The facilities look small. But at least they are neat and clean…and most importantly GENUINE .

3 good announcements today

- lot size reduced to 1000 from November

- one of the first companies to give result date…11/10/17

- to consider dividend also. Very positive.

Q2 results out… interim dividend announced…shareholder friendly…

good topline and bottom line growth seen… yarn division contributing to topline though its only operational from July 17… only thing bothering is the increase in receivables… any one has any insight on this?

disc: invested

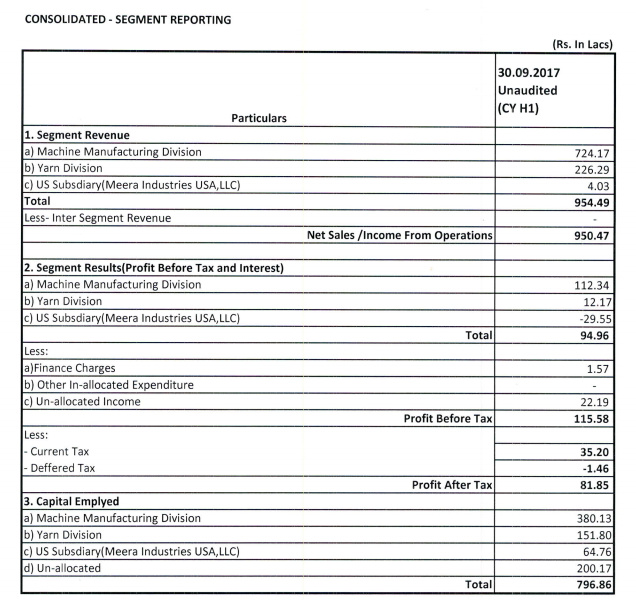

The results for the half year ended 30th December 2017 are in tune with what was stated by the company during and after the IPO…Sales at Rs 950.47 lacs are up by 36% from half year Sep 16 . Expenses have increased by only 26% at Rs825.96 lacs indicating the company’s control in containing costs . There is an impressive growth at Rs 111.46 lacs up by 150% . Very very impressive indeed for a startup like company. I feel it is worthwhile to go back to the AR2007 of the company where the directors in their report have clearly specified " that they believe that the improved financial results are directly attributable to the R&D activities of the company " which is very rare indeed for Indian companies let alone a start up . I believe that it is these qualitative factors that would ultimately lead a company to Blue Chip status .

The company has been one of the first in announcing half yearly results. Having declared a dividend of Re 1 earlier and again declared one more interim dividend of Re 1 now, I see that they have adopted a generous policy in distribution of profits to share holders by way of dividends which again is a positive.

The earning per share for the half year Sep2017 is Rs3.1 which is almost the same for the whole of FY2017. While the share looks well discounted at more than 25x the trailing earnings considering the growth ahead from a very small base of Rs 13 crores sales for FY2017 I feel that the company is reasonably valued .While analyzing the company i have not taken only the stand alone figures into account since the operations of the US subsidiaries seems to have not yet stabilized .

Note: I am invested in Meera .

1 Like

typo : Re read as "There is an impressive growth in profits at Rs 111.46 lacks - up by 150%. Please read AR 2017 instead AR 2007. I regret.

It is hard to watch a stock increase in value dramatically while you are still on the sidelines analysing it. I know, I know, It is better to be late than be sorry.

So I was having a look at their impressive, non-fluffy 2017 AR and found two numbers (inventories, Trade receivables) jump out because they have increased from the previous year. As the company grows, I would expect these numbers to reduce and not increase. Any thoughts?

as a former sheep, I am new to value investing. Could someone tell me how I can find YoY growth in order book?

Appreciate your help.

Disc: Not invested.

2 Likes

The Meera Industry Stock has increased dramatically, but that is in response to business developments which have occurred in Q12018 and Q22018. These are stated by company filings at BSE. The Annual report does not capture those developments.

Can’t one expect Inventories and receivables to go up as business grows? Inventories+ Receivables totalled together are just Rs 223 lakhs (123+99 lakhs), these are still less than 20% of enhanced turnover of 1346 lakhs for FY17. I am not an accountant to comment; but are there any norms for these numbers?

One red flag for me Profit in 2016-17 , 1 Cr and Promoter salary including commission 42L around

Me and some friends visited the company today

- I was amazed to see the factory setup and thought process of the promoter Dharmesh Desai

- Currently operating from 40k sq ft. Can go up to 3-4x fy17 revenues on exisitng facilities…ie upto 50 cr revenue.

- Can double capacity by additional capex of 10 cr (already has vacant land land for that at the existing location)

- Major competition from European oems

- European machines cost 6 cr per machine. Meeras will cost substantially lower. To be fair, European machine will have some higher automation.

- Meera operates in the gap between the costlier European (high end) machines and low cost low end jugaad machines.

- Dharmesh Desai used to work with Garden Silk for 6 years. Used to work in yarn twisting divn there. Wanted to do something of own. Started with only 8000. Very hands on promoter who was able to answer all questions about the company and the industry. Found him very level headed and sorted. Thinks big and seems to have the ability to scale up.

- Very well maintained facilities for a 15 cr revenue company. Has implemented SAP and automated storage systems…punching way above his weight

- Meera is mainly into machinery in filament yarn sector. Lakshmi machines more into spinning sector.

- Only one sales agent in the US. Will ramp up as scale improves.

- Asia africa Europe are major exports markets.

- Technical textiles, carpets, stitch yarn (quilt yarn, footwear) are the major application segments.

- also makes machines which can make niche items like medical sutures, bandages, parachutes, nets, bullet proof jackets and harnesses

- 50-60% repeat customers. Every 2-2.5 years the existing customer will come back for more machines. 5-7 years is obsolescence cycle.

- US subsidiary should breakeven in fy18 itself on full year basis.

- Yarn mfg divn is more to showcase their machine capabilities…but will be run as an independent profit centre. Focus will be to improve profitability through high end yarn sales. Scale will come later. Will keep yarn up to a certain extent of revenue.

- Craftsman storage systems - storage machines - this has halved the inventory

- All overseas invoicing in $. Usually they build in forex risk into the price. No separate hedging policy.

- 100 employees

- all machines are made only against confirmed orders and on receipt of full payment/ lc. Receivables shiwn as lc date not due. Yarn will have 60 days credit period

- to give u an idea of the quality of the co…they use 3d printers to develop prototypes for future launches. Design team looked capable to deliver innovative products

- many new processes developed by co which will soon be patented

- unique promoter who is keen to share with his shareholders . For example he gave 1 rupee dividend to post ipo shareholders based on pre ipo results. Unheard of. Also exemplary is giving consol results in half yearly numbers ( not mandatory ) and that too by 10th of the month, with an interim dividend amounting to 40% payout thrown in for good measure.

If I had made this visit when price was 40 (16cr mcap)…i would have picked up high % of equity in the co. Big Big miss for me

Stock is 4x for me in 3 months. This is in no way a buy call and shouldn’t be interpreted as one.

Disclosure : own . Since my holding amount is in public domain…not giving % of pf details.

8 Likes

Hi thestocklady,

The Book value of the company is just 9rs , and CMP is 200 ? Why it is so expensive ? I am new to investing but how do a person see value of a company with book value 9rs to 200rs ?

Modern day investors prefer high roce cos…and one essential ingredient for that is a lower book value. This means that the promoter is able to squeeze the last drop out of the capital he has put in.

Hey Utsav, looks like the SME segment has become a happy hunting ground for you. Wonderful picks. Agree with you that this provides an opportunity to do PE kind of investing. In the main exchange, all the IPO’s that are coming through, the big issue is that the real money has been made pre-IPO by the PE players. In fact, if you look at the data, 80 percent of the IPOs that have come in over the last 2 years are basically PE exits.

In that sense, its a great strategy to focus on the SME segment for PE kind of investing and multibagger returns. Great Work. Cheers!

1 Like

Good news for Meera shareholders. Company has announced an order from USA office.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/c3fad6a3-962a-41e7-b86d-0897caff91a8.PDF

While the order size is only 160000 USD, its significant for multiple reasons.

- With this USA ops become fully operational

- Augurs well for further business and we may even see USA office turning a small profit this year

- Most importantly, it is a great achievment for a small co from Surat to go and win a machinery order in USA. Here, many other factors other than price come into play.

Disclosure : Increasing position with each trigger

3 Likes

I had a look at the document and only thing I can find is the below table which breaks down of revenue from subsidiaries. Over here the earning from the US unit is 4L and it is making a loss of -29.5L. For a new unit these numbers are understandable but I am keen to see the $160K order in there. Could you please specify the page number or paste the section of the document for us.

DiscL Not invested.

my bad. I attached the wrong file. The right file is now attached

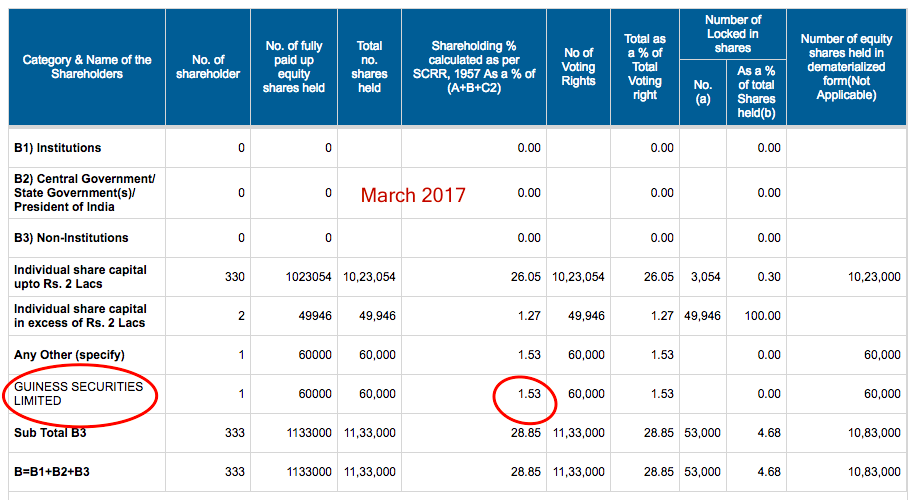

This seems to be true in latest shareholding pattern they disappeared …

http://www.bseindia.com/corporates/shpPublicShareholder.aspx?scripcd=540519&qtrid=95.00&QtrName=September%202017

judging by the chart in 6 months they must have made good profits …

PS: this link https://www.outlookbusiness.com/the-big-story/lead-story/a-lot-of-hot-air-1563

was really an eye opener for me … Everybody should read it.

Be careful with your hard earned money.

Wrong analysis. Guiness sold most of his stock at 39, so clearly he hasn’t profited from the rise.

It isnt fair to paint all companies with the same brush. As a market maker, he has to provide 2 way quotes for a period of time. If you check, he has bought at 191 also.

I request you to see the performance of the company and leave the valuation etc to the vagaries of the market.

1 Like

Meera recently announced completion of an expansion. Clearly a company which punches above its weight in terms of planning ahead for the future.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/d77f6648-fd4e-4d31-b2f5-5dee09a012ff.pdf

mcap today : 120cr

disclosure : increased shareholding in q3

2 Likes

its hitting UC every other day…it may be overvalued based on trailing nos…PE,PB…but may be the expected growth and expansion is what is driving the price…not sure if I should sell part of my holdings now or should i wait?

disc. invested since IPO

Best to follow your own judgement where selling is concerned.