I was trying to get answers for a few important questions

- How sustainable are the current camphor prices?

- What happened to the DRT deal?

- How exactly is Mangalam Organics different from Kanchi Karpooram

- Will the management share the money with us?

This is what I found.

1. How sustainable are the current camphor prices?

Came across this very interesting piece of research by a GM in the Chinese pine chemical industry.

This is from 2017 but I think it is a precursor for what has happened since.

Crux of it is that Chinese rosin production has been on a slow decline since 2006 and so has the exports.

China has historically distilled crude gum mainly for the gum rosin and it is from gum rosin that the distillers derived almost 70% of their revenue. Gum Turpentine Oil was more of a side-product. From 2012 onward China has started importing Gum Rosin because it was producing less and less of it and also because imports were cheaper from Indonesia and Brazil.

So what has caused this reduction in production in China?

- Plantations preferring Eucalyptus to Pine because of the paper industry

- Increase in labour costs in China which made people stop taking up menial jobs like tapping pine

- Substitutions of Gum Rosin with crude based C5 and C9 hydrocarbon resin which are lower priced and perform similar functions

- To a very small extent, pollution control in China. This however is not the main driver.

So the storm which was brewing for awhile looks to have tipped the boat over in Q4 FY18 when resin substitution went up full swing making it almost unviable for China to be distilling gum. This is not a one year thing but something structural which has been going on for over a decade, reaching its inflection point last year. Feb '18 saw zero imports of Camphor into our country. That’s when MO management must have smacked their lips and gone for the buyback. As insiders, they knew of this dynamic in the industry.

Coming to Camphor, 99% of the capacities in the world are in India and China. India has a large captive market for its Camphor while China was using it for pharma products and exporting some to India, Singapore, Thailand etc. Reduction in Gum Rosin has affected Gum Turpentine oil available for making terpene derivatives which meant that China had to stop production of Camphor and even had to import it because of unviable costs in RM and unavailability of Gum Turpentine oil.

While this does make it sound very sustainable, there is also the risk of China procuring gum turpentine oil to make camphor to dump into India or even a country like Indonesia which has a large captive production of gum turpentine oil can produce camphor and dump into India. This is a risk but will someone there setup capacities for a product which doesn’t have a captive market? Considering the market size isn’t very big, there are chances that the production might remain in the niche market of India.

Odds of Gum Turpentine oil prices reducing are slim and even if it drops, the camphor players have probably experienced the magic of “pricing power” for the first time where they could bump prices up 2.5x with no one kicking a fuss (Not many commodities can pull this off. In fact I can’t think of even one other. Imagine doing it with Milk for eg.). Will they give this up that easily? Remember that a large bulk of production lies with just 4 major players in India making it almost a oligopoly. Am not alluding to price-fixing, but it’s a distinct possibility. Now what if Gum turpentine oil prices rise even further? Can these players continue to pass it on, on top of the 2.5x they have done in the last one year? At some point the devout camphor burning devotee is bound to notice, even if he only buys 50gm packs? The last thing one would want is a govt. regulation of prices here. The pharma applications should be able to absorb the costs though considering camphor is a very, very small ingredient in topical and inhaling meds.

So it does look like prices are sustainable at this point with some mild risks which have to be kept in mind.

2. What happened to the DRT deal?

There are a lot of sources on the net reporting this deal here, here and here, among several others.

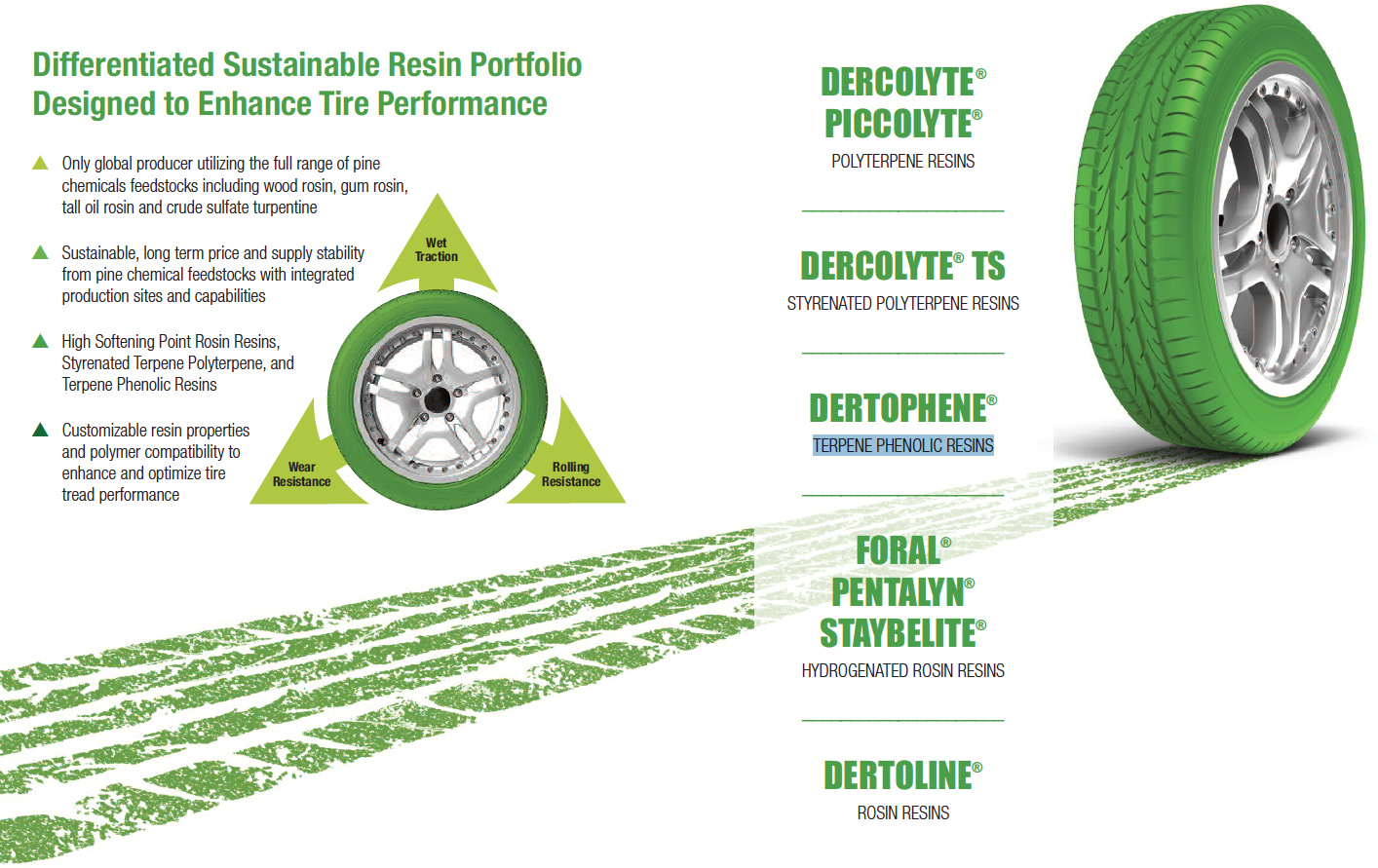

This is how Terpene Phenolic Resin is currently used in tyres.

DRT has a product called DERTOPHENE which is used in tyres. It doesn’t look like they expect this product to be exported to start with, going by the articles above. DRT has a sales office in Mumbai and perhaps DERTOPHENE is sold within the country at present using Mangalam’s terpene phenolic resin customised for DRT. I see weekly imports of Dertophene from imports data here lending credence to this theory.

MO has also increased TPR capacity to 50 MT/mo recently so it does look like this deal might be contributing to topline already.

3. How exactly is Mangalam Organics different from Kanchi Karpooram

I have speculated few times here - before Q2 results and before Q3 results that the margins MO was reporting was showing better signs and have speculated reasons from retail foray, backward integration and probably better processes. Here is some substantiation towards that.

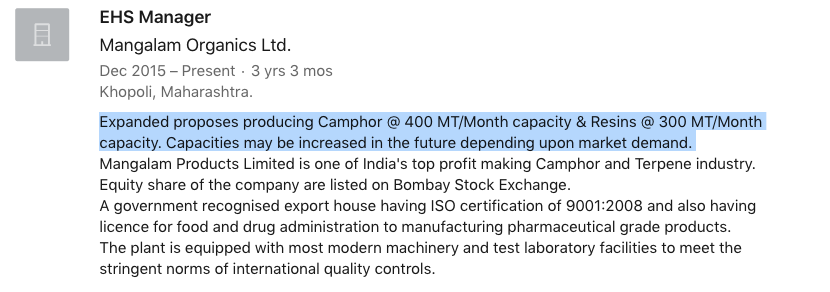

This is something i picked from linkedin from the profile of the [EHS Manager at MO] ((https://www.linkedin.com/in/shankar-parekar-68a17594/) (This fellow has worked at Sun Pharma/Guj Fluoro in the past).

It looks like it is easy to increase/decrease production without incurring large fixed operating costs. So part of the margin expansion is due to operating leverage.

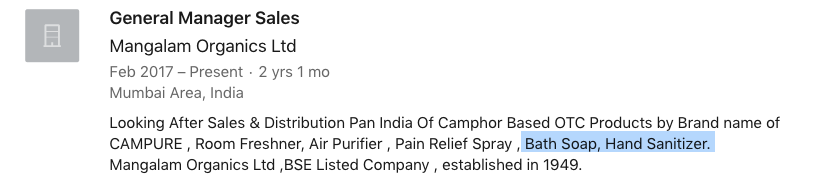

For the FMCG foray with Mangalam/Campure/Cam+ branded products, they seem to have hired a FMCG manager with past experience in Bambino/ITC/Parle/Wagh Bakri. This must be the guy behind the distribution reach they seem to have got pretty quickly in the last two years. Interesting thing is the mention of Bath Soap and Hand Sanitizer here because these products are not launched yet. Maybe they are coming soon.

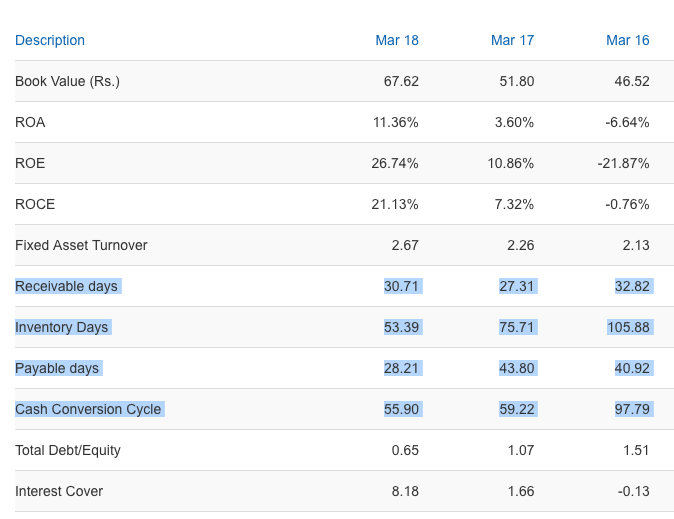

Retail foray is not an easy game and can lead to death by working capital. ![]() This is how MO’s working capital has moved.

This is how MO’s working capital has moved.

They are improving in every WC metric in the last 3 years, so its not time to panic (yet) from this retail foray.

Their operations head looks to have experience in Hikal/UPL/Bayer/GulfOil in the past and appears to be the one behind the process optimisation and cost reduction.

All these hires are in the last 3 years, so there appears to be good things happening here. Contrast that with Kanchi Karpooram’s people. There is really nothing to write home about. Its possible that they aren’t on linkedin but odds of that are slim. It does look like these two companies are different night and day based on these data points.

Update: For Kanchi vs Mangalam, I forgot the add that KK’s FCF since 2010 is not even positive (-4.94 Cr) while for the same period Mangalam’s FCF is positive at 24.68 Cr. For last 3 years, the difference is even more stark where KK’s FCF is -4.99 Cr and Mangalam’s is 45.60 Cr.

4. Will the management share the money with us?

The management has spent 15 Cr last year - 14 Cr in buybacks and 1 Cr in dividends. The yield would be 5% if it was all dividends based on current prices. Last year’s PAT was 14 Cr so they gave out 100% but I don’t think we can extrapolate based on this. The management has taken hefty salary increases - Almost 3 Cr + 3 Cr + 2.4 Cr for themselves this year. You can argue that they deserve because they are delivering but it is something to be kept in mind as a risk. Besides 14 Cr PAT is very different from a 75-100 Cr PAT possible this year. I cannot read what will happen based on these two data points because they are contrasting. However, going by the buyback price of Rs.230, the management I feel did what’s best for “them” which just happened to be good for the shareholders as well (reduction in equity base). At this point I am ready to let this pass but it will be a very important param for me later this year. Too many small companies have short-changed shareholders when large money was involved.

Disc: I am enjoying deep research and concentrated positions. This is not a buy/sell reco and I may buy or sell anytime if thesis changes.