that you may have missed on which mkt is worried

-

Trade War- Tariffs of Cars being exported from China. Infact MS facing issues in bringing ppl from Germany (source Q4 concall). MS has couple of plants in China.

-

Mgmt is always very vocal on ROACE but it is falling constantly. Hopefully it will improve now with all capex done

-

Debt/Equity ratio. Acquisition is fine but any highly leveraged business when growth slows down, things become worse …MS mgmt reduced some debt in Q…

Thanks for your comments.

- I think the issue was on bringing people to US Tuscaloosa plant, not China. They gave this as a reason on why startup of that plant is slower than expected. May be I am wrong and can rehear the call.

- Agree. I discussed this during the presentation but didn’t put it as a statement as such. Not just the plants, we need to wait for the new acquisitions like PKC and Reydel to turn around too.

- Fully agree again. Hence waiting for the acquisition to finish and me to analyze it.