Is mangalam organics expanding their capacity. I thought that their capacity is 6000 mtpa and I read in dialweath that they are expanding to 12000 mtpa

Sir is mangalam expanding its capacity X2. I read in dialweath that they are expanding to 12000 mtpa in 6 months but couldn’t find anything about capacity expansion or debottlenecking in AR or in AGM notes.

@Prasadkumaresan The Crisil report attached earlier on this thread on October 30th mentions the installed capacity at 16,000 tonne per annum, so personally I’ll go by that. I understand that there is still some spare capacity & any meaningful capex is probably still 12 to 15 months away. In the interim, the Co. could always go in for debottlenecking if required. With the current performance / cash flows being what they are, funding any future expansion should not be an issue when ever that is to happen,

1 Like

Sir are you also tracking kanchi KARPOORAM as well?.. I attended their AGM and from their inputs with the capacity expansion happening around in 6 months don’t u feel Kanchi is still undervalued?. I am invested in both. My views may be little biased too.mangalam s results were very much in line with expectations while Kanchi s results when compared qoq looks bad but they had a distinct advantage in q1 ( so the NPM was higher)coz of THE RM sourced at low cost which they actually divulged in the AGM and is clearly seen in their AR too. BUT topline looked very much in line to the demand and now the NPM at 15 looks reasonable and sustainable. Now with camphor prices settling around 820 RS per kg at factory level do u see both of the companies will be benefited?. And with the additional capacities happening may be around 2 yrs in our players do u see any change in demand supply mismatch happening with increased supply available which may be bring down margins drastically?. And as far as I researched on camphor Chinese smaller companies have closed but FUJI GREEN their largest player has stopped exporting to india. But with increase in prices here can we see the risk of Chinese starting exports to India as we are the major consumers in the world.

1 Like

I think I may have cracked the Camphor puzzle. ![]() I think the key is Menthol which is also a Terpene derivative, just like Camphor. Menthol prices have shot up due to pharma sector procurements. Both share similar intermediates, as well as raw materials. (For example, α-pinene, which is readily obtainable from natural sources, is converted to citronellal and camphor. Citronellal is also converted to rose oxide and menthol.)

I think the key is Menthol which is also a Terpene derivative, just like Camphor. Menthol prices have shot up due to pharma sector procurements. Both share similar intermediates, as well as raw materials. (For example, α-pinene, which is readily obtainable from natural sources, is converted to citronellal and camphor. Citronellal is also converted to rose oxide and menthol.)

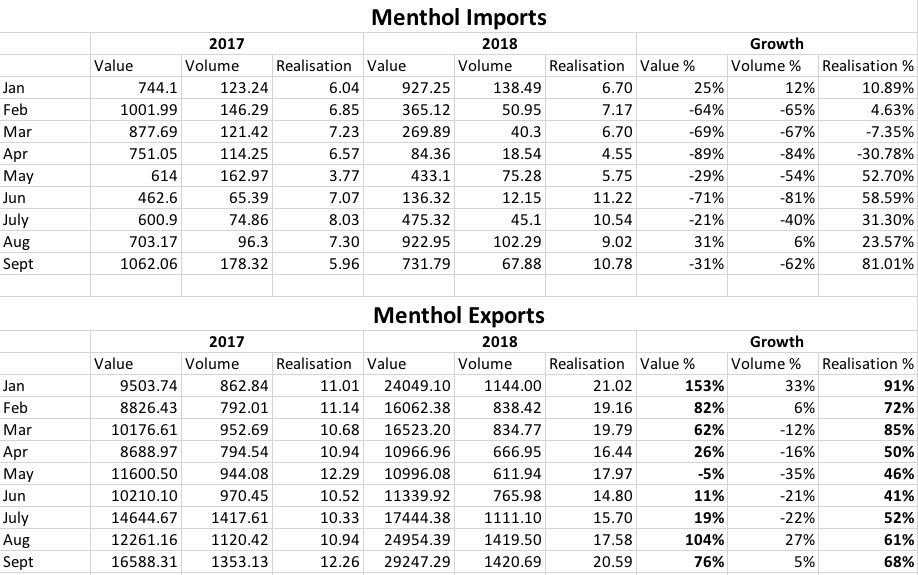

Here is some data I gathered for Menthol.

Menthol imports to India have come down by value and volume presumably due to shortages abroad, most probably China. This wouldn’t have directly affected Camphor industry in any way unless we were filling that gap by exporting Menthol. This is exactly what has happened. The reduction in imports also would have been compensated by domestic Menthol production, all of which would have stressed Terpene based products. Camphor is the predominant Terpene derivative in use in India. I suspect the increase could have also taken out the unorganised market which would have found procurements at higher prices difficult. If the situation continues, as it seems to be doing, going by last two months increase in realisations in Menthol prices, Camphor players will continue to have a good run. Tracking Menthol data might act as a proxy to play this theme.

36 Likes

Good analysis.

I have two questions -

1)Methanol can be a derivative of Terpene but i dont think that is the only way to produce it.

" Methanol is produced from synthesis gas (carbon monoxide and hydrogen), itself derived from oil,coal or, increasingly, biomass."

^First thing that comes up on google.

So that means demand for methanol does not necessarily have to create a huge shortage for Terpene. Do we have any breakup of as to how much of total methanol production is done from Terpene ?

2)Why did exports volume decrease from march to july 2018? Even though prices were up from 2017 the volumes decreased. What could be the possible explanation for this?

-

Menthol, not Methanol.

-

Probably high domestic demand

2 Likes

Oops.

No wonder I couldn’t find anything online connecting methanol to terpene.

Actually yes domestic demand not being fulfilled due to lower imports is fulfilled from domestic production which leads to lower exports.

Great work! But do you think without DRT deal they will be able to maintain think kind of volume growth for the next 2-3quarters?

Continuing my research on this sector and getting a bit deeper into the chemistry and underlying fundamental shifts.

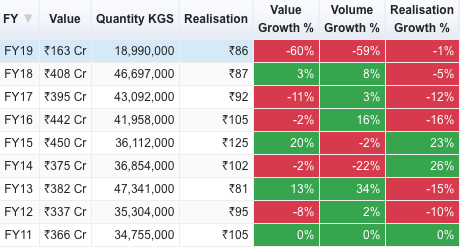

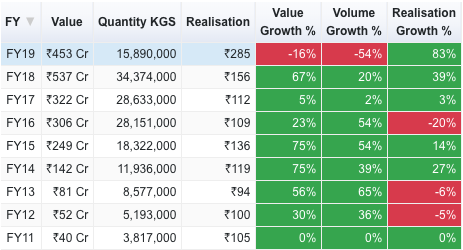

Check out the import data for Gum Rosin and Gum Terpentine for India.

This is Gum Rosin

This is Gum Terpentine Oil

The numbers I want you to look at is the realisation delta between the two.

FY11 - Both are same

FY12 - 5% higher

FY13 - 16% higher

FY14 - 17% higher

FY15 - 11% higher

FY16 - 4% higher

FY17 - 22% higher

FY18 - 80% higher

FY19 (so far) - 231% higher

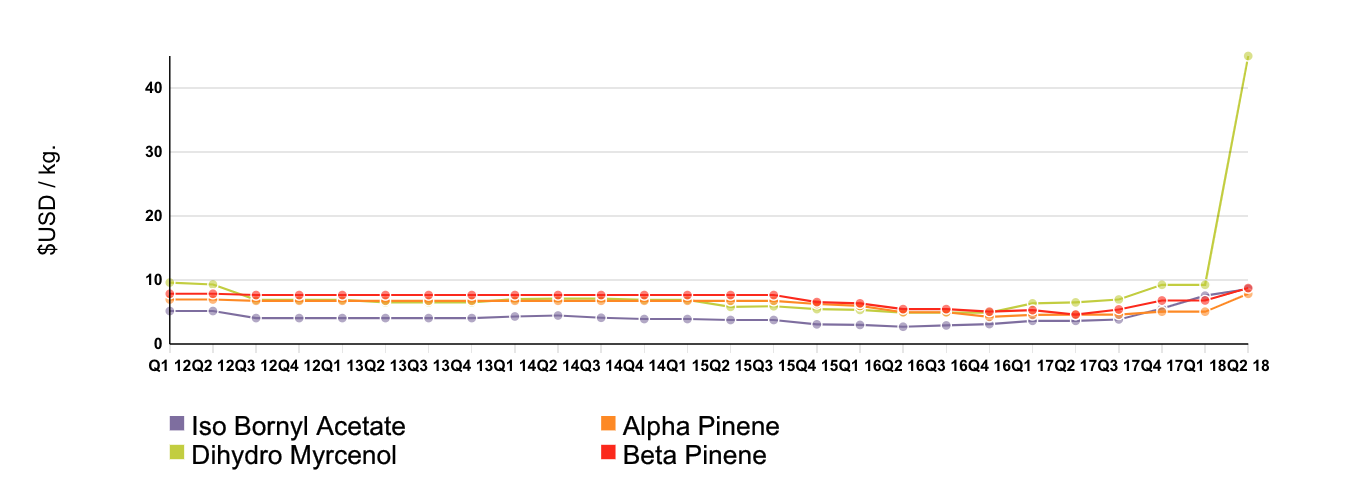

Why is this data significant? Let’s look at the relationship between Gum Rosin and Gum Terpentine Oil. Both are products of the distillation of crude gum. The terpenes are extracted from distillation and are composed of alpha and beta pinenes which are used to make the terpene chemicals like Camphor, Menthol, Tepineol, Terpinyl Acetate, Iso Bornyl Acetate etc. The Gum Rosin is the leftover resin post distillation and has several applications where its primary function is to increase friction and also as waxes, varnishes and adhesives.

It looks like users of resin have shifted to crude-based products.

Source: https://berjeinc.com/category/SYNTHETICS/

So the Gum Rosin/Gum Terpentine Oil manufacturers have cut down on production because Gum Rosin demand has gone down due to synthetic resins being cheaper (Look at the timeline, its in sync (with a lag when the market disruption took place) with the period when Crude cooled off) and that is adversely affecting Gum Terpentine Oil prices and consequently, all Terpene derivatives (I stumbled onto Menthol and that’s what set me off on this wild goose chase). So what was essentially moving together is now moving inversely.

For Gum Rosin/Gum Terpentine Oil manufacturers to continue production, the price of Gum Terpentine Oil must include the realisation they derived from Gum Rosin for it to be remunerative. In addition to all this, China seems to have peeved its farmers by importing cheaper crude gum which has lead to lesser availability of RM.

This was as of July. The Gum Terpentine Oil import prices in August and September show the consequence of this as prices have firmed up lot more since.

This is the latest update, from October

Source: https://berjeinc.com/2018/09/01/turpentine-derivatives-33/

This whole situation would reverse itself if crude went back above $100 because the low crude is what has caused this fundamental shift in FY17 and early half of FY18. Now that crude is cooling back down again, it doesn’t look like Terpentine Oil prices will come down and this might be the new reality where Gum Terpentine Oil price includes the previous realisation from Gum Rosin for it to be competitive for the distiller. If some productive use were found for the resin, the players who find that productive use could have double the benefit.

33 Likes

Great fact findings … Unfortunately there is no concall transcript available in BSE, it would be helpful to get more clarity…If any boarders have the transcript please share…

Some more updates from Berjé for November and December.

This was the Gum Turpentine price trend as of September.

If December prices are over $5/kg, then it should be somewhere in the vicinity of Rs.365. If the correlation between Gum Turpentine Oil and Camphor I presumed is real, good times should continue for domestic Camphor makers.

15 Likes

Great work @phreakv6. Was away for 2weeks as i was busy with an exam.

I have read your post twice to try understand the relations between all the variables.

This is what i have understood please correct me if i am wrong.

There are two ways to make adhesives -

- Resin From Trees & Plants

- Petroleum based products

From the 1st method i.e Trees & plants

Gum Rosin which is used to make adhesives is produced from distillation of Resin. The leftover resin post distillation is Gum Rosin. As a part of the distillation process terpenes are also extracted which is used to make terpene chemicals like camphor. So before when adhesives were being produced Resin,producers would have realizations from two products the primary one being Gum Rosin(Adhesive) and the secondary one would be Gum terpenes.

Now because crude is falling adhesives are being made from crude based products.This is leading to lower production of terpenes from natural resins because they find it cheaper to produce ashesives from crude rather than Gum Rosin. Supply of these terpenes is falling due to this which is leading to increase in prices of them i.e leading to increase in prices for camphor and other terpense based derivatives.So basically till crude based production is cheaper the prices of terpene based derivatives will be high.

14 Likes

Interesting analysis phreakv6! Thumbs up on the Menthol post.

A few points from my side.

If cheap crude oil => higher terpene based derivatives price, then we should have seen the price of camphor and menthol to be even more high in 2015-2016 years (crude touched $30 a barrel then). But that was not the case. Though your analysis makes sense, I think the “impact” of lower crude oil price is very low.

I think the stronger impact / influence was due to shortages in China. And this is due to closure of several facilities in China on account of pollution norms (source: SCL latest credit report). This looks in line with management’s guidance as pointed out by the blog post attached by Rajeev.

Also, the latest credit report suggests that the raw materials - alpha pine and gum turpentine, are very volatile. These are mainly imported from China and Indonesia. How easy is it pass on the raw materials prices to consumers? Tried some googling but unable to find any revealing trends / insights. If someone can point out good direction for this, it will be really appreciated.

Also I have some industry related questions like

- What is the size of the camphor industry?

- What is its CAGR over the past few years and its forecast for the upcoming years?

- What is its size in China? This would help us understand / quantify the under-penetration in the Indian “hygienic” market alone.

Disclosure: Not invested yet but I find the story interesting.

4 Likes

https://www.credenceresearch.com/report/camphor-tablets-market

This article suggests it was $93.9 million in 2016 and expects a CAGR of 7.6% to rise to $145.6 million in 2022. Not sure how relevant these numbers are now, given such a dynamic shift in the price.

I believe these sort of long-term shifts/substitutions take time due to various reasons. For eg. we were serious about blending ethanol in petrol only in 2017 when crude prices were above $110 years back. Oil fell big in FY16 and it looks like it was in FY17/FY18 that resin/adhesive manufacturers have substituted Gum Rosin with synthetic resins. I find this theory plausible.

I don’t think the company imports Gum Turpentine Oil from China because that would mean that the company is importing a crucial intermediate post distillation and there is no scope for significant value addition. The fact that the company also produces resin I think implies that the company does the distillation itself. The fact that Gum Turpentine Oil import prices have gone up when the company’s OPM has expanded also signifies that the company is not importing this as a raw material but is in fact producing this in house. The imports of Gum Turpentine Oil as well is quite small compared to the local Camphor industry size. We don’t seem to be importing any Camphor from anywhere as well, so competing with Chinese imports makes no sense (saw this line of reasoning in Crisil report).

I request you to go through the Berjé site I had posted above. They have covered the sector well and have pointed to what’s happening in China. Plant closures are not due to pollution issues but mainly because of the resin substitution affecting realisations. The Crisil report in this thread spells alpha pinene as alpha pine and says this is the raw material. I think the raw material for this company should be crude gum and not these intermediates. These reports were too confusing and made no sense which was why I decided to research these by myself. I have spun a story based on the numbers that made sense to me. I might be wrong.

UPDATE: Found this where products of Mangalam Organics are listed and it shows Gum Turpentine Oil as a product Mangalam Organics supplies which again substantiates that this is not a RM that the company imports.

12 Likes

So you’re saying Managalam would also be producing Gum Resin due the distillation process used to extract t oils?

Can you please elaborate on the process. Does distillation lead to Gum Resin and are the turpentine oils just a by product of this process?

@phreakv6 Your dogged determination to get to the bottom of the camphor puzzle is commendable & I for one am wiser for it. This is meaningful research & very beneficial. Thanks a ton & please keep the good work going.

8 Likes

The management had clearly said the prices are sustainable which shows that there must be a structural shift that is taking place rather than short a short term production mismatch.

I think till now @phreak theory is the best explanation for whatever is happening.

Has anyone got reply from the company for the questions asked?

Thanks for the explanation phreakv6. Fits very well into the data / records.

Credit rating reports indeed don’t seem fully credible.