- I dont think the gold loan business is lagging, on the contrary it seems to have performed better. revenue up by 22% and PAT 27%

- consolidated definitely better with 25% up on rev and 35% up on PAT.

- as per the company , they expect “substantial” pick up of gold loans during Q2

- Gross NPA of Ashirvad is really low. (0.68%)

- rate of borrowing same as last quarter at 9.3%.

4 Likes

The gold loan growth comparison is a little bit orange to apples. the loan duration for Manappuram is shorter than Muthoot and other firms. The impact is that the run down in the book is faster and growth is volatile as 1-2 quarters of low growth can impact growth much more. On the other hand, lower duration means that the NPA can be kept lower (muthoot is 3.2%+ GNPA i think) and funding can be done via short term instruments.

Playing devil’s advocate to your devil’s advocate  …would have management pushing growth in financial services or being conservative ?

…would have management pushing growth in financial services or being conservative ?

On vehicle loan and Home loan, you are right. their NPA are still higher than average

9 Likes

I thought they are apples only and no tangy orange yet as far as gold loan segment is concerned. Let’s take few factors here.

NPA - Well, these are no real NPAs which result in losses but accounting NPA due to late payment or default cases that need to recovered through auctions. In short, Manappuram is able to attract disciplined customers in theory. Manappuram scores here but this is not a fundamental differentiating factor for a LT investor. If I have to choose between high NPA of Muthoot’s gold biz vs. high NPA of Manappuram’s other biz, I would opt for higher NPA In gold loan any given day.

From borrowers’ perspective Muthoot provides more flexible payment options but Manappuram insists on hard deadline of MTM settlement every 3 months. Let’s face it, a typical borrower in the gold loan segment has either bad credit history or fallen into the difficult times. Muthoot is a better lender for this segment in either case. Manappuram is trying to enforce discipline on those who were not so in the past. Additionally, in a rising gold prices scenario risks are less and lenders could become aggressive without affecting quality which Muthoot is well poised for.

Value Leakage - I heard this term recently. When you are paying DDT in an industry which requires capital perpetually, dividend distribution is value leakage. Listing of Ashirwad will invite holding discount as well and another way of leaking value.

There can’t be a better biz environment for gold lenders than we are in currently. Galloping gold prices, NBFC liquidity squeeze etc but they can’t grow gold AUM more than 10% yoy. There is something in the market that I have not understood fully.

Disc: I have no strong view on Muthoot but can consider Manappuram @1.7-1.8 P/B again.

6 Likes

https://finance.yahoo.com/news/edited-transcript-manappuram-nse-earnings-235325165.html

there have been extensive flooding but our portfolio exposure, AUM exposure in this areas may not exceed 2, 3 percentage.

We target a consolidated AUM growth of around 20%, which we hope we’ll be able to achieve. And ROE of around 20%,

We expect growth in gold loans to pick up substantially in Q2, driven largely by growth in tonnage

4 Likes

Rising gold prices is a great environment for gold loan companies and it shows in the results of Muthoot, but not Manappuram.

Muthoot has grown their gold loan AUM by 15% yoy in Q1. And the growth would have been more if not moderated voluntarily by them due to rising gold prices. Muthoot decreased LTV from 75% to 70%. To further moderate the growth they stopped fresh disbursement for 3 days. https://www.bseindia.com/xml-data/corpfiling/AttachHis/f80525d6-fac9-44c8-b216-26822424203a.pdf

Manappurams growth (gold loan AUM), in comparison was only 6%, which is a concern.

Even a layman on the street know that to play the GOLD AUM the best choice is Muthoot … Nether the management nor any indicators demonstrated that Manappuram would be SECTOR LEADER in GOLD LOAN… Even now they guide for 10-12% gold aum growth.

Having said that … All that matters in a well diversified financial organization like Manappuram is

Good ALM , Stable Asset Quality , Good return Ratios and on top high class earning growth in tough environment and that’s been successfully demonstrated by the company.

This is the performance snapshot so far and every stakeholders of the company must feel good about it …

What next??? Thats projection and forecast and anybody’s guess …

1 Like

Hi Tauqeer,

One question I asked myself while buying this kind of business is

Is growth first or Safety first…? in this example considering the NPA’s which Muthoot is holding… it should be safety first… the street/customer might think Muthoot because they give loans at a cheaper rate of interest and it is almost 8 months or so for Muthoot to bring the loan to NPA for Manappuram it is 3 months. even LTV is higher for Muthoot compared to Manappuram.

All of the above means customers who are desperate for money will not approach Manappuram which is really good, because my(Manappuram) customers really have the ability to pay their money back. Particularly in turbulent times when there is a liquidity crunch this should be of utmost importance.

I felt it is safer buying Manappuram as long as they are growing their gold business (atleast for the time being).

Considering their NPA profile, any business would only want to lend Manappuram compared to Muthoot and this is proven as well if you read for investments in Manappuram’s Corporate Announcements. Their competitors downside is temporarily subsided because of the increase in gold prices, however think of a situation when gold prices are not increasing. If i were a bank/MF i will lend my money to Manappuram than Muthoot.

This is my 2 cents.

Disc: Holding Manappuram

10 Likes

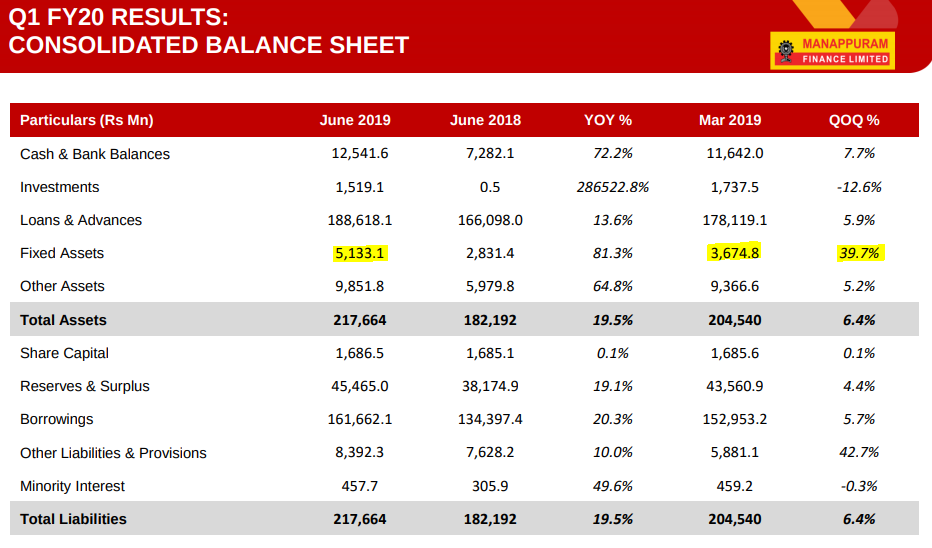

Did you notice the sudden spike in fixed assets? The result presentation for the quarter shows an investment of nearly 150 Crore into fixed assets during the current quarter - was this question raised by anyone during the concall?

Increase of 81% YoY and 40% during the quarter looks abnormal for a gold loan company.

Disclosure: Invested

AJ

3 Likes

Is it possible that these are the new Godrej Vaults that the management was talking about? Which will help them reduce security expenses?

Manappuram as a company for Investment is far better than Muthoot Finance. The difference between both the groups is that Muthoot has kept the Gold Loan company separate and the Vehicle finance company is Muthoot Capital Services. I am a huge fan of Muthoot Capital Services (They are into 2W financing and 2nd hand car financing) and I believe at the current price it has certainly got multibagger potential. However, I am not very enthused about Muthoot Finance due to the lack of growth. Quarter after Quarter they have shown inability to grow beyond 10 percent on Topline and Bottomline. Manappuram on the other hand has kept all the verticals in the same company. I admire both the groups though. Both have robust business models, have stood the test of time and will continue to do very well over the next 5-10 years.

As far as Manappuram is concerned, Show me a single comparable NBFI with the following characteristics:

Growth : It has been consistently growing its topline at 15-20% and bottomline at 35-40% over the last 4 quarters. It has been a steady growth pattern over the past 4-6 quarters. From all the evidences, it seems the growth trajectory is expected to continue over the next 2 years at least

Well diversified business: Well, some critics may say that if they want to play a pure gold loan company, they would much rather buy Muthoot Finance. Well, I respect their views but I look at at overall business model and the valuation of the NBFI. There is no point in buying a gold loan focused NBFI like Muthoot Finance which is growing at just 10% odd. In Indian markets growth is given disproportionate weightage in terms of valuations.

Asset Quality: We are operating in an environment of decades high gold prices. Imagine what is going to happen if gold prices crash from here. Muthoot Finance, which already has very high NPA as compared to Manappuram, is going to see very high NPAs because of their high tenures. Muthoot collection policy is very lax which is giving them the advantage in terms of AUM Growth. The promoter has himself said in a concall that they do not put pressure on customers for collection and are not really concerned about inflated ’ Technical NPAs’. Well, these so called technical NPA’s can swell from 4-5% to 9-10% very easily if there is a crash in gold prices. The risk management and credit systems are much better for Manappuram and that reflects better in their Gross and Net NPA vis-a-vis Muthoot. As an investor, I would prefer my company to sacrifice some part of growth to ensure high class asset quality. Also, the so called prudence of Muthoot Finance is not even helping them in growth. The topline and bottomline growth continues to be dissapointing every quarter.

Borrowing Profile: The borrowing profile is well spread out and there is no large dependency on any single source of borrowing. On top of the substantial investments by NABARD and IFC, the management indicated that they have initiated the process for ECB. They want to further broadbase their borrowing and earning profile both, thus reducing dependency on any one asset class OR any one source of borrowing instruments thus providing more stability and sustainability to its earnings.

Declining Interest Rates and Positive ALM: The entire NBFC crisis has been all about ALM mismatch and the hue and cry around it. This is where gold loan and micro finance companies are very well placed. Due to their short loan tenures, they usually have positive ALM. So they are not at all involved in this mess and the whole business of restructuring your asset and liability profile which would have impacted profitability for at least 6-9 months. The bigger good news (and this I am speaking for the sector per-se) which the market seems to be ignoring is the consistently declining Interest rates. This provides a massive delta to the earnings of NBFIs and this will start reflecting their cost of funds and their profitability from Q3 onwards.

Return Rations: The return ratios continue to Improve. The ROE’S , ROA’s are best in class. If you combine the ROE and ROA and see it in conjunction with the NPA’s and Topline/Bottomline growth, you will realise that we are staring at a goldmine here.

Capital Adequacy: The capital adequacy is currently around 22% and the management said this in the concall that they will bring this below 20% by the end of this FY, which means that more capital will be deployed in their new business as the Gold Business is anyways a cash spewing machine. I see a fantastic future for all the 4 business of Manappuram in the current economic environment and I feel they have a good management team in place for all the 4 verticals.

My Estimates are that FY20 PAT will be around 1200-1300 Crs and I dont see any reason why this company should trade at less than 25000 Crores due to multiple triggers as mentioned in my post. The FY 21 Book Value will be around Rs. 80 and such a sound and seasoned business model deserves 4-5 times PBV .

Disclosure: Manappuram is one of my top holdings. I respect the opinions of folks who differ with me. I am extremely bullish on this company and its management.

21 Likes

I guess they have taken possession of 100cr commercial real estate they bought sometime back. They intend to launch many other verticals like AMC etc. Posting the link again on this forum. I don’t consider this as a great move though.

2 Likes

2 Likes

Asirvad Microfinance, a subsidiary of Manappuram Finance, has achieved a significant milestone with its AUM (assets under management) in the state Tamil Nadu alone crossing Rs 1,000 crore. This was accomplished by disbursing microfinance loans to over 450,000 women members. Asirvad Microfinance commenced operations in Tamil Nadu in 2008 and completed a decade of operations last year.

Asirvad Microfinance achieved another milestone in August 2019 when it opened its 1,000th branch in Bihariganj in the state of Bihar.

3 Likes

One minor correction: Muthoot Capital Services (vehicle lender) is owned by Blue Muthoot which is a different entity than Muthoot Finance (Red Muthoot). Long family history.

3 Likes

Manappuram Finance Limited

*Long term rating upgraded to ‘CRISIL AA/Stable’ ; Short term rating reaffirmed and *term loan Withdrawal

2 Likes

https://www.kitco.com/news/video/show/Kitco-NEWS/2535/2019-09-05/Gold-price-at-$10000-is-not-crazy-talk-says-Frank-Holmes#48_INSTANCE_puYLh9Vd66QY=https%3A%2F%2Fwww.kitco.com%2Fnews%2Fvideo%2Flatest%3Fshow%3DKitco-NEWS

1 Like

5 Likes

Why the promoter is keeping changing the growth rate and why it is necessary for him to appear in front of the media every month?

April:

May:

August:

And what others shared is for September.

3 Likes

When are they raising capital?

Today corporate tax rate was cut to 25%

It is the biggest gift for all companies especially those who pay higher taxes

In India NBFC s pays highest tax rate of 35%

Manappuram also used to pay 35% tax

Now it has to pay 25%

It will increase the profit by 15-20% immediately

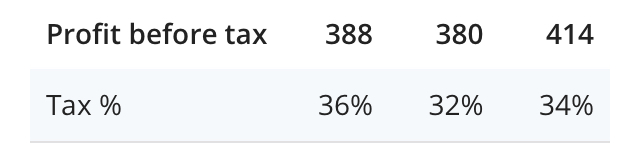

Now sept quarter profit before tax was 414 Crore

35% tax

So profit after tax was 272 Crore

Now with 25% tax profit will be 310 Crore given no growth (1240 annual profit )

At current price of 134 with zero growth

Price to earning comes 9.1 in 12 months

With 20% profit growth as expected by management PE comes 7.6 In next 12 months

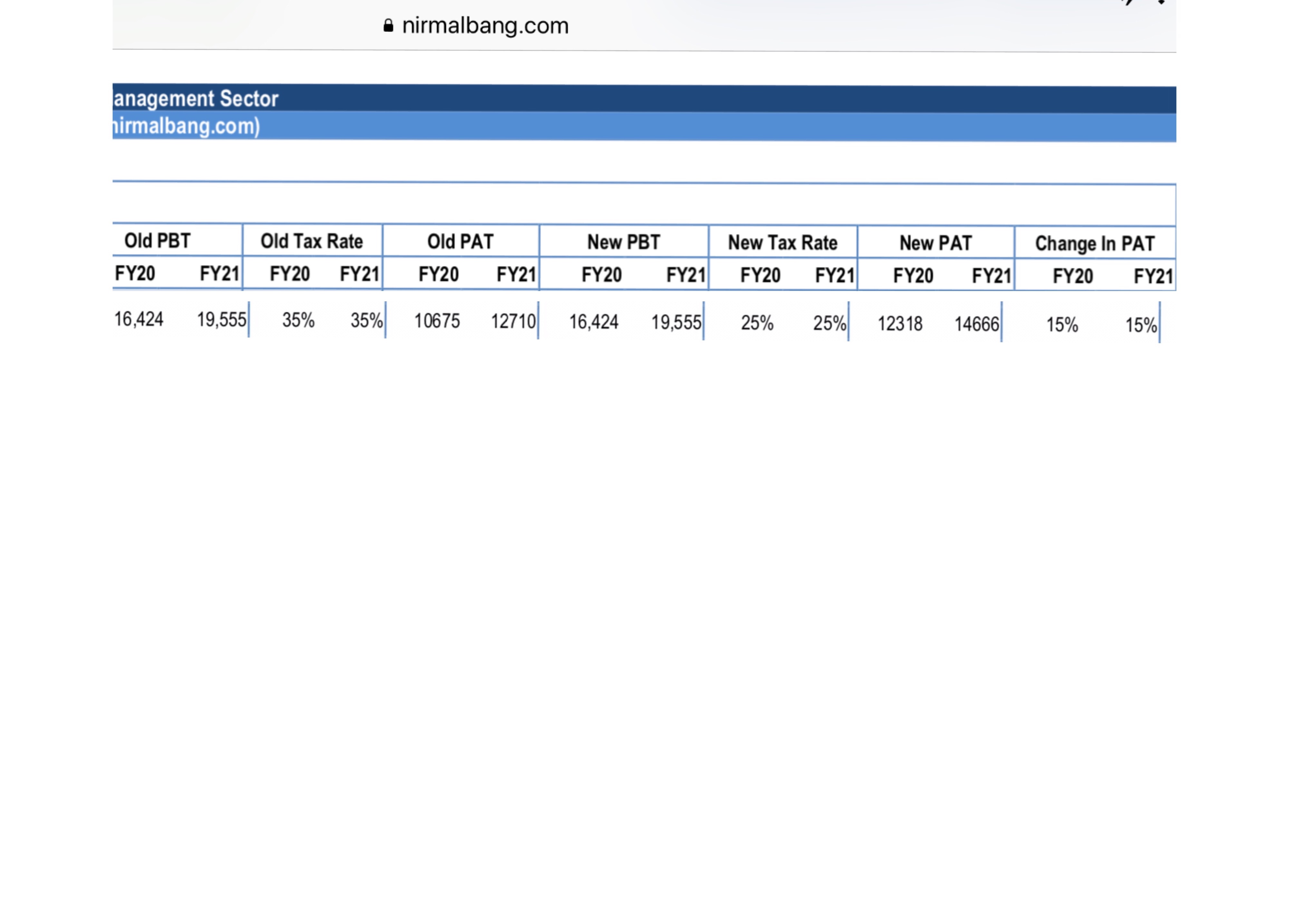

As per Nirmal bang report

Jim Rickards : If you take 33,000t and divide it by US$9.6 trillion, which is how much you have to back, the gold price comes to about US$10,000/oz.”

It is very possible that gold could touch 10000 dollars (6x from current levels if for some reason USD crashes )

We are living in a very uncertain world.

China and Russia can come up with crazy idea to introduce gold backed bitcoin like currency

Gold is like hedging in your portfolio

After reading this article It looks like physical gold is a very important asset

Paper gold is also risky

6 Likes