What is source. I dont see it in https://www.bseindia.com/corporates/Insider_Trading.aspx?expandable=0

You are checking under Insider Regulation 1992. You need to check under Insider Regulation 2015. Please check here.

3 Likes

I think this nbfc crisis is very good for big players like manappuram

1)it will make difficult for many small players to survive

2)new players will think twice before entering this space

3) new players will find it hard to get the licence

4) loan requirement is a never ending story and there will be always a demand

5) As long as assets and liability Ratio is maintained there won’t be much trouble for companies

6) high interest rate will affect the Margin but the volume growth will compensate for that

7)risk reward ratio looks favourable at these valuations

5 Likes

Promoter Again buying shares from open market today. Total 29 Lakh Shares bought in the last 3 days and 35 lakh shares bought in the month of Sep.

5 Likes

Exactly my thought. When I decided to invest in NBFC sector I had tried to mitigate dilution risk by identifying stocks with strong cash flow to generate internal capital. That’s where Manappuram (Gold loan and strong CAR) and Edelweiss (advisory + franchise biz) came into my mind. I realise that the theory is still valid for liquidity issues as well. Many pure play NBFCs don’t have alternate sources of cash flow. Both these stocks will emerge stronger from this so called crisis.

4 Likes

Apologies if this has been mentioned in the thread before, but Manappuram seems to be financing other, lower-rated NBFCs as well, “as part of our treasury operations”, at around 14% per annum, as per one of the recent concalls. It seems to be a way to utilise the excess cash, as they are well-capitalised currently. The figure seems to be small though, and they haven’t had any credit issues, at least till that concall.

Disc: tracking, not invested

1 Like

Can you elaborate ypur point with source and complete details…

From the May 2018 concall:

Question: Now I will come back to that question later, but the second question is that the other loan which has grown by significantly – it has gone from 120 Crores to 592 Crores now that quite a significant jump what contributes to this others and what is in the growth in that and how do you expect that others to grow now?

Kapil Krishan: Basically this is some loan we give to other NBFCs and there we are getting a yield of around 14% and there is absolutely no delinquency. These are low rated but they are all rated corporates and basically these are companies are better due dilligence by IFMR, so IFMR as you probably know the go beyond what the rating agencies also do, they do a lot of field level study and based on that we also have our own criteria, they are typically companies, which have some external private equity investments so that we can be assured of the corporate governance and with good auditors, good promoters and a professional promoter, so these are kind of companies we prefer.

Question: How do you see that book growing? How do you intend on growing it because at the end of the day that is like a wholesale kind of lending business that you all are doing, now that is not your core focus, your core focus was eventually to do the smaller ticket, smaller size, if you can just guide us and what you want to do with this book going forward?

Kapil Krishan: Basically our core focus does not change but as you know our capital adequacy is very high right now, so we are pushing on all fronts, we will obviously prefer our core business growth, which is the gold loan and as you know we are putting thrust on home finance, Asirwad and vehicles business, so this is more like a treasury operation, it is not a core focus but since our capital adequacy is so high and we have the space for this and if you see most other NBFCs also do this."

2 Likes

his explanation for the same

2 Likes

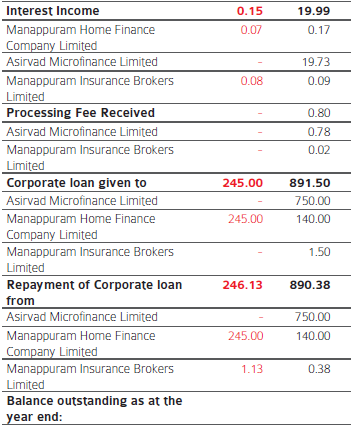

This a part of RPT of Manappuram with its subsidiaries. I find Interest income is very less on loans given to subsidiaries although company mention below that it is charging interest rate of 12% to 13% to them.

Anybody pls clarify.

2 Likes

Well done Suranjit

Manappuram Home Finance

0.07 = (245 x 1%) / 35 implies interest for less than one day - a THEORETICAL impossibility

0.17 = (140 x1%) / 8 implies interest for 3.6 days

at 12% p.a. or 1% per month

Asirvad

19.73 = (750 x 1%) / 4 implies interest for 7.5 days

Are these just “ACCOMODATION TRANSACTIONS” to comply with RBI Regulations for Quarterly reporting

OR

like you said concessional rate

In PRINCIPLE wrong, although at consolidated level immaterial as Asirvad is 98-99% owned and Home Finance 100%

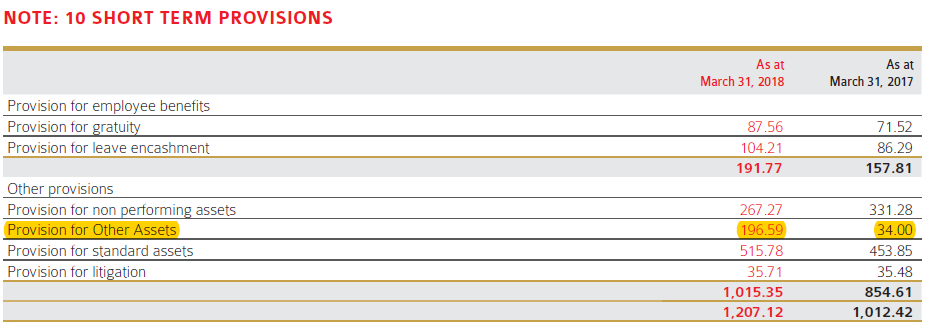

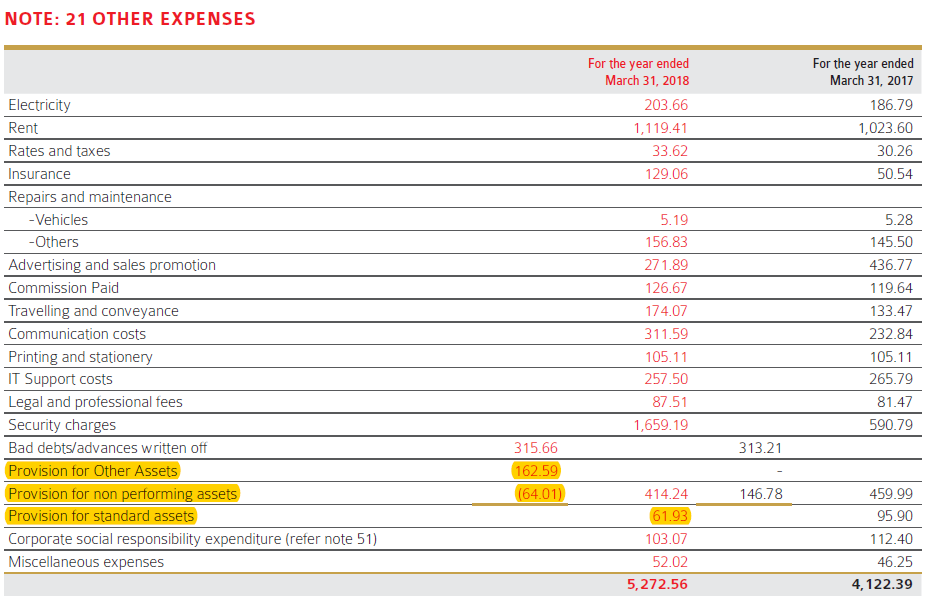

In short term provision they have provision for other assets of 196.59(2018) an 34(2017). what are these provisions for? The difference of 162.59(196.59-34) got expensed in P&L statement as other expenses along with both standard and NPA provisions.

I understand that provision for standard assets and provision for NPA cover their provisions for whole portfolio.

So what is this other assets they need to create provisions for. Is it for any regulatory compliance or something else? what I am missing here?

1 Like

isnt this a very old article 2016?

Some Diwali fireworks!! Checkout the results

Disclosure: Invested and added during the recent carnage.

Happy Diwali to one and all!

AJ

9 Likes

Do anyone have an update on the CFO? Mr. Kapil is no more a part of investor meets and his name is removed from the list of key managerial personnel.