This counter have very low float and looks expensive on every aspects.

Is there any timeframe when it’ll be listed on nse & bse

This counter have very low float and looks expensive on every aspects.

Is there any timeframe when it’ll be listed on nse & bse

free float should be 25-30% based on non-promoter holding;which is comparable to many promoter held firms; float in terms of no of shares may look low but that is also because the no of shares of the comp is less; in terms of listing in nse and bse, i dont think it is a stated agenda from the firm though logically considering their expansion and progress that should be their target;

tTalking to one of the investor I was told 18 months before we can buy single shares.

rules for main board listing

Meera is still 18m away from main board

http://www.bseindia.com/xml-data/corpfiling/AttachLive/00a5298c-8564-4223-ba4d-b4c5470e568e.PDF

Developments as per the board meeting dated 8th Feb 2018 of the company

I feel the above steps will greatly help in expanding the markets in scope and size over the present small base of Rs 13.71 Cr in sales - FY 2017, and present market cap of Rs 149 Crs.

The significant pointed to be noted here , in my view, is the existing sales being small at Rs 13.71 crores for FY 2017, any meaningful improvement in sales and profits will possibly take the company into a higher orbit in performance which is likely to be appropriately discounted into the share price in future.

I am holding on to my shares in Meera Industries for a long long time to come.

I post here my comments made recently on moneycontrol board with some additions as appropriate

mssmurthy

The company has to day intimated BSE about an order received from Indonesia for USD575000 for the supply of Twitter/Cabler Machines for carpet yarn and that the order will be executed first half of FY2018-19. The company is expecting to receive further orders from the same customer.I see that this order alone would add about 5 to 10 percent growth in earnings of Meera Industries for FY2018-2019. I also see that this is one of very few companies out of SMEs listed in BSESME platform which has performed very well by virtue of quality of earnings ,

One, potential to grow over a small base,

Two, High margins and high return on net worth at 40 percent plus, Three,moat by technology and innovation,

Four ,diversity of customer base,

Five, liberal dividend policy,

Six, burning desire on the part of the young promoter to surpass their self imposed target performance.

After having multiplied many times since last one year the share price has recently come down by about 40 percent which is understandable as it is still several times from the Rs 40 levels prevailing 10 months back .

I continue to hold in anticipation of better performance over next three years at least .

https://www.bseindia.com/xml-data/corpfiling/AttachLive/6EB33240_1769_43EF_B5F9_0144E3AA003E_134155.pdf. Results of Meera Industries

The results are in tune with the interview of the promoter with Bloomberg which was reported earlier here in this group.The sales revenue at Rs 21 Crores and net profit at Rs 2.65 Crores declared in the results for FY2018 are in synchrony with what is stated by the promoter in the above stated interview and lends credence to the same .If we are to go by the same interview the promoter expressed confidence about a better performance by the company in FY19 at Rs 35 Crore in revenue and Rs 4.5 Crore profit which I feel he would be able to achieve due to increase in the number of clients from different countries and broad basing the range of machines and marketsI believe that the increasing sales coupled with increasing range and market , high margins,lower base level of the business as on date, offers good scope for appreciation of the share value over next few years. While the EPS for FY at Rs 6.9 indicate a higher discounting , the high-margin, low-base, high-ROC, combination gives me confidence in this small and nimble footed company promoted by a young technocrat with a transparent business model.

I am invested in Meera and continue to hold for Long in anticipation of a good performance in nest few years.

Minimum quantity is reduced to 500 from today (earlier 1000).

http://floorplan.messefrankfurtusa.com/ttna/exfx.html#listCn

MIL name is not there in this list of exhibitors. I own a fund which invests after deep analysis. What is the address of the company in USA? Who is running the show in USA?

There is a lot of fake news circulated via whatsapp and the company may be doing this…

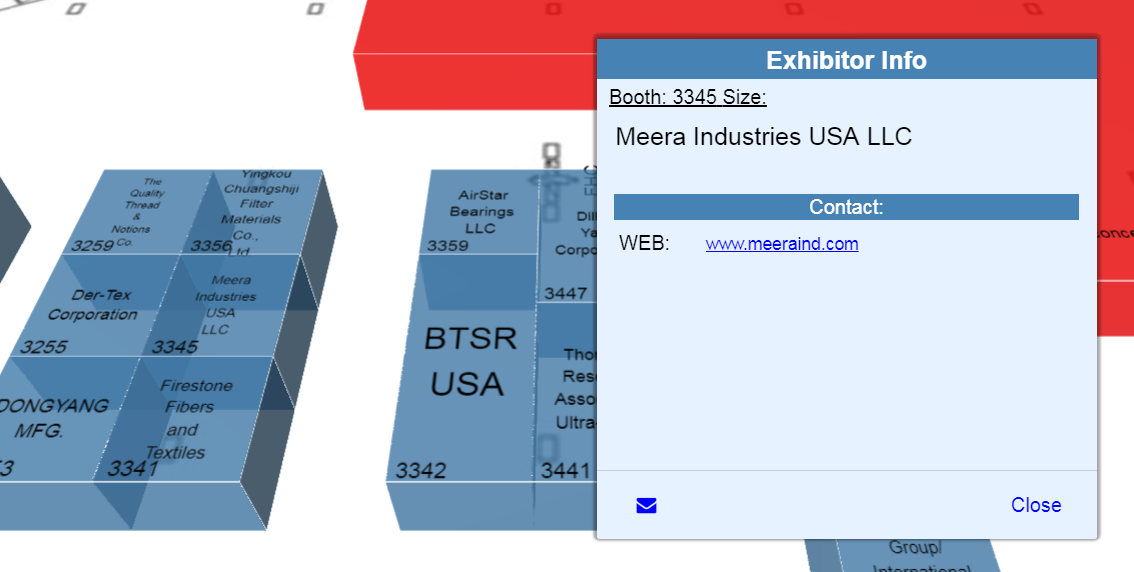

Hi, I can see Meera Industries in the 2018 list, number: 3345

As @rajsuccess mentioned, Meera industries is present in the 2018 exhibitors list (no: 3345) of the links you pointed (see below image for that). Also, the US mentioned in their website (meeraind.com) in contact/enquiry section clearly. See attached image for the same.

Disc: Not invested but tracking.

Since your company invests, any updates on your analysis of Meera Industries? Please share

Rajsuccess,

Before I respond to your query, I would like to thank the valuepickr forum member who pointed me to the right stall-345 for MIL. My oversight was a problem.

Some questions I have:

Apart from the statements or letters released to BSE, I would like to see the actual success these projects have demonstrated - Proof is in the pudding.

The equity capital is 29 million which is too small. It is very easy to play around when the promoter holds most of this.

The share price has increased exponentially from 30 to 390+ and dropped to 176 and again is currently at 249 which does not give a level of comfort to a true investor. All this in less than a year or almost a year.

IF THE COMPANY IS GENUINE, THEY SHOULD SHOW TRUE CUSTOMERS AND THEIR VIDEO ON THE SITE RATHER THAN BSE STATEMENT RELEASES WHICH ARE NEVER AUTHENTICATED.

4a) I would request the management to have an analyst meet or call.

4b) Site visit to the company - Meera Industries Limited

4c) Provide the contact coordinates of the foreign customers from whom we can confirm the details.

Based on that, we can decide the next steps.

I know this may not be what you intended to hear from me, but since this is a first gen promoter with unproven credentials, I would be circumspect before parking my money.

Still one question which perplexes me is: Why are they getting export orders and not many orders from India. We have a big textile sector.

Coincidentally IPO of Meera Industries was managed by same kolkata based Lead manager “GUINESS CORPORATE ADVISORS PRIVATE LIMITED”, who managed SME ipos of many fraudulent companies barred by SEBI for price rigging. See below link:

no fundamentals stock went up like balloon , As if merchant bankers don’t know how to price IPO.

Clearly many SME stocks are operator driven.

Meera Industries have posted a good result for the latest half year . What I have been observing during earlier quarters was that soon after the result was posted and discussed by any member on this ValuePickr board immediately a negative message is also posted with unfailing regularity .So i have posted the link of the result from BSE and waited for a while before commenting on the result .As expected the a post has appeared from Mr Grohal which I have gone through before writing this . I beg to differ from the implication of Mr Grohal that Meera Industries is not a genuine company like some others which we have happened to see in the SME boards . The promoter Mr Dharmesh Desai is an young engineer from MIT Surat and having about 20 years experience in product development and innovation a reputed textile mill like Garden Silks . As a small investor in stocks for more than 40 years I find his credentials and those of the other directors who are qualified Chartered Accountants and Cost Accountants are good enough for investing in this budding company .

As for the results for the latest half year I find that the company has been able to maintain a consistent growth of more than 40 percent , with an increased margin of 17 percent on revenues . The sales have consistently grown from Rs 13 Crores for FY2017 to Rs 21 Crores for FY 2018 which is good. From the results of the current half year I expect the company to register sales of around Rs30 Crore with a commensurate increase in profits.

I feel that since the present base of sales is small at Rs 21 Crores there is a lot of stream for future growth . The declared payout policy of disbursing 40 percent of net profits as dividend plus dividend tax is favourable to investor and also indicative of good cash position .

Every SME company should not be painted with the same brush. Meera’s continuous sales/profit growth shows that its a genuine company and doing things right. Couple of investor friends met promoter and visited facility, according to them promoter is passionate, they have good enough capacity and operating leverage is yet to play out. Company is tapping international markets. I think, considering the potential its quoting very cheap.