Really good to know the extent of exposure to Kerala. The good thing is that they have a good geographic spread to manage the risk.

2 Likes

Manappuram Finance Ltd

Highlights of Q1 FY19 results

Financials

- AUM grew by 24 % YOY and 5 % QOQ which stands to 16,600 Cr.

- Gold loan book grew by 16 % YOY and 6 % QOQ which stands at 12,500 Cr.

- Gold loan portfolio grew by 3 % QOQ and 11 % YOY growth in gold holdings s, which now stands up to 66 tonnes.

- Online gold loan or OGL, digital gold loan important focus area has increased to 37% out of total gold loans compared to 32% in the preceding quarter.

- PAT grew by 21 % YOY to 200 Cr due to remarkable turnaround in company subsidiary.

- Asirvad Microfinance closed the quarter with an AUM of 2,400 Cr, a growth of 33% year-on-year.

- Asirvad also made a profit of around 28.6 Cr compared to a loss of 16.5 Cr Q1 of the previous fiscal.

- Standalone Profit decline by 6 % YOY and because company had book other income of about 19 Cr in Q1 of last fiscal plus the impact of IND-AS.

- Good growth was seen in vehicle loan division. and Home Fin sun which closed the quarter with a compiled AUM of 1124 Cr up by 12.4% year-on-year from 1000 Cr earlier.

- Together all non-gold business of company contribute 25 % in the total revenue.

- Company cost of fund has increased marginally by 11 BPS to 8.77 % .

- Company capital adequacy ratio stood at 20.2 %.

- The home loan business was up by 8.5 % QOQ to Rs.406.5 Cr It now operates from 35 branches. The vehicles loan book stood at Rs.717.7 Cr, which up by 14.8% quarter-on-quarter and operates from 141 locations.

- The new businesses now account for 25% of the consolidated AUM. The consolidated financing cost was Rs.294.32 Cr. Average cost of borrowing during the quarter increased by 11BPS to 8.77%. The average cost has declined by 63 BPS YOY and 158 BPS in the last two years.

- Employee cost increased by 17.4% YOY to 169.8 Cr.

- Total consolidated headcount, which now stood at 24,717, a decrease of 0.5% QOQ.

- Administrative cost increase by 9.3 % YOY to 139.7 Cr.

- Depreciation cost increased to Rs.18.5 Cr, an increase of 16.6% YOY.

- Provisions and write offs for the standalone entity during the quarter were 11.3 Cr, Gross NPA was 0.7% as same as quarter ended Q4 FY18.

- Loss of assets due to thefts, spurious gold etc., only amounts to 0.2% of AUM.

- Company consolidated net-worth stood at t Rs.3,986 Cr as of June 30, 2018.

- Book value per share stood at Rs.47.3.

IND-AS numbers - Consolidated Numbers

o AUM grew by 24.2 % YOY to 16,618 Cr

o Income from operation grew by 12.6 % to 936 Cr

o PAT grew by 18.7 % YOY to 198.8 Cr from 167.4 Cr

o ROE stood at 20.3 % - Standalone Numbers

o Profit was down by 6.4 % to 171.60 Cr compare to 183.38 Cr due to service tax input credit of Rs.19 Cr carry forwarded to GST and credited to other income in Q1 FY2018. - Company has provided 100 % provision for loan due over 90 days. Company has provided 24 Cr excess provision as compared to RBI prudential norms. 100% of disbursements were made in a non cash manner.

IGAAP Numbers - Profit stood at 174.6 Cr for the quarter

- Gold holdings were 66 tons at the end of the quarter which is up by 3.1 % QOQ and 11.1 % YOY. Gold holdings are highest since FY2012. Total number of gold loan stood at 23.17 lakhs.

- Gold loan book stood at Rs 12,466 Cr up by 6.2 % QOQ and 16.2 % YOY

- Auction during the quarter were Rs 62 Cr. Weighted average LTV stands at Rs 1890 or 67 % of the current gold price. Interest accrued was Rs.307.1 Cr that is 2.4% of the gold loan AUM compared to 2.6% a year ago.

- Gold loan disbursements during the quarter at Rs.23,119 Cr compared to Rs.20,488 Cr in Q4 FY2018. The online gold loan book accounted for 37% of the total gold loan book compared to 32.1% in Q4 FY18.

- Asirvad Microfinance AUM grew by 33 % YOY to 2,438 Cr. Company made a profit of 28.75 Cr compare to 16.51 Cr loss in Q1 FY18.

- Company made a provision of Rs.3.42 Cr in Q1 FY2019 for doubtful loans

Key Highlights - Asirvad is the sixth largest in NBFC MFI in the country and company expect a significant contribution to profits from Asirvad Microfinance. Asirvad has 15.1 lakhs customers, 840 branches, 4,364 employees present in more than 22 states and union territory.

- Company is planning for a public issue of NCDs to raise in medium term funds has current rates. Last public issue of NCDs incidentally took place in 2014. Company clarify that gold loan are essentially very short-term loans where company have the leeway to raise yields as necessary to counter the higher borrowing cost.

- Company recently announced the acquisition of India School Finance Company, a niche player in loans for the educational segment where company see good attraction.

- Provision on gold loan has been made as an expected credit loss model or RBI prudential loan whichever is higher. Company diversification journey is running well.

- In the light of good profit, growth of gold loan, as well as Asirvad coupled with continued improved performance of diversified businesses the board has declared an interim dividend of 55 paisa per share, an increase of 10%. The capital adequacy at the end of June 2018 was 25.54%. The total consolidated borrowing stood at Rs.13,439 Cr as of June 30, 2018.

Q&A - What is the strategy for the Micro Finance business going forward ?

o Traditionally the Q1 growth in microfinance is subdued because company had shown a huge growth in the last quarter of the previous year. Company sub disbursement in the last quarter was close to 900 Cr and this quarter it was 670 Cr. The reason for the flat growth is company collection equaled the disbursement in the first quarter, which has traditionally what happens and subsequently in July company has increase the AUM by another 100 Cr. Company had disbursed 330 Cr and collected 230 Cr so the AUM will increase to about 75 Cr to 100 Cr per month and company should reach the target as envisaged about 3,400 Cr to 3,500 Cr. - There was a rate increase by 200 basis points in last two quarters so does company had done rate revision ?

o The rate revisions of microfinance is the RBI regulation is done based on the previous quarter rates so whatever new loans company take in previous quarter company add a margin of 10 % and revise the rates. So all the loans which company have taken earlier company have already lent given a margin of 10% earlier, in fact company have reduced rates from 22.5 to 21.9 from July 1, 2018. So, this quarter again based on the rates, which company take floating and incidentally company total mix of the loans or the floating rate loans are more or less insignificant. Company always go with the fixed rate so change in interest rate does not affect.

o In Gold loan there is an increase of 20 basis points in the cost of borrowing. Company is passing on that In the first quarter there were some decline, now that decline will be addressed during this quarter company have slightly increased in some of the gold loan scheme company have increased by 20 to 30 basis points, so the cost increase in the cost of borrowing will be passed on, it is being passed on now. - How will be the growth in cost remain for the year ?

o It is because company has increased the salary especially of lower level of employees, company minimum salary has been increased and also up to the field level, company have increased to ensure retention. This increase may not be repeated every time so that will not go to the extent of 17% that may not be, a sustained increase every year could be around 10% as far as employee cost is concerned that is sustainable. So the employee cost for the Q1 will be sustainable. - Will profit margins increase because of the cost remaining at the same level?

o Yes and also the opex will come down because the portfolio per branch is increasing - Other loans category again that has seen a relatively flat growth on a quarterly basis even though on a year-on-year now again where would like this book to end up at the end of the financial year ?

o The share of other loans, non-gold loans will go up beyond 25%. In first quarter it was flat but it will grow for next 3 quarters.

o The current run rate of commercial vehicle division is around 80 Cr, it will go to 100 Cr, the home finance also will grow in the coming months, so it will go up from 25% to around 28% as expected. - What is the extent of provisions that company have in the Balance sheet with break up of Stage-1,2 and 3?

o 85 Cr cumulative .

o In case of gold loan company follow RBI prudential norms and company is not in the provision. In vehicle finance up to 30 days considered as stage 1 and 30-90 will be stage 2 and above 90 will be stage 3 and company followed ED is around 1% and LGD at the rate of 60% as company do not have enough historical data and currently is 60%. - In vehicle finance does company only finance to Commercial vehicle or also finance to Two wheeler and Four wheeler ?

o Company have two-wheeler financing portfolio which company started a year back. The size of the portfolio will be around 100 Cr. Apart from commercial vehicles and two-wheeler company have entered into used car financing. The portfolio is very small. It should be around 25 Cr. - Why NPA for the commercial vehicle is high to 2.9 % whereas company average ticket sixe is very low to almost 6,90.000 ?

o Company have an average ticket size of 7 lakh and company cater to retail portfolio and company maintain its weighted average of around 18.5% and compared to industry. So company have to maintain its NPA level and it will be continue in level of 2.5 % by the year end. - Is the vehicle loan is unsecured ?

o No it is secured company have collateral backed loans. - In housing finance company have a very low ticket size that is 1.10 Mn then also company NPA stood at 4.6 so what is the reason for the high NPA ?

o This NPA percentage over a period of time has come down in fact it was around 4.8 as of March it has come down to 4.6. Company is also into higher ticket sizes to start with and some of this calls over a period of time are having some difficulties. And then company have actually scaled up their recovery efforts increased in a three pronged strategy one is in terms of soft bucket the solution, second is in terms of legal recourse and also in terms of negotiator settlement. So going forward company will be able to substantially bring it down during the course of this year. - Which segment will lead to the company growth in FY19 ?

o The gold loan, which is the major area around 75% as of now will grow at 15% that will be a good number in absolute growth followed by microfinance as microfinance MD had stated that they will grow at 3500 Cr. so CV is growing steadily CV two-wheelers etc., the run rate is around 100 Cr now, so which may grow to 200 Cr to 300 Cr, so the growth has started in affordable housing also. They are also dispersing, so that may reach around 700 Cr. - What is happening on the gold loan side as after so much time this kind of growth has come back ?

o Company is expecting double digit growth in gold loan. All regions all the years other than the demonetisation regulatory changes company have grown double digit. so that has come back, so it may not be short-term, it is medium term total of three to five years company expect a double-digit growth. - Does company see any other alternate products competing the SME loan or the unsecured personal loan , does that has any bearing on company customers ?

o In a country like India, which is a fast growing at a rate of 7.3%. With the growth of these products, the opportunities of this growth will definitely complement each other. - In Gold Loan what would be ECL model, would it be as low as 10 BPS or 15 BPS ?

o Gold loan ED is around 18%, but the recovery is very good in the case of gold loan, so the LGD days 0.63%, so overall the provision was much less than RBI norms. - In micro finance now the small finance banks have closed down reasonably because should company will get the market share or are some other players again becoming more aggressive any thoughts on that?

o No the small finance banks moving to the microfinance company to SSB has really opened out funding sources for the existing large players so to that extent funding to us becomes much easier that is the main thing that has happened because banks are lending more than 50% to those people and now they are not eligible for banks funding and banks are chasing large microfinance company, funding become that much easier for the company. - The rate of growth in microfinance is a little unnerving at a point in time when large established players were taking the range and price they are trying to calibrate so at which stage is company right now ?

o No, in fact the whole industry was growing till demonetization and subsequently it came down and last year industry grow only by about 26% to 28% and again in 2018-19 again the industry has now moved into a lot of risk mitigation efforts and as it given Asirvad company have move completely 100% bank disbursement that is only the major risk scenario, cash handling was one of the major risk and company is e planning to go about 42% in the coming year and as against 26% to 30% in last year. More or less the bigger players will grow only around that 35% to 40% this year that is company assumption. - How the competition is there with un-organised players in Gold loan ?

o Gold loan is growing and have a double digit growth in last 10 years other than the hit towards the time hits one with the regulatory changes and second is demonetisation other than that this is going at double-digit, so company expect the same double-digit growth to continue overcome medium terms five year. Many players are trying to enter this area because many could not sustain the business over the appropriate practices were not adopted so company is able to adopt and hope it could sustain. - What was the auction during the quarter?

o 62 Cr - On Consolidated AUM of company there is a other component and that has broadly remained flattish QOQ so any sense on that under consolidation ?

o Company dispersed around 60 Cr. That is the same amount that company had recovery and company expect this number to grow around 750 Cr in the year. - What is the outlook on the education loan that company has acquired because somewhere there is aggravated stress on this education portfolio at various geographies what made company acquire this portfolio and growth plans there ? What is the AUM of this book at current level ?

o One they are niche players. There are a few players of the country, then the team is good, they understand the product, they have scoreboards, etc., so each of the segments they are in so they have understood that segment well and will good response and practices are followed by the company and the prospects for growth company assess it is good and they are growing now, they have got good run rate now, so these are the reasons, so they will be able to report ROA of around 3% to 4% this is company expectation.

o AUM is 650 Cr and company expect it to reach 1000 Cr by the end of the year. - In housing finance segment does company is seeing any supply side constraint ?

o Company current run rate is around 30 Cr, month-on-month it is increasing by 5 Cr to 10 Cr, so company is targeting own customer base which stands at around nearly 40 lakhs, which includes gold loan, microfinance and other business, so the business is coming from that area also. - How much growth is company expecting in FY19 ?

o Expecting about 40% to 42% growth ending the year is about 3,500 Cr

8 Likes

The listing of this will be good value unlocking for the share as we will get shares of Ashirwad.

I disagree that listing of Ashirvad is great news for Manappuram investors. This is one reason many institutions would like to play Ashihrvad directly rather than through MFS shares. Whole idea of deploying extra cash and capital will go for a toss. Holding structure will invite discount for MFS shares. It will appeal to investors expecting 15-20% including div. Not bad as such but this might lead to another round of consolidation.

1 Like

Agree but the management has indicated that it wants to do this. I sense because it will be value unlocking for them. My sense is a company which is into too many businesses get discounted a lot more. Anyways when the listing happens we will get Ashirvad shares so on the value it will create value. Am i missing something here ? Would appreciate discussions on the same.

Don’t think they are talking about demerger which will result in share allocation. They own close to 95% and would want to monetise Ashirvad and list it at certain valuation most probably through IPO. There is nothing to unlock here since P&L is fully consolidated and there is no hidden value to discover as such.

1 Like

With adequate capital, improving operational efficiency, company looks well poised to capture growing loan demand of customer. Also due to regular auction policy of company, we expect no liquidity/working capital constraint issues. We also expect Asirvad to return to profitability and group to realize significant cross-selling synergies going ahead. Company’s focus on becoming a diversified player (with regard to product line and geographical-concentration) augurs well in terms of risk management for the company. We expect AUM CAGR of 16% over FY18-FY20E. We value stock at 1.9x P/BV FY20 and arrive at a target price of INR134 giving an upside potential of 34%.

During Q3FY17 and Q4FY17, reports of theft were reported in various branches. Management addressed the concern by deploying more security guards in all branches (3331) which resulted in spike of security expense from 3cr in Q1FY17 to 41cr in Q1FY18. Company has now sought Godrej to install cellular storage technology by which company expects to reduce quarterly security expense to 12cr.

Any reasons for the recent fall? Kerala issue has long been known, not sure if something else is missing here. Anyways to me fundamentals are intact and attractive at current levels to add.

Discl. Invested

1 Like

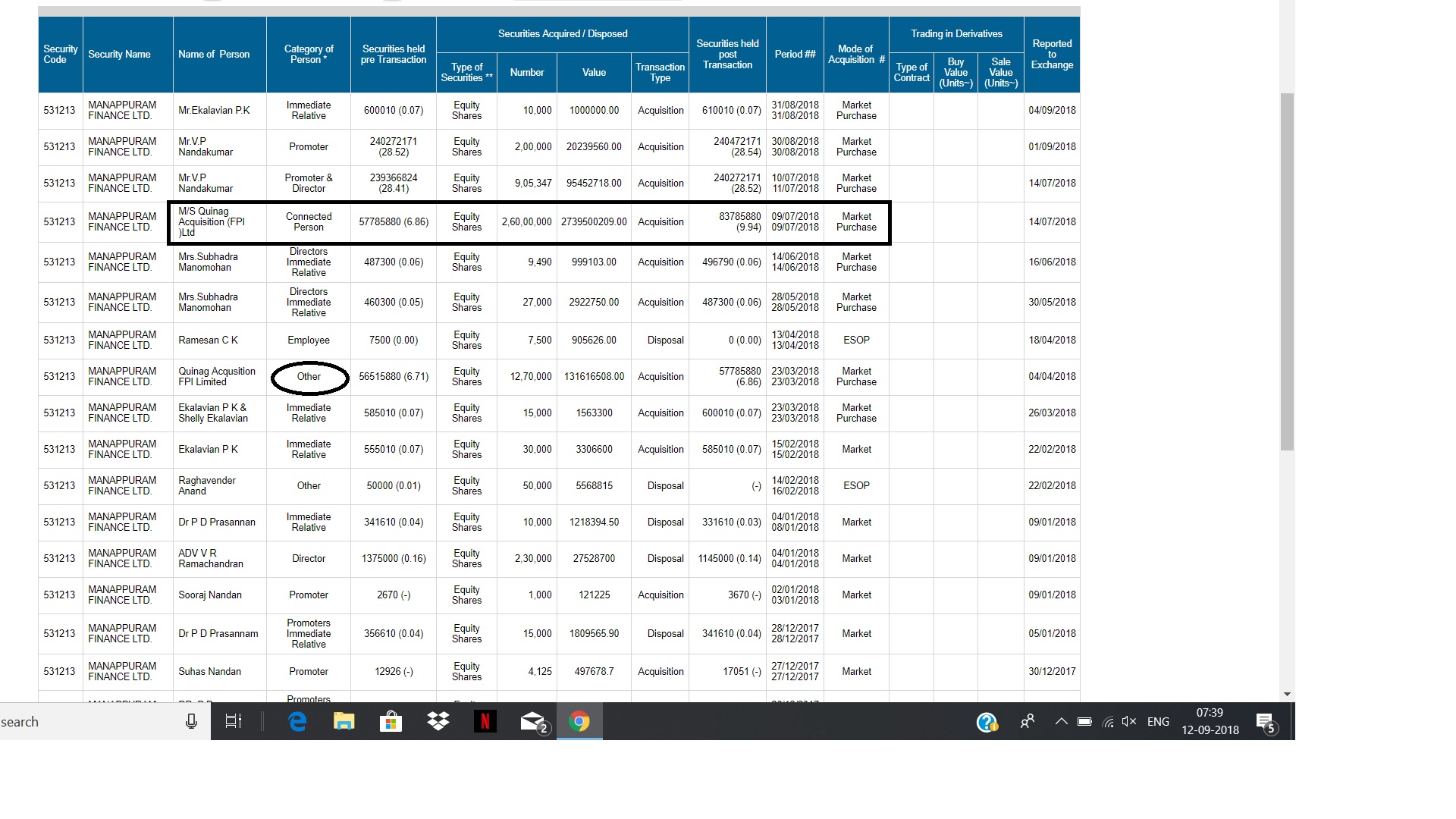

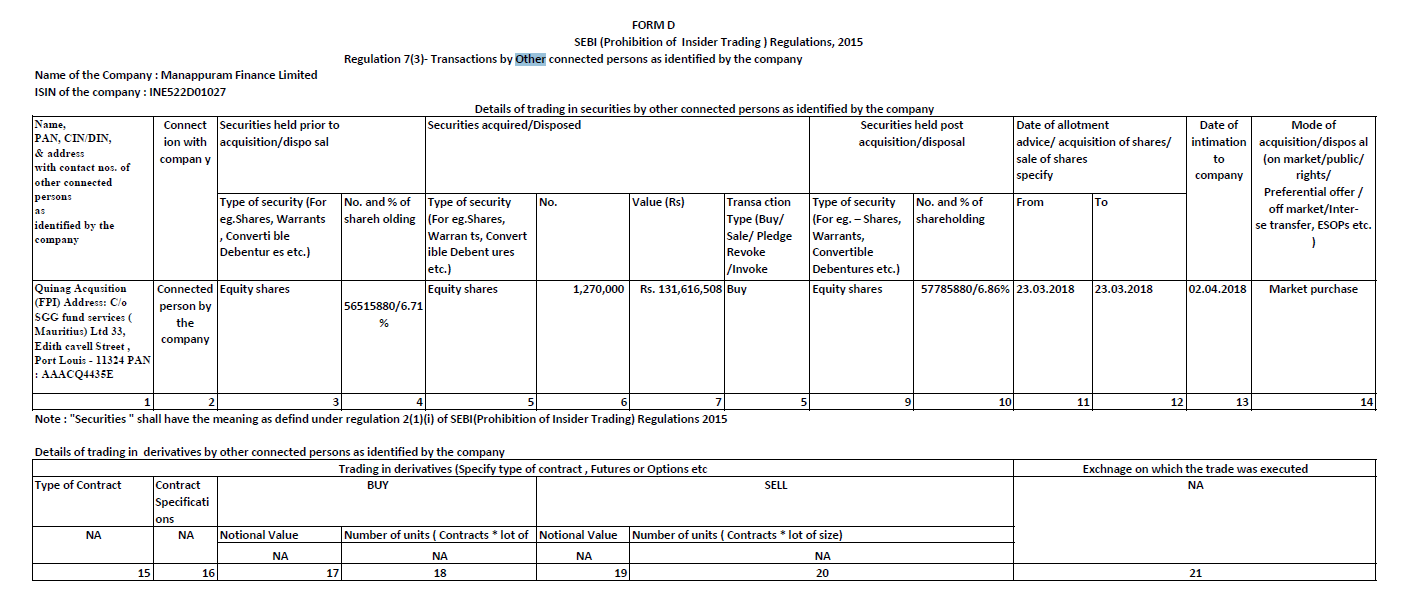

There is a peculiar thing that has been bothering me for sometime. This Quinag was “other” category of FII and after it acquired ~10% stake, it became a connected person that too an FPI. what is the connection here? Obviously fundamentals haven’t gone bad to justify this kind of fall. Gold in INR is stable, Kerala loan loss could be very small and manageable for it. In fact the upcoming liquidity squeeze in the wholesale debt market will be net positive for Muthoot and Manappuram due to their superior rating and high capital base.

The 2017-18 AR shows Quinag to be a FPI even at 6.85% holding.

couldnt understand what you are pointing at …

The fundamentals r only set to improve after their diversification. i feel the current correction is a risk-off play due to kearla floods.

During march 2018 it was categorised as “Other” and now it is a connected person. How did this transition happen?

2 Likes

Gold loan financers to be least effected as per crisil

1 Like

Hi, this may be because, as atishay pointed out, the Company has begun to disclose Quinag as connected entity. As per SEBI definition, a connected entity includes one which has access to non-public material information, which as a fund Quinag may have. Quinag itself seems to be managed by Apax, the global private equity house - https://www.apax.com/news/press-releases/2018/funds-advised-by-apax-partners-to-acquire-healthium-medtech-private-limited/

Disc: Not invested

4 Likes

What is source. I dont see it in https://www.bseindia.com/corporates/Insider_Trading.aspx?expandable=0

You are checking under Insider Regulation 1992. You need to check under Insider Regulation 2015. Please check here.

3 Likes

I think this nbfc crisis is very good for big players like manappuram

1)it will make difficult for many small players to survive

2)new players will think twice before entering this space

3) new players will find it hard to get the licence

4) loan requirement is a never ending story and there will be always a demand

5) As long as assets and liability Ratio is maintained there won’t be much trouble for companies

6) high interest rate will affect the Margin but the volume growth will compensate for that

7)risk reward ratio looks favourable at these valuations

5 Likes