Why the promoter is keeping changing the growth rate and why it is necessary for him to appear in front of the media every month?

April:

May:

August:

And what others shared is for September.

Why the promoter is keeping changing the growth rate and why it is necessary for him to appear in front of the media every month?

April:

May:

August:

And what others shared is for September.

When are they raising capital?

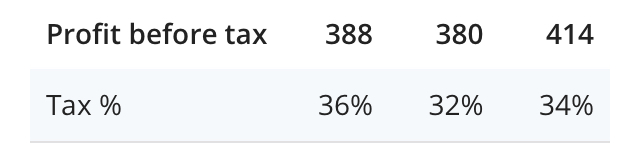

Today corporate tax rate was cut to 25%

It is the biggest gift for all companies especially those who pay higher taxes

In India NBFC s pays highest tax rate of 35%

Manappuram also used to pay 35% tax

Now it has to pay 25%

It will increase the profit by 15-20% immediately

Now sept quarter profit before tax was 414 Crore

35% tax

So profit after tax was 272 Crore

Now with 25% tax profit will be 310 Crore given no growth (1240 annual profit )

At current price of 134 with zero growth

Price to earning comes 9.1 in 12 months

With 20% profit growth as expected by management PE comes 7.6 In next 12 months

As per Nirmal bang report

Jim Rickards : If you take 33,000t and divide it by US$9.6 trillion, which is how much you have to back, the gold price comes to about US$10,000/oz.”

It is very possible that gold could touch 10000 dollars (6x from current levels if for some reason USD crashes )

We are living in a very uncertain world.

China and Russia can come up with crazy idea to introduce gold backed bitcoin like currency

Gold is like hedging in your portfolio

After reading this article It looks like physical gold is a very important asset

Paper gold is also risky

Thanks for detailed writeup. Manappuram mgmt quality is impeccable with good execution track record. Views invited on it from VPers

https://www.freepressjournal.in/interviews/mannapuram-home-finance-could-be-a-financial-gladiator

is the mgmt overoptimistic in above interview ?

Error: At what rate is your gold loan be increasing?

We have targeted gold loan growth by 50%. We are meeting that.

Just an error here - he would have said 15% gold loan growth - Communication error. Can refer to previous interviews.

Aggregate growth of 20% with higher growth coming from non gold business.

ROEs of both gold loan financiers have increased recently(22% last year) and should move higher with corporate tax rate cuts.

Fund Raising update:

I feel rationale presented here looks quite simplistic. Don’t think it works like that in reality.

I think the rise in gold prices not gonna help gold financing companies as they don’t often sell gold and recover the loan amount.

Manapuram yield on gold loan is 24%(as per their latest quarterly presentation). Isn’t this too high for secured loan? If personal loan is available at 11 to 14% then who is taking gold loan at 20+ interest rate? Is this yield and NIM sustainable??

Please help me to understand

Not anyone can get personal loan. There is lot of documentation, credit history, required. For gold loan you almost don’t need anything and best suited for immediate needs

Ok understood but is such high yield sustainable?

In India gold finance is dominated by unorganised sector and they charge 1.5 times the organised companies like Manappuram and muthoot

Gold loan is taken mainly for short duration eg for one month interest will be 1-2% for a month .In such cases people don’t care about interest rate ,they just need fast money .

As Sunil said, personal loan is available only for the salaried. Farmers, Kirana guys are entirely dependent on gold and unorganized lending. So we can’t compare gold with personal loan.

Higher prices will help Manappuram to distribute more money to borrowers. So there should be 1 to 3% boost to the existing distributions.

You have a point there. I just took a gold loan (actually Sovereign Gold Bonds, but they are classified as gold loan by the bank) from HDFC Bank. Interest 10.5%; processing fee waived off; no annual fee or any other fee; HDFC Bank has become very aggressive on these kind of products

Buying Sovereign Gold Bonds and mortgaging it requires some level of financial knowledge/awareness. Generally those segment wouldn’t go for gold loan unless they have any other option.

From what I have seen, gold loan customers generally repeat their mortgage. Every year they would put their jewel on loan for some x months and recover it. Purpose of load would be agri fertilizer purchase, medical need, short term obligation like relative’s marriage expense etc. They don’t save money so they take jewel loan, and pay it back in 2 to 3 months. And this continues often as some expense would pop up every year. I would say most use it as a short term credit facility as they don’t have credit card.

Jewel loan is non-salaried’s credit card so it carries higher interest rate

Many banks have tried gold loan in the past without much success.

I have visited many towns in India and when I speak with farmers ,many say that they are unaware of Manappuram and muthoot branch in their own village.They just visit the local gold finance guy who gives loan at higher interest and no cap at LTV(loan to value )

So the order will always be like this ,due to lack of knowledge and urgency :

First unorganised sector

Second Manappuram/muthoot etc

Third small banks

Fourt large private banks

Last psu banks

Most of the customers just know unorganised local guy who gives gold loan at very high interest rate

This order will change to organised sector in future but I guess it will happen very very slowly

Hence today there is huge untapped market

Manappuram is growing at 20% and still getting PE of 10 due to many such reasons .Management is aware of risks due to monoline business hence since couple of years there are moving towards diversified nbfc with diversified borrowing /funding

Its price usually fluctuates between 10-15 pE

Market has still not factored the recurring 15% annual profit growth just due to tax cut

We may see the rerating soon

I think Mr. Market will rerate this stock only when the management shows clear signs of good capital allocation and ability to handle diverse biz lines. Their diversification as a strategy is good but the execution has been patchy so far. Both housing and vehicle segment have not stabilised the asset quality even after so many quarters. Making money from gold loan is good but it is not a high growth market so market wants to be sure they are not blowing capital in other businesses.

Management said 20%

CAGR

And 20% Consolidated growth looks very possible

20% growth plus 10% tax cut if both comes together then rerating is definitely on board

Even if no PE rerating ,it looks like 20-30% compounder for couple of years till gold loan is more than 50% of total book

Hopefully NPA remains under control and no surprise regulatory /geopolitical shocks

The foremost factor expected to propel gold’s price upward is the deepening economic slowdown, not just in India but globally. The second factor is trade war.

“A rate-cut cycle in the US, which is unlikely to reverse anytime soon, has the potential to spark off a secular bull run in gold

Gold has done well for one year after remaining stagnant for five years prior to that. The upward leg in gold’s cycle tends to last for at least three-four years,