Agreed,

It has potential to become true cash generation machine. But 2020 Mumbai license renewal will be key to their future roadmap and also 200 city gas distribution license which is about to be floated will be crucial for sector to prosper.

1 Like

2020 license renewal shouldn’t be problem as per managment and past precedents of renewals being awarded.

Below article predicts that gas distribution companies will report steady earnings

1 Like

I have been tracking this company for some time now and think it has real competitive advantages both over other forms of fuels and other companies.

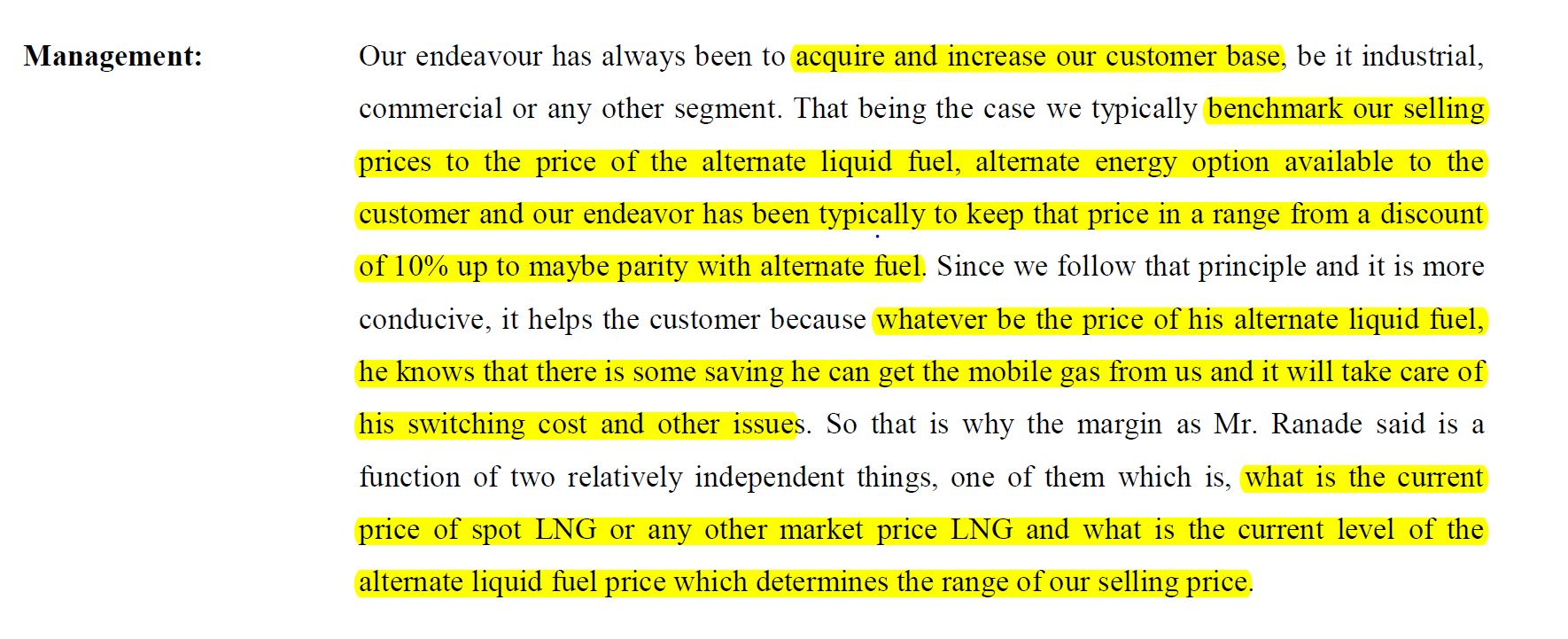

Here is an extract from the Q2FY18 concall about their pricing formula: (if you think about it, they are always at a price advantage, no matter the input cost increase!)

I will be closely tracking their bidding aggressiveness for other cities, Raigad expansion progress. Lots of opportunity in this scrip from the long term. Their moat will not extinguish unless we enter into the age of electric mobility which is at least 10 years away. Also, as noted by the management too, electric vehicles will displace the more polluting fuels first and only then CNG.

Disc: Invested

Good results from MNGL. YOY Revenue up 15% , PAT up 25%

1 Like

As was stated by the management in Q2 concall, the volumes are up by close to 2%.

I hope when we see more growth triggers realized, we will see even better volumes.

The recent surge in oil prices augurs well for the company as they cap their baseline prices as a function of alternative fuels with at least 10 percent margin.

The recent correction offered a good entry.

Disc: Invested

1 Like

Thanks for the indepth analysis and discussion:

Couple of questions I have are:

-

Any reasons for such low volume growth inspite of almost doubling CNG customer base from FY13 to FY17 (2.9 lakh to 5.4 lakh vehicles respectively). Given the cost benefits of CNG and Mahanagar being a virtual monopoly. Are customers not using CNG as much?

Source/Links for numbers above:

https://www.mahanagargas.com/UploadedFiles/_MGL_Investor_Presentation_Sept_2017_Final_017ad18e76.pdf -

Bit far fetched but long term sochna padta hai: The threat from electric is real in the long run. I read that hydrogen is going to be the sustainable fuel in future. Can the same infra and pipes be used or can hydrogen be blended with Natural Gas in future?

Would you guys even worry about this right now?

Link to research report: https://www.nrel.gov/docs/fy13osti/51995.pdf

My 2 cents:Since there is huge sunk cost in petrol vehicles that have already been bought, customers may prefer to convert to CNG rather than getting rid of their petrol cars. So CNG will continue to be a backup/alternate fuel even when electric cars get adopted in a big way.

1 Like

Recently I read that Maharashtra government formed a probe unit and ruled that CNG vehicles must have CNG inspection certificate every three years. This was due to malpractices of some companies during CNG installation on vehicles. The cab drivers are not obviously pleased with this inspection rule. So they went on to strike. Some details here. http://www.dnaindia.com/mumbai/report-mumbai-is-your-cng-cab-travel-safe-2600481

1 Like

As good an explanation there can be, though this is exactly the kind of short term thinking which prevents people from making good money in the markets!

It’d be good to know how much does an inspection cost but it’s once in 3 years so any cost will easily be offset by the benefits of CNG from a running cost perspective.

Also these kind of strikes don’t last for long since drivers have to make money too! So at most it’ll be a temporary blip in MGL’s P&L.

Hope they get Nasik and Aurangabad in upcoming bid rounds.

Bullish for this company’s prospects and willing to add more if it corrects to 900~! But willing to change my mind too if this issue is more than it appears to be!

2 Likes

Have you guys come across any reason too why BG is selling? This article doesn’t say anything about that. At the time of IPO too BG sold 12.5% at mcap of 4800 crore. It has since doubled at the current price.

1 Like

It would be very difficult to know why someone is selling. It could be due to the fact that foreign entity needs money for investing in some other field or change of strategy etc.

As a long term investor, we need to focus on whether anything changed for the company just because one foreign promoter is selling its holding. I think tailwinds for this business continues. So I would like to use this opportunity to buy into this excellent monopolistic growth story

Disclosure - investing from Jan 18, added more today

1 Like

The article says stake sale is for simplification of BG corporate structure to improve returns, nothing against MGL as such.

I was going through the numbers and money control shows MGL is trading at 19 times TTM earnings. Can’t help but wonder why it trails in comparison to IGL (33x) and Gujarat Gas (44x).

It’s true that MGL doesn’t have the benefit of mandatory CNG for public transport like IGL has. Nor does it have advantage of higher Revenue from PNG vs CNG like Gujarat Gas has.

But still recent announcements of mandatory CNG for Ola, Uber, albeit without a time frame, and progress on Raigarh should give a lift to this stock. Plus, upcoming auction rounds too should bode well.

The reason could be that these triggers don’t come with a definite time frame so the market is discounting this stock compared to others.

2 Likes

Stake sale had nothing to do with MGL’s business performance. It’s a part of Shell’s $30B divestment program over 2016-18 to reduce D/E ratio. Can read more about it here: https://www.ft.com/content/ca98a0d2-d40c-11e7-a303-9060cb1e5f44

Posting an extract from the Nov’17 article since it’s behind paywall :

"A $30bn divestment programme launched after the BG deal to cut debt was “almost delivered,” a year ahead of schedule, Shell said, with $25bn of disposals completed or agreed and a further $5bn in “advanced progress”.

This put its debt to capitalisation ratio, which was 25.4 per cent at the end of the third quarter, “within sight” of its 20 per cent target."

The scrip should rebound pretty quickly IMO.

1 Like

Some interesting links with respect to latest round of bidding -

Full ICRA report comparing old and new rules for bidding -

https://www.icraresearch.in/Research/DownloadSpecialCommentReport/1859

More details about the bid requirements can be found here - http://www.pngrb.gov.in/cgd-network-bid-2018.html

-

Bids for 174 districts have been invited compared to 100 districts allotted cumulatively so far. So the potential is huge.

-

A number of districts in Maharashtra are up for grabs. Since this is MGL’s traditional battleground, will be something to look forward to.

-

I also find comments of Chairman, PNGRB quite interesting - he said for earlier rounds many bids were received and awarded but not completed because of economic unviability. With the rules tweaked now and penalties in place, the focus is more on ability to meet infrastructure demands rather than bidding on tariffs and performance guarantees. MGL should be able to leverage its know how and local expertise to bet big at least in Maharashtra, if not other areas.

Views invited from @bheeshma and other members.

4 Likes

Mr. Dinesh Kumar Sarraf, PNGRB Chairperson, in the interview below has said that the bidding process is likely to be completetd by October 2018.

2 Likes

This is good news for MGL because it has historically not been able to find reinvestment opportunities like IGL. This is the main reason why its growth has been muted as reflected in its earnings multiple wrt to IGL despite having good return ratios and margins. The recent changes at the PNGRB helm are also a welcome change as I think the PNGRB did not have a chairman for a long time. Lets see how this pans out going ahead.

Best

Bheeshma

3 Likes

Came across this research report on MGL from an HDFC analyst. (I mention analyst because IMO only mentioning HDFC, the institution which has created huge wealth for itself and investors, lends a halo effect to whatever comes out from it. In the end, it’s just an opinion and can be challenged and could turn out wrong too.)

Mahanagar Gas - 3QFY18 - HDFC sec-201802122229211911563.pdf (366.8 KB)

Key highlights as follows:

-

Volume growth will come from industrial customers in and around Thane district. Industrial customers are price sensitive so the report expects pressures on margin. Plus, it says, potential customers in these areas are slow to switch to gas. (Don’t know the basis for this.)

My opinion: MGL’s Q3FY18 margin was at 35% and was as high as 38% in Q1 and Q2. This is very high to begin with and even if this comes under pressure, volume growth should be sufficient to offset that. Plus, it’s a very healthy trade-off if MGL compromises somewhat on the margins to boost volumes because of the convenience offered by PNG and the difficulty in switching back to LPG if prices rise. Also, Raigad is progressing quite fast which this report didn’t factor in:

-

For FY18, FY19 and FY20, the report predicts Adj PAT of 470, 440 and 450 crores.

My opinion : I don’t believe in this forecast. MGL has already done PAT of 373 cr till Q3. Why would it make less in Q4?

It’s very difficult to predict PAT for MGL when gas prices are outside anyone’s control. From what I have seen from MGL’s numbers, the company has been able to pass on the increase in prices to customers. There is nothing to suggest at present that will change. See for eg. gas prices for Apr-Sept’18 period were increased by ~11 bucks / mmbtu.

Gas price - Apr 18 to Sept 18.pdf (492.8 KB)

And MGL increased CNG, PNG prices effective April 1 citing increased cost:

CNG, piped cooking gas rates hiked in Mumbai from today | Mumbai news - Hindustan TimesSimilar story happened in Oct’17 as well: 13 lakh Mumbaiites to pay more for PNG, CNG from today | Mumbai news - Hindustan Times

Wonder if this report has factored in or can put a number on this ability (to pass on cost increase to customers) for as long as it’s there.

I have done some rough calculations to find out the impact of this increase in gas cost on MGL’s expenses: (I have assumed CNG and domestic PNG volumes for Q1 and Q2 FY19 to remain the average of past 3 quarters, i.e. 180 mmscm and 30 mmscm respectively. To make this calculation conservative, I have taken the cost increase on volumes for 2 quarters and selling price increase on volume of one quarter)

So for 2 quarters, volumes will be 420 mmscm = 16.67 mmbtu (at a conversion rate of 39,683 mmbtu / mmscm. Source : MoPNG which says 25.2 scm = 1 mmbtu)

Now the prices have grown by $0.17 i.e Rs. 11. So this translates to an impact of roughly 18.5 crores on gas cost.

On the price increase in CNG (by Rs. 1.23/kg) and domestic PNG (by Rs. 1.17/scm): The impact of this on revenues will be as follows:

CNG Price increase / kg = Rs. 1.23

CNG volume (average of Q1-Q3 FY18) = 180 mmscm

CNG volume (converted to kgs) = 126.4mm (mgmt claimed doing 1.41mm kgd in Q3 concall)

Price increase impact on revenue = Rs. 1.23 * 126.4mm = ~16 crores

Domestic PNG price increase / scm = 1.17 (1.17mm / mmscm)

Domestic PNG volume (average of Q1-Q3 FY18) = 30 mmscm

Price increase impact on revenue = 30 * 1.17 = ~35 crores

Now of course, the above calculation does not take into account some things :

- Gas volume increases, if they are met by PMT gas (which is double the cost of APM gas at around $6/mmbtu) will further increase gas cost estimate from 18.5 crores. (Though CGD is a priority sector and govt allocates 110% of demand from CGD companies admittedly with a lag of 2 quarters. So impact of purchasing higher priced gas from PMT will be there for 1 quarter. Plus, MGL had 78:22 ratio of APM to PMT gas till Q3)

- Any surcharge / transmission / marketing cost MGL has to pay to GAIL over and above the base price of gas.

- Industrial / Commercial LNG is purchased on spot basis and its cost will increase too. If the Industrial customers are as price sensitive as this report suggests, maybe MGL will not be able to completely pass on the price increase to them. I have not taken that impact in this model since it makes up for less than 15% of total revenues.

But these factors will more likely affect the scale of positive impact of (sale price hike - cost price hike) rather than the direction of it. Also to offset that somewhat I have already taken impact of cost price hike on 2 quarters volumes and impact of sale price hike on one quarter volume only.

Note: I have taken these conversion metrics from official sources but I am not a technical person to verify their accuracy. If anyone from fellow boarders has technical knowledge of this, please share.

Disclosure : Invested

7 Likes

This is what authorities say:

Transport expert and member of the Railway Passengers Committee Anil Tiwari said that more than seven lakh vehicles run on CNG in MMR, but there are not enough CNG dispensing points.MGL’s compression capacity should be increased to 50-lakh kg per day, he said. The way, the CNG vehicles are increasing each year, the MGL should add 10-15 lakh kg CNG each year at least for next four years. Only then would the problem of queues get tackled, according to him.

MGL is trying different ways to solve this problem:

“To ensure availability of CNG across its network area, MGL has an infrastructure of 223 CNG stations with 1,290 dispensing points spread across MMR. The present infrastructure has the capacity to dispense more than 30 lakh kgs of CNG per day, which can fuel over 11 lakh vehicles in its operational area.”MGL has also launched MGL Connect App, which will assist our consumers to know the nearest CNG station in MMR, for better fuelling experienceThe time for filling required is more for gas not because of quality of the equipment but because of the properties of the gas. To fill 5kg gas, it will take five minutes at present. But we are working on how to reduce the timing. A research is going on how to reduce the timing. Besides, we are working on out to reduce the queue. For which, the number of dispensers are being increased in many stations wherever space is available.

Also, they have been working on arranging mobile dispensers.

Getting land to set up new gas stations in the heavily populated Mumbai region is one of the main challenges for Mahanagar Gas. Due to lack of enough gas stations, queues outside gas filling stations have been getting even longer. To solve this problem, Mahanagar Gas is exploring newer options such as mobile gas dispensing stations. The company is looking to fix dispensers on its gas transport trailers, so they it can fill gas directly into vehicles, once parked at a safe place—a parking lot, taxi stand, etc. This move will help Mahanagar Gas reach new locations, where stations construction has been stuck due to land acquisitions or pipe connectivity issues. Since this new method requires regulatory approvals, it may take a few quarters before it materializes.

Overall I feel like they have to work on improving the turn around time of filling to accommodate increase in demand.

Disclosure: Recently taken a tracking position (bought 9 shares at 912) after the price fall during the shell stake sale.

6 Likes

There must be something more going on with the company. Is anyone aware of it? Stock is down another 2% today. Very close to 52 week low.

IGL follows a unique model to increase its capacity utilization. It gives rebate to fill CNG at non-peak hours i.e discount during late nights, and hence allowing them to better utilize the infrastructure.

Not sure, if MGL follows similar model or not.

1 Like