So Rs 300 per Kg turpentine is converted into Rs 1000 per Kg Camphor. Mangalam is probably getting higher margins to its FMCG products and value-added products which they supply to DRT.

@Prasadwakchaure - MOL sells Gum Turpentine Oil too. Here is the link: http://www.indiachemicalexporters.com/mangalam-organics-limited/gum-turpentine-oil-pr1602972-sCATALOG-swf.html

In my opinion, MOL is a big black box right now. Need to get out a lot of information from next AGM meet since management doesn’t share much.

Need to understand their position in entire value chain. Not sure of their backward integration capability. Need to know if they buy Rosin (Crude Gum) as their raw material and then distill it themselves with Gum Rosin and Gum Turpentine Oil as the distillation output. Or they buy Turpentine Oil as raw material (then why trade when you can make value added products?). Looking at the difference in gross margins between Kanchi and MOL - I won’t be surprised if MOL has backward integration capability and does it’s own distillation. But higher gross margins can also be because of domestic value added Cam Pure and Cam+ products. That is why I said - MOL is a big black box, at least for me.

I was trying to get answers for a few important questions

- How sustainable are the current camphor prices?

- What happened to the DRT deal?

- How exactly is Mangalam Organics different from Kanchi Karpooram

- Will the management share the money with us?

This is what I found.

1. How sustainable are the current camphor prices?

Came across this very interesting piece of research by a GM in the Chinese pine chemical industry.

This is from 2017 but I think it is a precursor for what has happened since.

Crux of it is that Chinese rosin production has been on a slow decline since 2006 and so has the exports.

China has historically distilled crude gum mainly for the gum rosin and it is from gum rosin that the distillers derived almost 70% of their revenue. Gum Turpentine Oil was more of a side-product. From 2012 onward China has started importing Gum Rosin because it was producing less and less of it and also because imports were cheaper from Indonesia and Brazil.

So what has caused this reduction in production in China?

- Plantations preferring Eucalyptus to Pine because of the paper industry

- Increase in labour costs in China which made people stop taking up menial jobs like tapping pine

- Substitutions of Gum Rosin with crude based C5 and C9 hydrocarbon resin which are lower priced and perform similar functions

- To a very small extent, pollution control in China. This however is not the main driver.

So the storm which was brewing for awhile looks to have tipped the boat over in Q4 FY18 when resin substitution went up full swing making it almost unviable for China to be distilling gum. This is not a one year thing but something structural which has been going on for over a decade, reaching its inflection point last year. Feb '18 saw zero imports of Camphor into our country. That’s when MO management must have smacked their lips and gone for the buyback. As insiders, they knew of this dynamic in the industry.

Coming to Camphor, 99% of the capacities in the world are in India and China. India has a large captive market for its Camphor while China was using it for pharma products and exporting some to India, Singapore, Thailand etc. Reduction in Gum Rosin has affected Gum Turpentine oil available for making terpene derivatives which meant that China had to stop production of Camphor and even had to import it because of unviable costs in RM and unavailability of Gum Turpentine oil.

While this does make it sound very sustainable, there is also the risk of China procuring gum turpentine oil to make camphor to dump into India or even a country like Indonesia which has a large captive production of gum turpentine oil can produce camphor and dump into India. This is a risk but will someone there setup capacities for a product which doesn’t have a captive market? Considering the market size isn’t very big, there are chances that the production might remain in the niche market of India.

Odds of Gum Turpentine oil prices reducing are slim and even if it drops, the camphor players have probably experienced the magic of “pricing power” for the first time where they could bump prices up 2.5x with no one kicking a fuss (Not many commodities can pull this off. In fact I can’t think of even one other. Imagine doing it with Milk for eg.). Will they give this up that easily? Remember that a large bulk of production lies with just 4 major players in India making it almost a oligopoly. Am not alluding to price-fixing, but it’s a distinct possibility. Now what if Gum turpentine oil prices rise even further? Can these players continue to pass it on, on top of the 2.5x they have done in the last one year? At some point the devout camphor burning devotee is bound to notice, even if he only buys 50gm packs? The last thing one would want is a govt. regulation of prices here. The pharma applications should be able to absorb the costs though considering camphor is a very, very small ingredient in topical and inhaling meds.

So it does look like prices are sustainable at this point with some mild risks which have to be kept in mind.

2. What happened to the DRT deal?

There are a lot of sources on the net reporting this deal here, here and here, among several others.

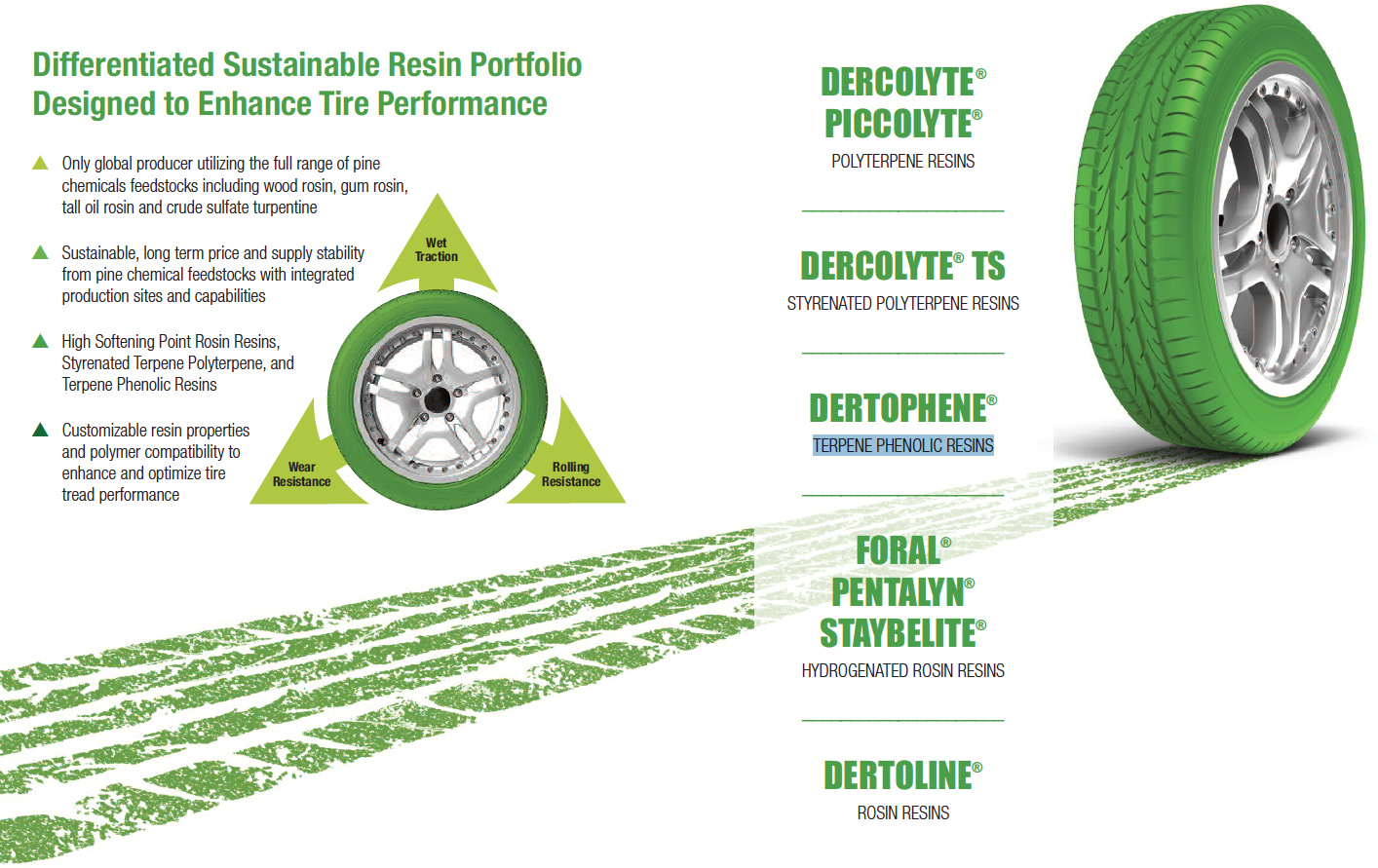

This is how Terpene Phenolic Resin is currently used in tyres.

DRT has a product called DERTOPHENE which is used in tyres. It doesn’t look like they expect this product to be exported to start with, going by the articles above. DRT has a sales office in Mumbai and perhaps DERTOPHENE is sold within the country at present using Mangalam’s terpene phenolic resin customised for DRT. I see weekly imports of Dertophene from imports data here lending credence to this theory.

MO has also increased TPR capacity to 50 MT/mo recently so it does look like this deal might be contributing to topline already.

3. How exactly is Mangalam Organics different from Kanchi Karpooram

I have speculated few times here - before Q2 results and before Q3 results that the margins MO was reporting was showing better signs and have speculated reasons from retail foray, backward integration and probably better processes. Here is some substantiation towards that.

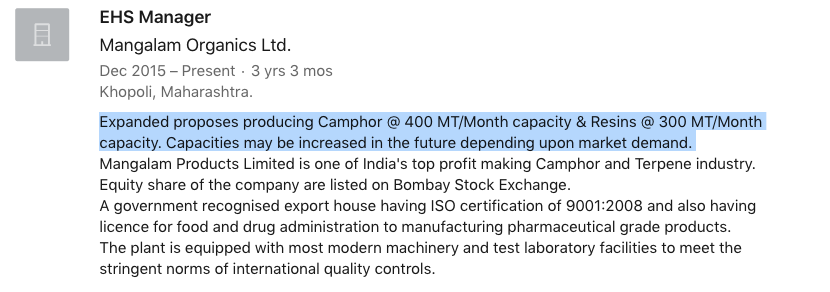

This is something i picked from linkedin from the profile of the [EHS Manager at MO] ((https://www.linkedin.com/in/shankar-parekar-68a17594/) (This fellow has worked at Sun Pharma/Guj Fluoro in the past).

It looks like it is easy to increase/decrease production without incurring large fixed operating costs. So part of the margin expansion is due to operating leverage.

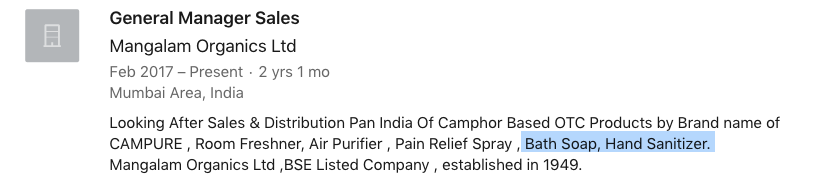

For the FMCG foray with Mangalam/Campure/Cam+ branded products, they seem to have hired a FMCG manager with past experience in Bambino/ITC/Parle/Wagh Bakri. This must be the guy behind the distribution reach they seem to have got pretty quickly in the last two years. Interesting thing is the mention of Bath Soap and Hand Sanitizer here because these products are not launched yet. Maybe they are coming soon.

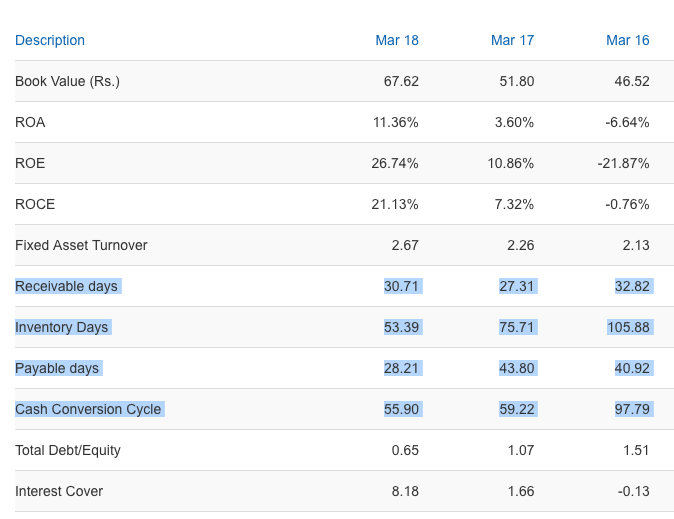

Retail foray is not an easy game and can lead to death by working capital. ![]() This is how MO’s working capital has moved.

This is how MO’s working capital has moved.

They are improving in every WC metric in the last 3 years, so its not time to panic (yet) from this retail foray.

Their operations head looks to have experience in Hikal/UPL/Bayer/GulfOil in the past and appears to be the one behind the process optimisation and cost reduction.

All these hires are in the last 3 years, so there appears to be good things happening here. Contrast that with Kanchi Karpooram’s people. There is really nothing to write home about. Its possible that they aren’t on linkedin but odds of that are slim. It does look like these two companies are different night and day based on these data points.

Update: For Kanchi vs Mangalam, I forgot the add that KK’s FCF since 2010 is not even positive (-4.94 Cr) while for the same period Mangalam’s FCF is positive at 24.68 Cr. For last 3 years, the difference is even more stark where KK’s FCF is -4.99 Cr and Mangalam’s is 45.60 Cr.

4. Will the management share the money with us?

The management has spent 15 Cr last year - 14 Cr in buybacks and 1 Cr in dividends. The yield would be 5% if it was all dividends based on current prices. Last year’s PAT was 14 Cr so they gave out 100% but I don’t think we can extrapolate based on this. The management has taken hefty salary increases - Almost 3 Cr + 3 Cr + 2.4 Cr for themselves this year. You can argue that they deserve because they are delivering but it is something to be kept in mind as a risk. Besides 14 Cr PAT is very different from a 75-100 Cr PAT possible this year. I cannot read what will happen based on these two data points because they are contrasting. However, going by the buyback price of Rs.230, the management I feel did what’s best for “them” which just happened to be good for the shareholders as well (reduction in equity base). At this point I am ready to let this pass but it will be a very important param for me later this year. Too many small companies have short-changed shareholders when large money was involved.

Disc: I am enjoying deep research and concentrated positions. This is not a buy/sell reco and I may buy or sell anytime if thesis changes.

46 Likes

Update by Berje for month of March 2019 confirms that Gum Turpentine prices continue with their upward climb and now are back to Dec '18 levels and suggest price will continue to go higher.

https://www.berjeinc.com/2019/03/01/turpentine-derivatives-38/

3 Likes

Appreciate the detailed evaluation on Mangalam Organics, but isn’t the comparison with Kanchi a bit weak? There is no evaluation basis the effective future capacity of both the companies product wise. With new infusion at Kanchi, it would be important to see that. Since the thread initiation is for Mangalam and there has been point wise elaborate discussion on it, is it a case of inadvertent bias?

1 Like

What is the new infusion at Kanchi ?

I meant the previous equity infusion

Capacity post expansion s.t. regulatory:-

Mangalam Organics-

-

Enhancement of production quantity of Camphor (350 MT/M to 550 MT/M), Sodium Acetate (275 MT/M to 500 MT/M) & Alkyl Phenol Formaldehyde Resin (28 MT/M to 50 MT/M),

-

Reduction of Carene, Lg, DP, Pine Tar, IBA, Camphene, Terpene Chemicals from 465 MT/M to 300 MT/M & Phenolic Resin (166.66 MT/M to 150 MT/M) and

-

Removal of Alkyd Resin, Furan Resin, Polyster Resin, Polyamide Resin, Ketonic Resin, Paper Sizing Chemicals

-

Overall total production quantity shall be 1559.66 MT/M. (Source link and details from this thread)

Kanchi-

2 Likes

3 Likes

Some more substantiation from a different source

argus-c-5-and-hydrocarbon-resins.pdf (3.3 MB)

There is a definite bias towards Mangalam. The problem was that the market was pricing both these companies similarly when the post was written. IMHO, these two seem to be different companies in terms of growth, product mix, capacity, ambition, financials and governance. The post should be seen in the context of peer comparison and nothing more.

6 Likes

“This is with reference to the above captioned subject line and in compliance of Listing Regulations, we wish to inform BSE that Mr. Ankur Gala, has tendered his resignation from the post of Company Secretary and Compliance Officer of the Company with effect from closing business hours of March 6, 2019.”

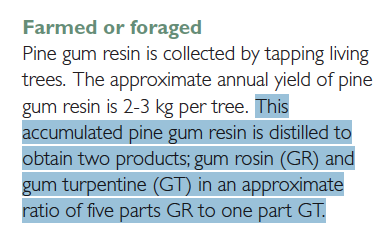

Trying to figure out how much higher can Gum Turpentine prices go. It looks like GR:GT is something like 5:1 in the distillation process.

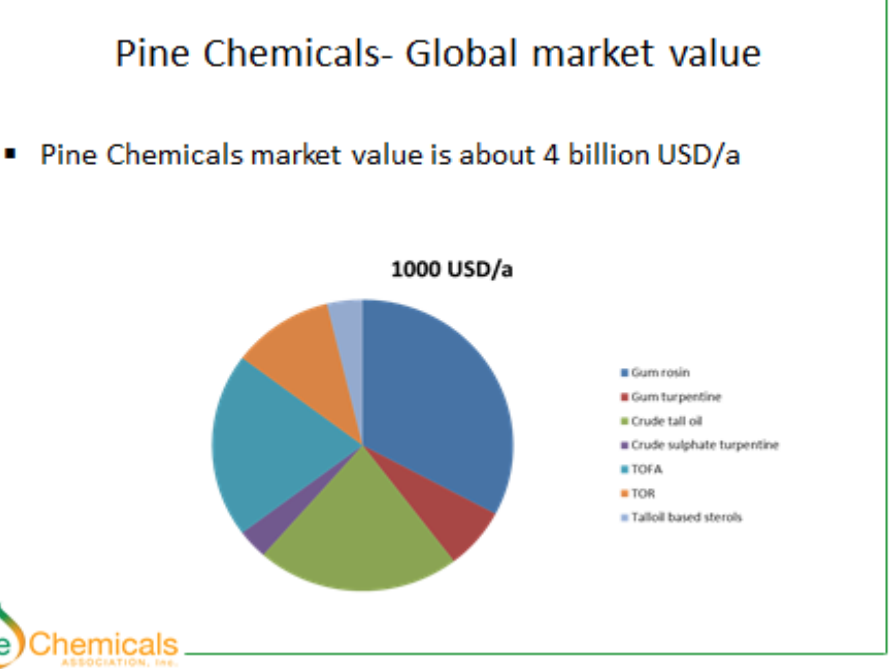

This is how the pine chemicals market looked in 2015. Something like 1/3rd of the market is GT/GR. Notice how small GT is in the whole mix. Gum Rosin used to be the bigger market - almost $1 billion by itself and it has suddenly gone out of favour due to substitutes.

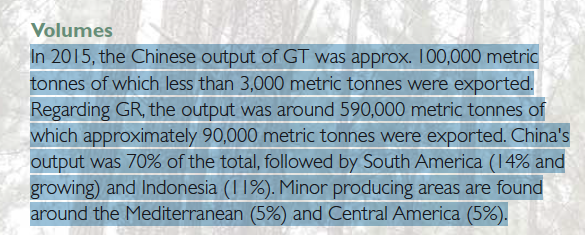

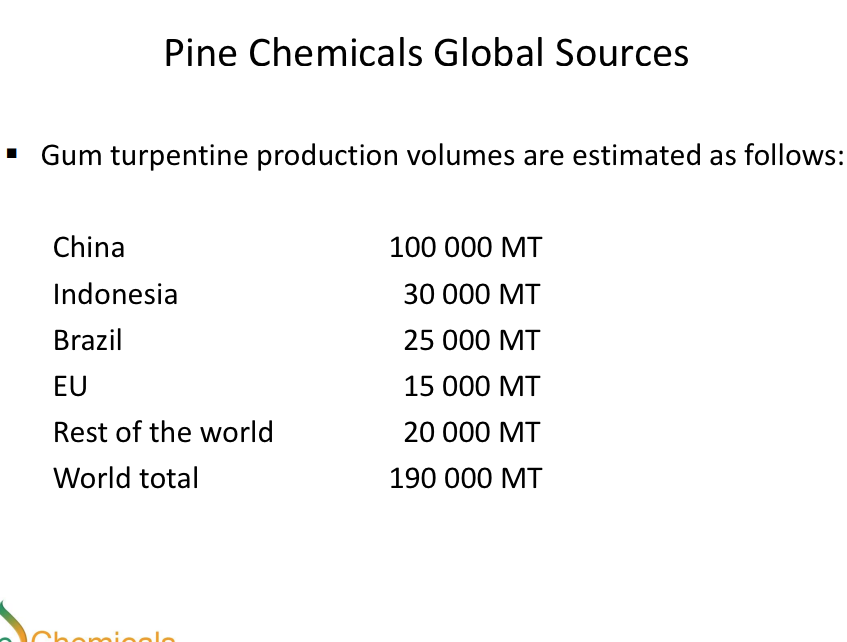

It looks like China used to make 100,000 MT of GT, of which 3000 MT was exported. This was back in 2015 and this number must have fallen drastically since.

Where does this 100,000 MT stand in terms of total production?

So China used to be almost 50% of world production and has taken a serious structural hit based on the sources shared previously.

GR:GT used to be 1:1 in terms of price earlier. This means that 5:1 is the value extracted via distillation in the past. This explains why Gum Rosin demand falling is such a big deal. GT can theoretically rise almost 5x from old prices (right now at 3x) for it to be remunerative. If it does rise 5x, it will be interesting times as the demand is fairly inelastic, both in terms of Camphor or other flavours and fragrance RMs/intermediates, considering they form a small part of the cost of end-products. I am not very sure though if Camphor prices can move up higher to 1500/kg levels (wholesale) from the current 1000/kg. If that can’t be done, margins will shrink for pure Camphor players while companies that are backward integrated will expand margins greatly.

A company like SH Kelkar for eg., has been facing the brunt of it, with their margins shrinking to multi-year lows

Sources attached

10-Socio-Economic-Report-TURPENTINE-Report.pdf (603.8 KB)

Monday_Speaker_2-_Keijo_Ukko.pdf (739.2 KB)

12 Likes

Great findings @phreakv6 . Thank you for sharing!

If GT’s price rises 5x from older prices, why wouldn’t locals tapping pine gum resin (PGR) ask for more money? In other words - I mean the owners of pine trees asking for more money for their PGR. Ultimately, its them who have to be remunerated properly in the supply chain to provide main raw material (PGR).

If PGR’s price rises, and camphor prices remain unchanged, margins will suffer for everyone regardless of backward integration or not. Would you agree? Thoughts?

1 Like

It doesn’t look like the problem is because of supply constraints in PGR. The problem is because of drop in demand for GR. So the pine-tappers who were already ill-paid now have a double-whammy - in fact there is something to this effect on Berje from last year where China is even importing PGR because its cheaper from outside. Given this, PGR prices will remain suppressed.

Now coming to some math, PGR looks to be around Rs.80 ($1.1 or so/kg) and has been so for a long time without much changes. GR and GT both were around Rs.100/kg.

Assuming 6 kgs of PGR is distilled, it should give 5 kgs of Gum Rosin and 1 kg of Gum Turpentine.

So for a distiller,

RM cost = 80x6 = 480

and what they can make out of it is,

GT = 100

GR = 5x100 = 500

Gross Margin = (600-480)/(500+100) = 20%

Now assume GR prices drop to Rs.75 from Rs.100 (a reality at present) and GT prices rise to Rs.300 (again, this hss happened already)

GT = 300

GR = 75

Gross Margin = (675-480)/(375+300) = 29%

This is assuming all the Gum Rosin is sold. If say, demand has slumped and only 60% can be sold

Gross Margin = (525-480)/(225+300) = 9%.

Now to compensate and get the GM back up, GT prices rise to 400

Gross Margin = (625-480)/(225+400) = 23%.

So as long as Gum Rosin has at least some usage, GT price may not rise more than 400, which is about 30% more than current prices around 300.

But this simple math shows why GR will be replaced by GT as the prime contributor, as long as resin substitution continue, with crude remaining low.

As for backward integration for terpene derivatives, if a business is already at present backward integrated and is unable to raise derivative prices, increase in GT price will not increase their margins. At best, they will remain what they are. If however, they can sell some of the intermediate GT, their margins could increase. This is of course assuming they make more GT than they require for their derivatives, which may not be true in reality. Privi Organics (Fairchem) is the only player I could see in the listed space that is backward integrated. It shows in their Q3 margins as well.

When it comes to Camphor, I think it’s possible for prices to rise further till about 1200-1300 wholesale when GT prices move up to Rs.400, if at all. This would mean that retail Camphor will go up to about Rs.2000/kg which I consider a hard-top - because then 50 gm packs will get into 3 digits above this level. I already see d-mart selling 20 gm packs alongside the 50 gm packs. So reduction in pack size could again be a permanent thing.

We must also consider the low barrier of entry here, being a commodity chemical. Capitalism will work its magic if this goes on for long and competition will drive prices down. It could be some time away but it’s an eventuality that will make the market not give a higher multiple here, even if the prices are going to be sustainable.

15 Likes

Mangalam will be out of ASM from Monday 8th March.

Looks like the soap thing (found in the linkedin profile above) is indeed true. Not sure how any of these will move the needle on the numbers though, due to base effect. If they are going to hold inventory for all these SKUs in an unproven brand, working capital could suffer badly, although it hasn’t done yet. They don’t seem to be aggressive pushing all products equally though at this point and I presume manufacturing is outsourced. This one looks like it may have to compete with Dettol. Tall ask? Let’s see if their BTL advertising strategy works here, as it looks to have done in Campure Cone/Stick/Camphor products.

8 Likes

Your passion for mangalam is beyond compare. Hope it proves its worth.

1 Like

Mangalam’s valuation are very low as the markets are not certain about the sustainability of December qtr margins. It is perhaps also being seen as a commodity player largely in the B to B category. This could change going forward.

If it is established that even when Mangalam is branding for other players like D’mart etc, it is doing so in small retail quantities, as opposed to supplying in tonnes, it could well bring about a perception change. Besides, it is reasonable to assume that its own branded sales must be growing rapidly.

The expanding range of Cam + products is significant in that it tells you that the mgt. could well be using the current boom to build an FMCG brand. Its products have already been tried by most of us so product quality is not an issue here. The soap market is huge as we all know. If any one of its products catches the fancy of the consumer, it could potentially create enormous value for its share holders, given that we are in an era of on-line marketing and scaling up does not require the same kind of marketing effort as before.

14 Likes

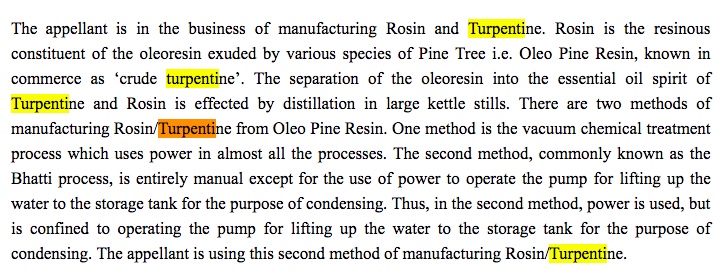

A court case document - it mentions that Mangalam is a producer of Turpentine and Rosin.

This verifies for me the increase in gross margins for the company over the past 8 quarters. Unlike Kanchi Karpooram, which imports crude turpentine.

8 Likes

Thank you for sharing @akshat96jain! Can you please share the document? I’m interested to know more about this case.