What i think is you have to think in terms of what fraction of cost of trade is taken by exchanges ? If its insignificant then BSE & NSE won’t be able to attract anyone by giving it even for free.

If the cost is significant then you will for sure going to see a trade war, what we saw in telecomm with jio ( market share can be gained by giving it away for free). It’s hard to tell but if this happens then other exchanges have nothing to lose (Cost of setting up & running is nothing for BSE - said in conf call) and MCX has everything to lose.

Can anyone list down step by step what is the process n skills of 1. Running a commodity exchange 2. Participating in trading on a commodity exchange. I am sure it is much different from an equity stock exchange. I think a detailed understanding of this will clear lot of doubts. The least I ve understood is it’s not as simple as it looks . Things like ware house mgmt r different from equity. Would be glad if some one can provide detailed understanding

I can’t deny but I think pricing matters less. Volumes bring liquidity, if volumes are less, spread will go up. Traders will lose more on spread. If this is that easy, why NSE is NSE ? I think market will increase with new entrants. If market share has to go, it will go slowly slowly with time. In this time consolidation will happen in industry as a logical conclusion as MCX shareholders will not give up that easily.

I think, full merger with NSE is logical conclusion to save business.

Here i think MCX is playing with great master strokes. The permission for which they are asking for future contracts will get them into monopoly at an international level. Their plan for setting up spot exchange is tough too after NSEL scam but still there is room for success keeping in mind the market share. Besides this, @AmitContrarian i think having a good team & HR is also a great cost(for BSE) for the business especially like MCX India. Also looking at the volumes i think it will be tough for BSE to compete further.

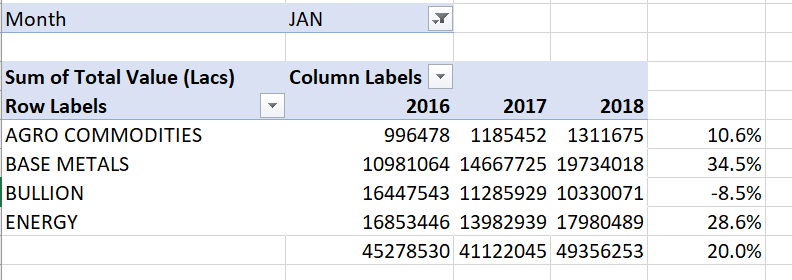

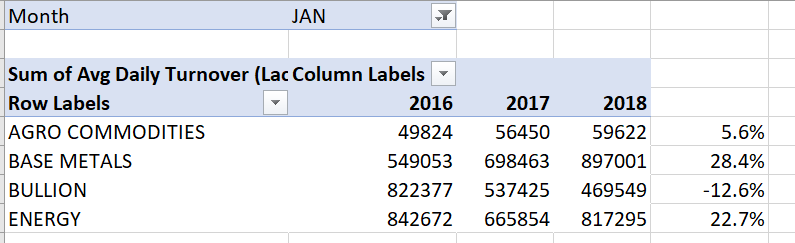

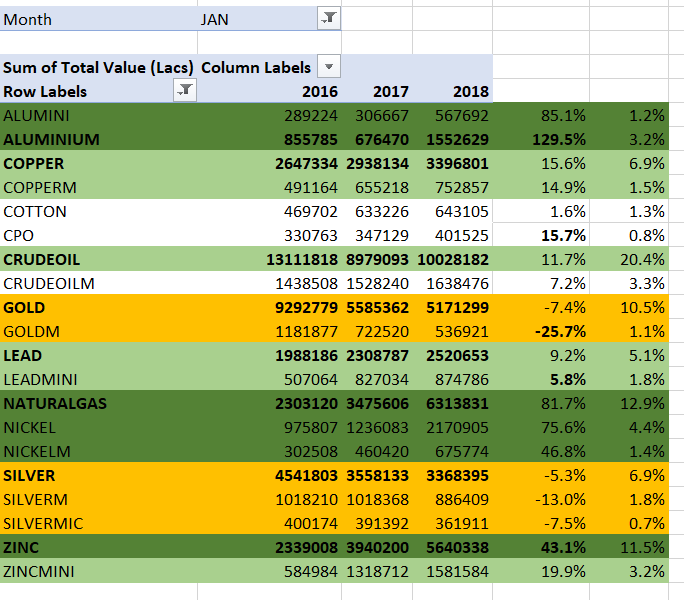

Sometimes i feel is purpose of such articles is to hide the big positives and create more panic. Gold is one of the many items traded on MCX. If we see January data, almost each and every segment has shown good double digit YoY growth on all metrics including ADT,TC,TV. Considering the low base impact of demonetization and now slowly impact of GST going away, look like 20% YoY growth should be on the cards.

Some numbers to chew from MCX website itself for Jan’17 vs Jan’18:

Disc: Recently invested and accumulating. Yet to find lot of answers

Edit: Above point was just to highlight many times media give extreme n sensational news on either side without balancing things. Nothing against the content.

There’s a lot of respectable value investors on this thread who are invested in this business. But I just can’t shake off the feeling that MCX is a great short. With only 1% delivery based trading, it really doesn’t have any moat. From October, BSE will attack with all its might to gain new business, and MCX has to protect it’s existing business. Its either win-lose or lose-lose situation for BSE-MCX respectively in the near term.

Once BSE establishes it’s commodity trading, one can hypothetically shut down MCX and all trading will seemlessly move to BSE from the very next day. Why will anyone miss MCX?

Another aspect of the commodity trading segment in India is how much of it will develop in IFSC, which has no CTT, STCG, STT, DDT, and foreign currency denominated contracts etc.

With FPIs being allowed entry into commodity trading in IFSC, it could be a good tailwind for the business to develop in IFSC. For AIFs the initial battle will be between impact cost of liquidity and tax benefits from shifting to IFSC.

This just has the 2 days of data. Looking for historical. Could not find anything in their Feb. investor presentation and annual report which was last years.

Over years BSE has managed to gain market share and become the leader only in markets where network effects hadn’t set in e.g. currency derivatives, or the business itself was new.e.g. BSE starMF

The case of MCX seems to be different because, I think most of the players who would trade are already doing so on MCX and network effects have already set in. The ones who might shift to BSE will be HFT firms and speculators who are happy making money through price movements in points. However, they also need liquidity which might lead them not to shift to BSE.

Also, BSE’s liquidity enhancement schemes to gain share in cash and derivatives haven’t worked in the past.

I think given the past experience it might be quite difficult for BSE to attract liquidity unless it first creates some fake liquidity which attracts true liquidity.

Agreed with you. If we see the current valuation we are getting core business at 2000 odd crores after deducting cash and cash equivalents. Just take the quarter of march 2018, where MCX has done business of near about 15 lacs crore. So which will translate into the revenue of Rs. 75 crores. Expenses are majorly capped at 50 crores. so this brings PBT of Rs. 25 crores (excluding other income, Cant estimate the other income as dont knw as of march where investments are made… but can take other income near abt 25 crores on a conservative basis which can give pbt of 50 crores after considering other income). Seeing on a yearly basis this translates to 100 crores on 2000 crores valuation. Just a 20 PE for an exchange with such amazing growth aspects even entry barriers in the business and all sort of things. I think it has fantastic moat and it is very attractive at current price. Now attractive part lies here… If we assume 25% growth in sales i.e. sales of 94 crores on a quarterly basis their expenses are nearly capped at 50 crores, additional sales wont increase their expense which is interesting part of this business it gives PBT of 44 crores so 25 crores turns into 44 crores… now when we take 44 to an annual basis it turns out to mouth watering 176 crores on 2000 crores valuation. So when growth comes in sales profit is going to grow exponetially… I dont think bse can take existing business which is of futures because of ban on liquidity schemes and sort of things … Chances for bse are remote on existing future contracts… As far as options are concerned this can be a sacrificing area for mcx . chances are high over here… But at current levels and looking at current business forgetting options available at very attracting price with great risk reward ratio…

Discl: Invested from lower levels still accumlating… These are just my views and it can change over time and date. Request you to do your due diligence before taking an investment decision.

This operating leverage is double edge sword. If volumes drop, profits will plunge.

Disclaimer -Exited after remaining long term investor for 3 years. Watching the business to see effects of BSE.

25 Crores per quarter is excluding other income which gives yearly 100 crores. For Quarter ended March 2018 from the data available in the public domain my estimate is Revenue excluding other Income at 75 Crores. Expense near about 50 crores which gives PBT from core operation at 25 crores.