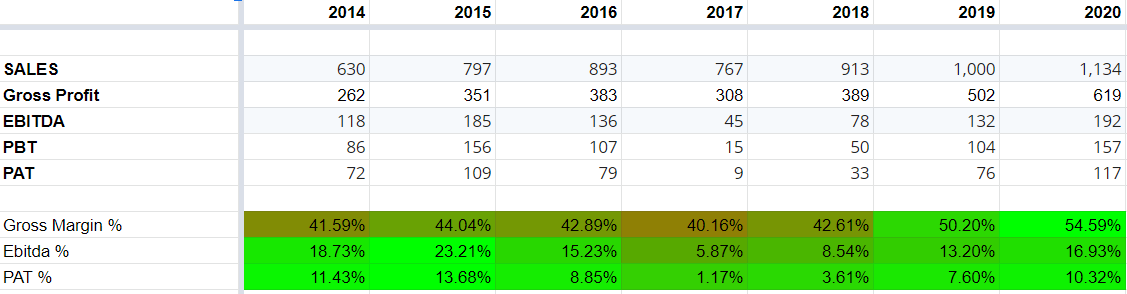

Company has shown good growth last year in both sales and margin profile. Growth has come majorly from products like Ibuprofen, Paracetamol and Naproxin. Company does not spend much on R&D.

We have established our foothold in diverse therapeutic segments, such as Pain Management, Cardiovascular System (CVS), Cough & Cold, Central Nervous System (CNS), Anti-diabetic, Gastrointestinal, Anti-Allergic , Antibiotics & Oncology.

First time sales in Anti Cancer segment of Rs. 16.74 cr.

Anti Allergic sales increased from Rs. 8 cr in FY19 to Rs. 32 cr in FY20.

Share of OTC to Rx changed from 50.95% and 49.05% in FY19 to 54.67% to 45.33% in FY20.

the formulation business in the UK registered a growth of 23.5% in FY 2019-20, adding Rs. 510 crores to our revenue share. A strong product pipeline and successful launches every quarter helped us to consistently retain our dominance in this vertical. The US and North American business too reported growth of 6.1% with revenues of Rs. 436.4 crore. Further, revenue from Australia & New Zealand stood at Rs. 140.7 crore in FY 2019-20 and Rs. 47.4 crore from the rest of the world.

In FY 2019-20, expenditure on R&D amounted to Rs. 8.3 crore and with our team of over 50 talented and experienced scientists, we continue to pursue specialisations for new drug delivery systems and other formulations.

Our newly commissioned state-of the-art R&D center at Navi Mumbai aims to cater to hitherto unmet therapeutic needs and enhance the Company’s responsiveness to file more ANDAs.

Capex

During the year, we further incurred capex of approximately Rs. 59 crores, spread across the facilities in India, USA and UK.

We continue to increase capacity at our India plant by putting in new manufacturing lines.

We have also invested in creating a robust warehousing infrastructure in the US and UK in FY20

UK Market

We feature among the top 5 pharma companies in the UK and our subsidiaries, Relonchem and Bell, our wholly-owned subsidiaries, strengthen our presence in the region.

While Bell contributes to an OTC portfolio of 150+ products, Relonchem contributes to a high-end RX portfolio of over 100 products.

We have robust portfolio of 50+ products in the pipeline, at different stages of approval & R&D in the UK market.

Company also provides contract manufacturing and research services to some of the top pharmaceutical companies in the EU region.

Partnering with major retailers in UK including AAH, Lyods, NHS,Tesco, Asda, Morrisons, Coop, Boots and Superdrug, among others, the Company addresses therapeutic segments across pain management, diabetes, cough and cold, neurology, cardiovascular, and hormonal treatment.

US Market

In an effort to expand our offerings in the US, we acquired Time-Cap labs in 2015 and it strengthened our position in the strategic US pharmaceutical markets.

Our presence in the soft gel category favourably positions us to drive better margins and our dominance in the OTC as well as RX segment allows us to further extend our offerings in the US market.

We remain focused on capitalising opportunities in the US pharma space by introducing 4-5 new products to our US portfolio every year.

With 6 new approvals on the way, in US, we expect to improve our revenues significantly in the near future. The integration of our US subsidiary is now complete, with the business on track to achieve its objectives.

The Company is amongst the few active Indian companies that have a USFDA approval for generic soft gel capsules. Therefore, the Company enjoys a strategic advantage in the world’s largest market and limited competition in the region, resulting in higher margins in the soft gelatin capsules segment in the US generic business.

Australia & Nz

We conduct business operations in Australia and New Zealand through our subsidiary, Nova Pharmaceuticals. Nova Pharmaceuticals is one of the leading generics and private label suppliers in Australia and has partnered with the leading retailers & pharmacies in Australia, like Woolworths Ltd., Coles Mayer Ltd., Aldis, Metcash and Fauldings.

Looking at the size of the market and the growth opportunity it offers, we are optimistic about our growth in the region.

ROW

After pioneering in the regulated markets, we expanded our presence into emerging countries targeting four major clusters such as South East Asia, Russia and the CIS, Middle East and Africa. In these four clusters, we are focusing on specific countries like Iraq, Kenya, Ukraine, Sri Lanka and Myanmar. We have already started filing for approvals in these countries.

Outlook: We are strengthening our presence in these target markets and we expect to generate 10% of the total revenue by FY 2021-22.

Marksans AGM was held today a few hours back.Only people who had written in earlier or who had asked to be “speakers” were allowed to ask questions.Live chat was disabled.Some highlights:

-> Company has “evolved” over the last 3 years.This is reflected in the debt free,cash rich balance sheet.Marksans is planning to increase capacities.Might commission a new plant as well.

-> All subsidiaries are adequately integrated now.Dividend payouts can rise.Buyback decision depends on the cash reserves the company has(didn’t seem too eager for this)

-> US market is weak for Marksans because company has a very limited product portfolio.Company plans to increase filings from this financial year.See US as the next growth driver.Operating leverage should start kicking in from this year,helping OPM.Expecting much better profitability from the US market over next few years.

-> Plan to take R&D to 3% eventually,of consolidated revenues.Company believes this is the right time to invest for the future.

Overall,Mr. Saldanha seemed a bit hurried and didn’t want to take even the questions that were sent in by shareholders who were not live.He eventually answered though,after the CS’ nudge.

@ayushmit Sir , got to read you are tracking Marksans ( not sure though) , but incase true can you please share your notes on Marksan’s turnaround prospect ?

Looks like continues business momentum. Big beat on all operating metrics + cashflows. I wonder how have they been able to growth GM% yoy any views? I thought the OTC markets would be more competitive.

Stock had been consolidating since 3 months even as many smallcaps were flying.Earnings have continued to be strong,balance sheet is strong as ever(150cr. net cash) and valuations are also very supportive.There is some lag effect between cause and effect.Not necessary that stocks will react immediately to good news or bad news.I think what hurts the stock is the poor visibility of the top management and an overall lack or absence of transparency over the years.Otherwise,this should do well from here as well.

I have been tracking this name for the last few quarters and i have a few basic questions if anyone can help answer:

a) This is a 1000 crore topline business and spends just 8 crores on R&D. Even though there is fair bit of OTC on it’s portfolio doesn’t that seem on the lower end?

b) What has been the reason for this sharp increase in GM% ?

c) Their UK business is gaining business momentum in 2020 (and continuing in H121) so have they dislodged someone within this space (since the organic growth in market is low single digits). What is the competitive positioning of the business in the market place? Can someone take Marksans share?

d) I understand their strong technical focus on soft gelatin tablets as core moat. It’s just hard to imagine none of the large guys do not want to enter this space.

I can assure you that soft gelatin as a moat is more of a PR than anything.A quick google search will disprove the hypothesis that Marksans is the specialized pharma in this formulation.

Harshit, results tomorrow…topline + margin expansion will help do wonders…but with UK being hit hard with second wave in Dec and much of US also under pandemic, not sure how this would impact volumes. Also any red flags on the USFDA that you are aware of? Anything on promoter quality / governance?

Very good results from Marksans. EBITDA margins are at 25% now,GMs have surged too in Q3. Net cash of 199cr.,up from 154cr. a quarter back. US business up 45% for 9 month period.Management had mentioned they will do well in US markets at their AGM.

Find investor presentation here. Seems they are getting back on track after a long consolidation and correction path. Once UK and USA opens up from Corona lockdown this may start showing good growth:

Given the challenges in preparing Softgel formulations plus other economic, technical and patent constraints there are not many players in this segment. Marksans has filed softgel products in all major markets including USA, UK, Europe, Canada, Australia & Russia. Of this, US alone is potentially a USD9 billion market

6 ANDA pending approval

Marksans’ Goa facility has a capacity to turn out 2.4 billion softgel capsules per annum, and has all the necessary approvals by USFDA, UKMHRA, TGA & other key regulatory authorities.

The UK & EU pharmaceutical market is estimated to grow from ~USD 468 billion in 2016 to ~USD 585 billion by 2030, at a CAGR of 1.6%, driven primarily by a robust life sciences industry. Marksans is among the top 5 companies in UK. UK business is driven by its two subsidiaries, Relonchem and Bell. Bell has a strong OTC portfolio with 450+ OTC/SKU products and 50+ products in pipeline. Relonchem’s portfolio comprises 162 MA’s.

Company has 50+ products in the pipeline in different stages to cater to UK market. Company is awaiting approval for ~20 MAs in the UK market.

Working on receiving USFDA approval for Southport facility(UK) to commence exports to USA. Company also plans to acquire product licenses. New products in pipeline - Developing a range of narcotic & dermatology products. Range of oral solid products under-development to increase market share in generic and OTC markets.

US Markets: 50+ products in various therapy area segments. Add 4-5 new products to its portfolio during the year under review.

Expansion strategy - 23 ANDAs filed till date. Increase in ANDA fillings for soft gel dosage. New products in pipeline - 25 products identified with a focus on soft gels and OTC products. 15 products in R&D.

Expecting few approvals in FY21.

Australia’s pharmaceutical market is set to rise from $30.5 billion in 2018 to US$ 40.1 billion by 2024 registering a CAGR of 5.1%. Marksans carries out business operations in Australia and New Zealand through its subsidiary Nova Pharmaceuticals. Nova is one of the leading generics and private label suppliers in Australia. Tie-ups with topmost retailers & pharmacies in Australia, like Woolworths Ltd., Coles Mayer Ltd., Aldis, Metcash and Fauldings

RoW Markets - Targeting four major clusters such as South East Asia, Russia & CIS, Middle East and Africa. In these countries, specific countries like Kenya, Ukraine, Sri Lanka, Cambodia and Myanmar are targeted. In the process of launching new products and obtaining product registration for ~175 developed products in emerging markets.

Spent 15.7 crores on R&D activities which is 1.5% of revenues(9M FY21)

Plans to enhance portfolio with addition of 12-13 products every year

The company has a robust forward integrated business model and plans to backward integrate into API manufacturing (for captive consumption thereby having presence in the entire value chain)

Ongoing investments in the frontend gives confidence of maintaining the momentum.

Achieve 2000 crores of topline in next few years

FCF - 91.3 crore

Improvement in EBITDA margins due to Operational efficiency and better product mix

Integration of acquired companies added to better value addition over the years. COVID situation also added to better price realizations. Saw price correction in raw materials(RM of Ibuprofen).

US Markets: Entered the markets in 2010-11, filed ANDA in 2012. The business model was supplying bulk drugs. Late 2015, acquired Timecap labs and pursued front end sales. Started creating their own labels and moved to retail markets. Current US Orderbook status - $100 million. Future plan: increase wallet share from existing cx, add new cx, market penetration

UK Markets: Active in the market, revolved from CRAMS to vertically integrated company.

Plan to invest in R&D, capex(infra and expansion of capacity). Capex mapped for backward integration of key molecules. Capex of 200 crores for next 2-3 years. Allocated 50 crores for backward integration, will invest more in later stages.

WC cycle of 120 days, this is the best optimal no. Need to maintain higher level of inventory(frontend).

-> US will be the main growth driver going ahead. Expect to clock 80 MUSD revenue soon,have very strong visibility and can take this to 100 MUSD given the orders.WC cycle of 120 days on overall basis.

-> Margin improvement mainly led by US operations maturing. Fixed costs are very high and thus it takes time. Company entered US markets in 2010-11 as a contract manufacturer but has now evolved into a company with own front-end post Time Caps acquisition.

-> Plan to undertake backward integration for few molecules.Envisaging a capex of 200cr. over next 3 years.Majority of this will be towards capacity enhancement.Current utilisation is around 70-75%(I might be wrong on this)

-> Q3 margins may not sustain since company had some element of better realisations coming from few products.However,operating leverage on account of higher volumes in US market might mitigate this.

-> Company has only “scratched the surface” in US market,has a very long way to go.The profitability though is dependent on market dynamics and company has little control over this aspect.

A lot of questions were around buybacks and higher dividends.One participant seemed extremely exasperated with the stock price movement and Mr. Mark had to ask him to make way for others Overall,company seems very confident of growing sales and volumes in the US market.All things remaining equal,this should lead to better profitability.They also seemed to have taken on-board some suggestions on raising promoter stake or buybacks/dividends.

Overall,company seems very confident of growing sales and volumes in the US market.All things remaining equal,this should lead to better profitability.They also seemed to have taken on-board some suggestions on raising promoter stake or buybacks/dividends.

Overall,company seems very confident of growing sales and volumes in the US market.All things remaining equal,this should lead to better profitability.They also seemed to have taken on-board some suggestions on raising promoter stake or buybacks/dividends.