@madhavikkutti Can you please share few names who are struggling?

Dear Lohiyaakshay, I was not refering to either Q1’18 results or to any peers struggling right now. I was talking about the 2015-16 period, when the company had faced a lot of adversities and still came up with good results. I believe that, true colour of someone/something can be best measured during difficult times. Please have a look at how Sandur manganese, Facor alloys etc had performed during the above period.

Agree. I have a good position built in. Invested between 275 since Jul last yr and exited at 520 this May and re-entered at 450. However i now am convinsed that its time to hold this one, I hope that better prices with a subsequent market falls will be a good opportunity fr all medium term investors to add this business.

@madhavikkutti Yes that is true.

I found the below link while searching for maithan alloys. If anybody have access to premium content, please share the highlights.

From annual report:

2015-16 capacity utilization 92%,

2016-17 capacity utilization 95%

Also,

1 Like

All is well, but I do not see any mutual funds or other big financial

institutions investing in the stock, They are also aware of the results !

I also found this company very good investment but could not hold this company as this was not gaining inspite of good results.

I saw that promoters are trading. Or I should see differently when in last few quarters promoters has increased as well as decreased stake. Change has happened in every quarter.

Moneylife Article Summary -

Brief description of Maithan Alloys - what they do 2017 results viz.a.viz 2016. Volume growth 7% Value growth 17%. Key reasons for growth stable RM prices, power subsidies from govt, better prospects for steel industry.

CMD says

a. Happy that in ferro alloys they are able to convert heterogeneous inputs (multiple geographies) into consistent quality output.

b. National Steel Policy 2017 could be a huge growth driver. Low debt allows company to acquire stressed assets at reasonable costs or by making incremental improvements in existing facilities.

c. Expect 15 to 17% operating margins.

4 Likes

There was re categorization of promoter few month back. So, the shareholding got affected due to that. Otherwise I dont see any trading activities.

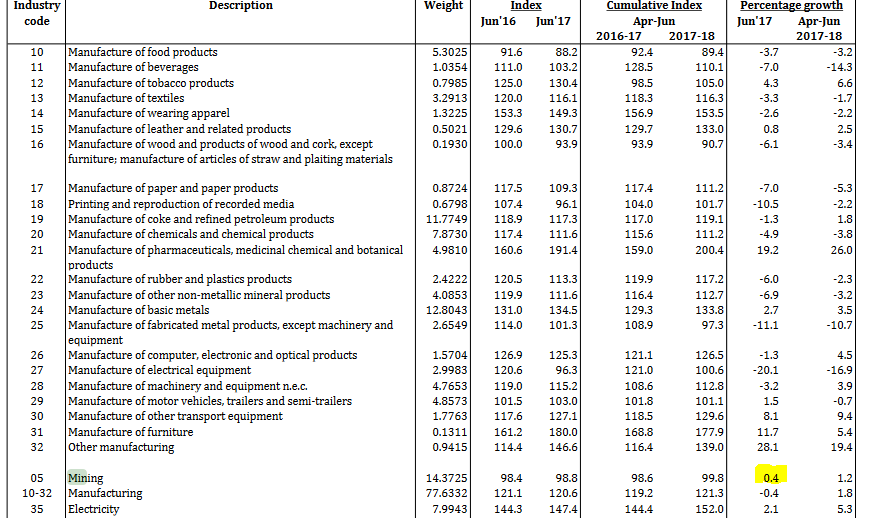

IIP data shows the level of industrial activity.

Overall IIP was negative for June 2017

For mining it was positive

1 Like

As usual set of uncommon results from the company same way muted reaction from the stock market.

Few questions which are worth posting to the management if some one plans to attend upcoming AGM on 26th August 2017:

– Why is the company not publishing consolidated results on quarterly basis? When big conglomerates working across segments can publish consolidated results, what prevents this tiny company to publish consolidated numbers?

– Last year eps of Rs 65 and cash eps of much more, why the dividend is restricted to just Rs 2.5 per share. Why not company publish dividend declaration policy so that market get some clarity on that front.

– Last year lot of promoters exit or de classified in most non transparent manner. Can some one ask what was the consideration paid to the outgoing promoters or what was the deal all about.

– Every time company talks about acquisition of stressed assets but when the opportunity was present last year or year before they failed to take advantage. So, why hold back money and not make a large payout to shareholders to let them enjoy the outperformance as market due to above mentioned points and many others are not ready to give decent valuation to the company.

Disc: Vested interest and biased views

1 Like

All things being equal- since in AR 2016-17, they mentioned, they are operating at 95% capacity, with no acquisition story coming an 75% of Domestic sales coming from SAIL ( Huge loss), how it give superior result in the coming month ? Debottle-necking of existing capacity will add how much capacity ? Not sure

Has anybody attended the AGM ?

Yes exports have gone up significantly.

Can anyone explain, despite good 82rs earning per share why management is paying a dividend of just 2.5 rs per share. Why are they not sharing the profit to it’s stakeholders?? Are they planning any acquisition in near future??

PS: Not invested, following closely.

@Pavankr2014 Yes they are looking for acquiring stressed asset.

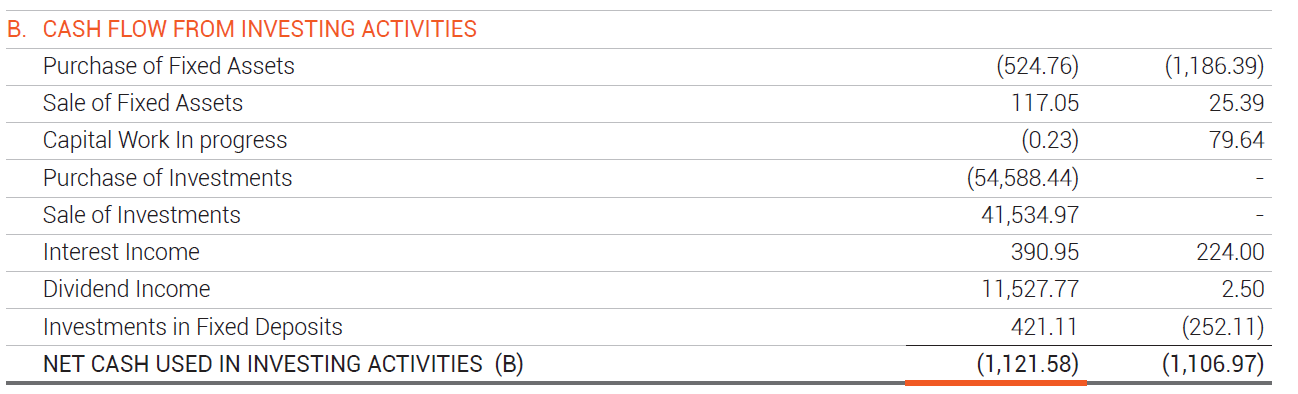

Hi,

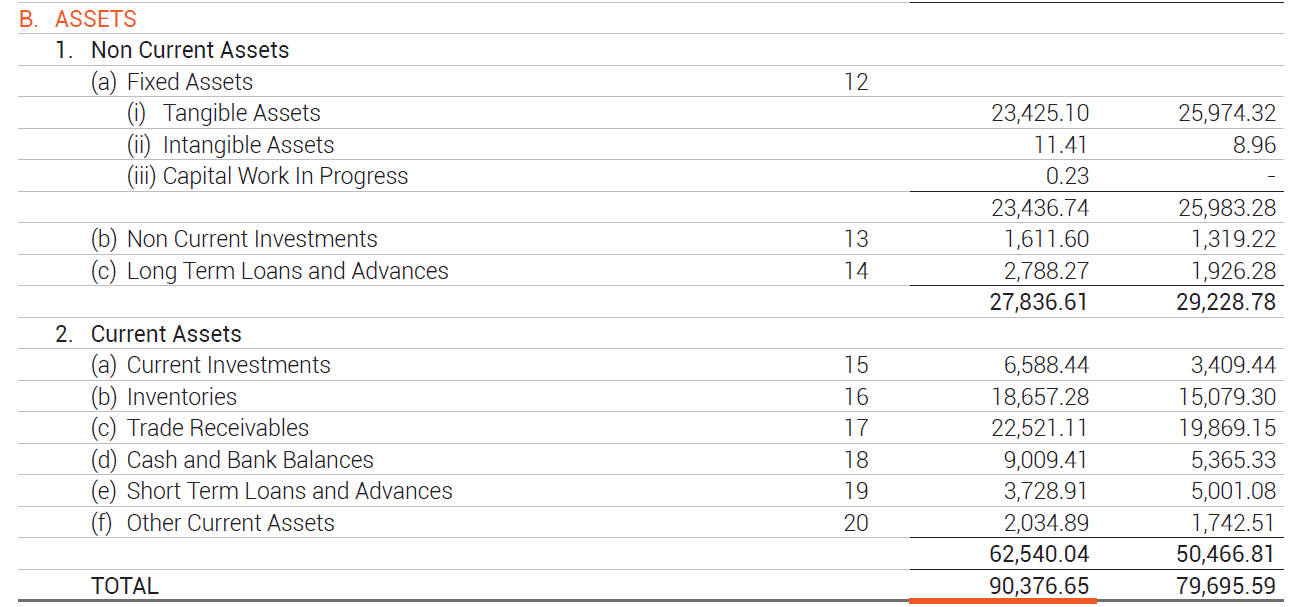

I was going through the annual report and it mentions purchase of investments worth INR 545 crore. Any idea about the details of this investment? Seems quite large given they didn’t do any such investments in the previous years

Seeing this figure in context to other, it looks like large part of this amount came from selling the old investment & adding the dividend income in it.

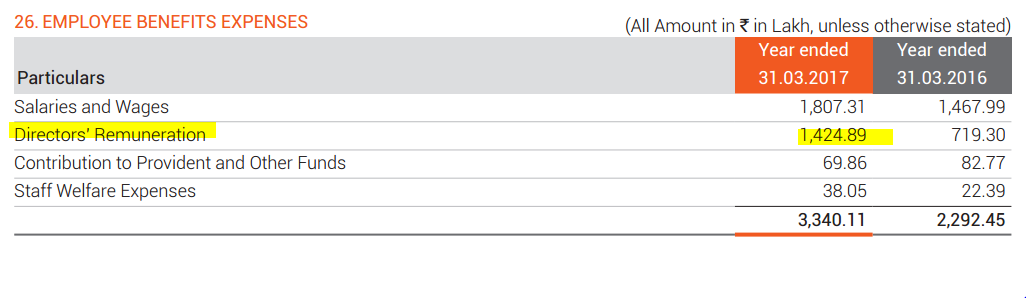

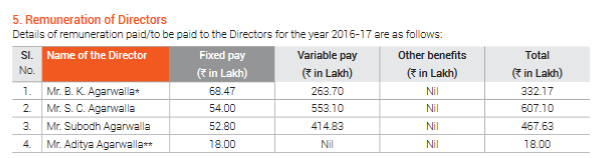

Although I do not have the answer to your question, I would give you couple of more from my end as you are on the quest for details. Chairman, CEO and CFO (father and the two sons) are taking a salary of ~ 15 Cr. which is just below the figure of What is paid to all other employees of the company?

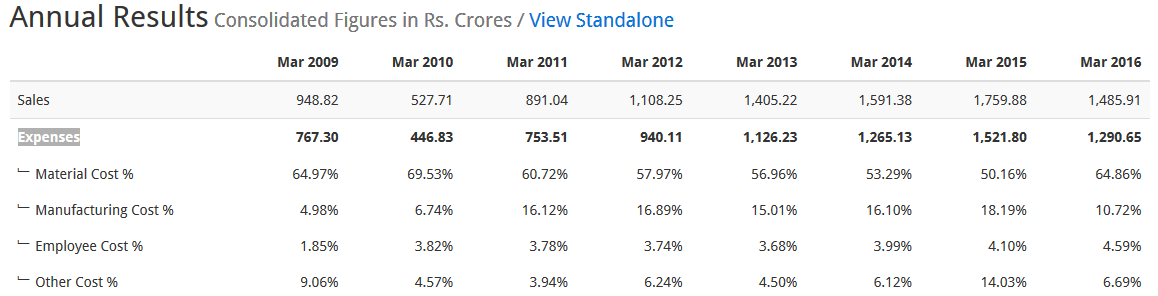

Also, the employee cost of the company is just 1% of the sales. is that a norm in this industry?

Disclosure: No holding. Quickly glanced as one colleague discussed about it.

From Screener:-

Maithanalloys-

Its closest competitor is sharda energy.

Yes, the director remuneration is high. Its due to high variable component.

Thanks a lot for your your responses @lohiyaakshay08 and @Surender .

@lohiyaakshay08 shouldn’t these investments show up on the balance sheet? However even if I sum both current and non-current assets, it shows up as ~INR 82 crore. Am I missing something here?

1 Like

Yes, Even I tried to look for that on balancesheet butnot got any. We need to talk to their Investor team.