Found an article in the web about the distillation process. Please find it attached.

Summarizing the inputs, catalysts and outputs:

Inputs: Alpha-pinene, Beta-pinene

Main catalysts: Titanium Dioxide (TiO2), Sulphuric Acid (H2SO4), Sodium Hydroxide (NaOH)…

Output: Camphor Ponomarev.pdf (218.1 KB)

Throwing some questions for people to ponder about:

Where do we source those pinenes from? Are those imported? Do we have enough pine trees in India? Who cuts those trees and sells the pinenes to us? What is our bargaining power with them?

We didn’t really research much about our interaction with the customers yet. Looking up SCL’s website (India’s largest camphor player as claimed by them). It is indeed some pharmaceutical and beauty product companies. What is our bargaining power with these guys? Given camphor is a commoditized product, I believe there is very less scope for value-addition, but I’m not sure.

I believe the catalysts mentioned are cheaply available as they are widely used chemicals. Any comments?

This video suggests that 67% of alpha-pinene is produced in China and the total alpha-pinene market is less than $200 million world-wide.

We may be importing them from China.

Having said that, I find that lots of companies which produce camphor (and related derivatives) also sell alpha-pinene (Checkout Himalaya Terpenes for example). So it is possible that alpha-pinenes are an “intermediate-input” to Mangalam and the raw pine trees are the “actual-inputs” to the company.

@phreakv6@NamantS

Price of terpene derivatives like camphor, menthol are rising because of supply constraint, not because demand has increased. Infact we should see the demand falling in response. Why is this good for mangalam organics? Infact, how does mangalam organics benefits from supply constraint?

Yes you are correct there is supply constraint but we are trying to find out if this supply constraint is cause of a structural reason or just short term.

According to @phreak theory the supply constraint is due to a structural change which makes us believe that these high prices are sustainable.

Why should the demand fall in response? Do the pharmaceutical, beauty and tyres have alternative inputs other than camphor (and its derivatives) to replace?

Let’s take tyre. The Tyre manufacturers will increase price to find the optimum profit point. They will in process sacrifice part of the demand, and will in turn consume less of camphor. Though if camphor costs a fraction of value of product (say tyre), then we can treat demand as inelastic.

Let me rephrase. Mangalam is doing crude gum distillation to produce both gum rosin and gum turpentine oil. However, demand for gum rosin is declining because of crude oil based alternatives. This means, Mangalam will see reduced profitability from gum rosin derived products, and to offset that, they are charging higher for gum turpentine derived products like camphor, just to make the same level of profit as before. That will not explain their increased profit margin.

Am I missing something?

I don’t think they have charged higher so easily. Camphor is a fairly commoditized market, with less scope for firm specific value addition (at B2B level), so Mangalam wouldn’t have such higher pricing power. From what I understand, the supply of camphor based products has come down as adhesive makers have moved to crude based manufacturing instead of the distillation process. This brought up the prices in favour of Mangalam.

Regarding the increase in margin, I think it is due to the introduction of B2C value-added products like CamPure, Cam+… I can’t attribute it to this point confidently unless I get a breakup on the revenues.

Perfect! Your theory was on point. So now we have established that this supply constraint and price increase is structural change and is here to stay for atleast next 1-2years if not more. The current PE for the whole year would come to be around 7-8 which seems pretty attractive for company that is now in growth orbit . Will post my chart analysis on this stock soon on this thread.

I dont think they make anything from Gum Rosin as of now. 80% of realisation is from Camphor. I think rest of the terpene chemicals will contribute another 10% and Gum Rosin might be less than 10% which I think is why they are trying the tie-up with DRT to export terpene phenolic resin which is a value-added derivative of Gum Rosin.

Is the break of the revenue given anywhere?

Also how is it that other companies that were producing Gum rosin and as a byproduct were producing terpene oils are not able to take advantage of this price increase in camphor? Cause if managalam uses the same process then what is the advantage?

Is it that managalam does not need to go through the whole distillation process to extract the terpene oils as a byproduct and therefore has a cost benefit? Something is missing

Please read the annual report that points to 80% revenue being from Camphor. This was for FY18. Now the proportion should be higher.

All Camphor players are having a good run at varying degrees. Check Kanchi Karpooram and Oriental Aromatics.

I am done with researching this. Let’s wait for Q3 and see how things go. Messages are not adding to the discussion as I sense a lot of repetition happening.

There is good support around 440. Will watch this level closely,if 440 is broken the next support would be around the 400zone. Best accumulation zone would be between 440-400 in my opinion.Also if you observe the volumes on this downfall has been very low so that is a good sign that the downfall may be shortlived.

Disclosure: Not holding any shares.

My messages may have been repetitive so sorry for that.

Sirs I have a small info regarding this. I attended AGM of KANCHI KARPOORAM and found out a few things

Camphor is the main product of distillation of alpha pinene which u have discussed clearly.

China is still producing camphor but imports to India stopped 2 yrs for now.

I requested for quote from a major Chinese player who says a kilogram of camphor is 16 dollars per kg. While in India it is only 11 dollars per kg or 750 RS per kg.

The RM for Kanchi is not sourced from China but from Indonesia ,Brazil mainly.

Hence we are not able to match our domestic consumption at all. But i do have a concern coz mangalam I have confirmed from the management is doubling their capacity and Kanchi is tripling their capacity. Will the supply exceed demand if that happens.

The reason given to me for stoppage of Chinese imports is because Chinese are getting better margins from exports to Europe( by Kanchi mgmt.)

We should know what is the domestic requirements and whas it production capacity.

The companies produce dipentene which is also sold. ( It also needs a little research also)

Gum rosin is not of much interest for the companies since whenever crude based derivative is available cheap they don’t get good prices

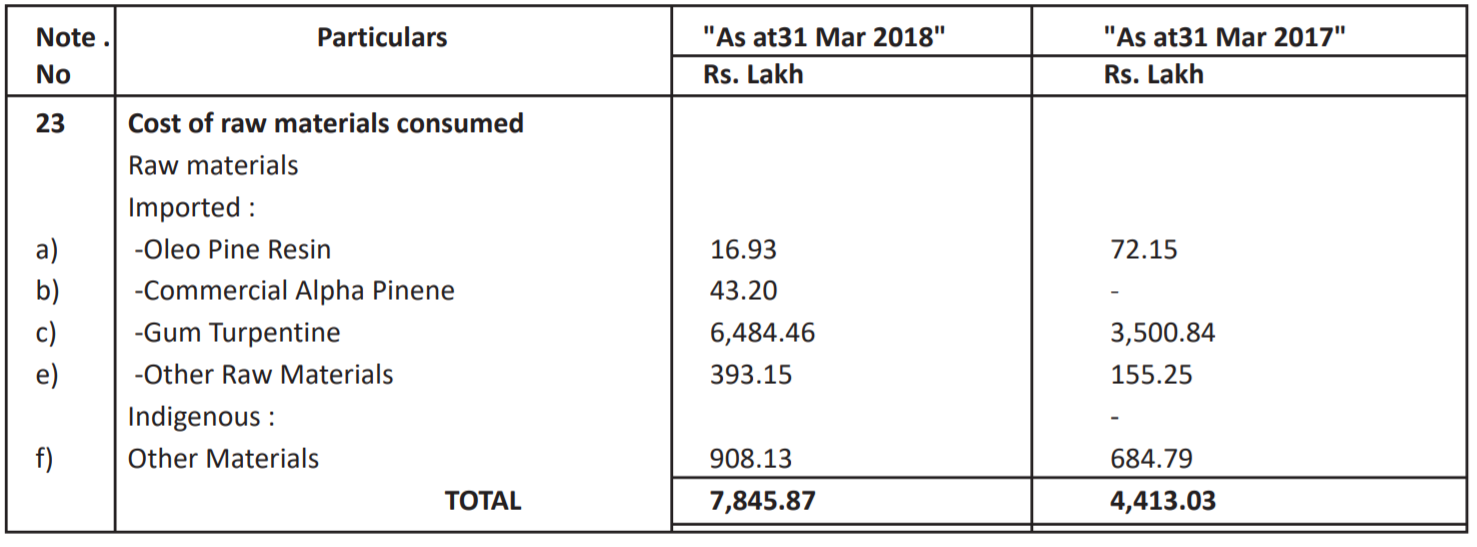

@phreakv6 Going through Kanchi Karpooram’s AR, they say they import Gum terpentine and that foreign currency fluctuations can have a significant impact on their profits.

And if Mangalam is producing on their own, they need to have better margins in comparison to Kanchi, which is not the case. Can you please explain if I’m missing anything here?

@gurramlokesh - I noticed this too in Kanchi’s AR although I couldn’t find anything concrete from Mangalam. I don’t think its a bad idea to assume both are doing the same business and there is a possibility that Mangalam is also importing Gum Turpentine like Kanchi Karpooram. If this were true, the only way to explain the numbers these players are having is via pricing power. (It can’t be inventory gains, going by the RM inventory in the BS as of Mar ’18. Also going by their WC cycle, they must have gone through multiple cycles of inventories during this period.)

Can a commodity business pass on price hikes of over 2-3x that easily? I think this is where the uniqueness of Camphor comes into the picture. Unlike most other commodities which are consumed by businesses to make other commodities or products backed by brands, camphor here is almost completely consumed by retail households as is. Maybe this is why it was easy to pass on the price hikes?

I did a small calculation to see how this will work. RM looks to be 65% of sales so when it doubles, to maintain the same EBITDA, the topline has to go up by 65% and when RM triples, the topline has to go up by 130% to maintain same EBITDA, roughly. But if they are able to increase topline by 70% in the first case, the extra 5% flows directly to the bottomline. If they are in fact able to maintain gross margins at 65% even with RM price doubling or tripling, they will be able to double or triple their EBIDTA which is what appears to be happening (most of the retail consumption is in 100-250gm packs, so not very difficult to raise prices?) so this could be another alternative explanation - just good old pricing power. How long it can last is anyone’s guess.