Hello, I have put together below portfolio over past 3 yrs with my limited knowledge of businesses. Suggestions from knowledgeable boarders would be highly appreciated to further improve it.

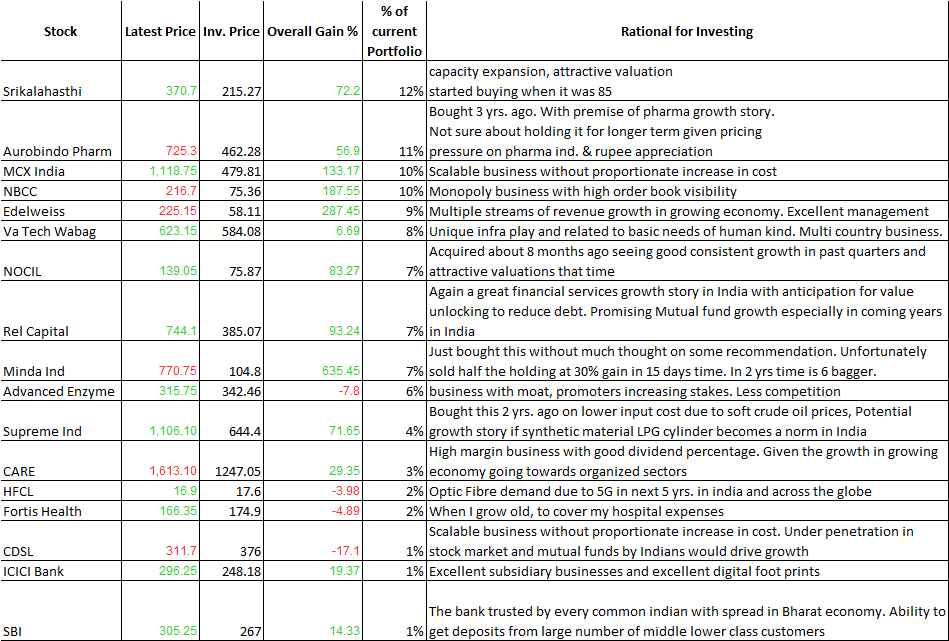

Stock Latest Price Inv. Price Overall Gain % % of current Portfolio Rational for Investing

Srikalahasthi 370.7 215.27 72.2 12% “capacity expansion, attractive valuation

started buying when it was 85”

Aurobindo Pharm 725.3 462.28 56.9 11% “Bought 3 yrs. ago. With premise of pharma growth story.

Not sure about holding it for longer term given pricing

pressure on pharma ind. & rupee appreciation”

MCX India 1,118.75 479.81 133.17 10% Scalable business without proportionate increase in cost

NBCC 216.7 75.36 187.55 10% Monopoly business with high order book visibility

Edelweiss 225.15 58.11 287.45 9% Multiple streams of revenue growth in growing economy. Excellent management

Va Tech Wabag 623.15 584.08 6.69 8% Unique infra play and related to basic needs of human kind. Multi country business.

NOCIL 139.05 75.87 83.27 7% “Acquired about 8 months ago seeing good consistent growth in past quarters and

attractive valuations that time”

Rel Capital 744.1 385.07 93.24 7% Again a great financial services growth story in India with anticipation for value unlocking to reduce debt. Promising Mutual fund growth especially in coming years in India

Minda Ind 770.75 104.8 635.45 7% Just bought this without much thought on some recommendation. Unfortunately sold half the holding at 30% gain in 15 days time. In 2 yrs time is 6 bagger.

Advanced Enzyme 315.75 342.46 -7.8 6% business with moat, promoters increasing stakes. Less competition

Supreme Ind 1,106.10 644.4 71.65 4% “Bought this 2 yrs. ago on lower input cost due to soft crude oil prices, Potential

growth story if synthetic material LPG cylinder becomes a norm in India”

CARE 1,613.10 1247.05 29.35 3% High margin business with good dividend percentage. Given the growth in growing economy going towards organized sectors

HFCL 16.9 17.6 -3.98 2% Optic Fibre demand due to 5G in next 5 yrs. in india and across the globe

Fortis Health 166.35 174.9 -4.89 2% When I grow old, to cover my hospital expenses

CDSL 311.7 376 -17.1 1% “Scalable business without proportionate increase in cost. Under penetration in

stock market and mutual funds by Indians would drive growth”

ICICI Bank 296.25 248.18 19.37 1% Excellent subsidiary businesses and excellent digital foot prints

SBI 305.25 267 14.33 1% “The bank trusted by every common indian with spread in Bharat economy. Ability to

get deposits from large number of middle lower class customers”

In most bull markets it tends to go up pretty late in the party for one reason or the other.

In most bull markets it tends to go up pretty late in the party for one reason or the other.