PNGRB launched 9th CGD Bidding Round On 12.04.2018, for development of

City Gas Distribution (CGD) networks for the 86 Geographical Areas (GAs) which

includes 174 districts (156 complete and 18 part), spread over 22 States and Union

Territories (UTs) in India. Based upon the bids evaluations PNGRB in its 79th

Board meeting held on 03.08.2018, approved issue of Letters of Intent (LoI) to the

following 18 successful bidders for 48 Geographical Areas (GAs) http://www.pngrb.gov.in/pdf/cgd/bid9/Ninth%20Round%20CGD%20Bidding-Press%20Release-03.08.2018.pdf

MGL’s all three bidding region are not announced yet.

Igl has won Meerath region and it’s 50% jv Maha rashtra natura gas has won Sindhudurg district.Only IGL know how much volume they can generate and what is the capex required.Both IGL and MGL was very conservative on bidding.

I personally like companies which take on their plates what they can digest and then execute well. IGL has NCR, Ghaziabad, Gurgaon, Rewari, and now Meerut, Muzaffarnagar & Shamali as well.

Then it has Pune and now a new one with MNGL stake.

Also, it has Kanpur and Bareilly with CUGL stake.

Earnings growth will now come if:

-

Execution is done timely(means maximum availability of CNG stations, quick action on PNG connection requests) and without debt, &

-

Districts allotted adopt the idea of a cleaner, cheaper fuel that is abundantly available.

I was surprised to see Mr Adani getting max districts in Gujarat & an established player like Gujarat gas getting just one (Did it bid for others at all?).

This, imo, boils down to the difference between entrepreneurs & bureaucrats & secondly the belief of the current administration that private players working for profits first will speed up natural gas development, provide better services even though they’ll charge more.

That said, I came across a comment on how MGL doesn’t respond to connection requests for long periods:

Disc.: Invested in both IGL, MGL & generally positive on the value migration to natural gas theme.

Iam also invested in MGL and IGL. I did a project on queing theory as a part of MBA course in one of the CNG filling stations in the NCR area. This was around 2008 and the waiting period was dependent on the pressure of the cylinder banks and if the pressure was less, you had a long queue. Although things have progressed, you still have a waiting time for refilling as compared to conventional fuels.

As a user of CNG car in Gujarat, it might be slightly cheaper to run than diesel, but the range falls short. You could run about 120km on a tankful and then queue up. I also felt the pickup was a bit less and the spark plugs needed replacement.

I bought my first share of IGL after the project at around 91 rs and have held on. Typically owners of pipelines/highways should give you lifelong toll kind of income. But there are risks with IGL/MGL. IGL took a dive sometime in 2013, when there was a PNGRB ruling on pricing.Being a government run company, the motive to do well is little and with private players closing in their glory days must be coming to an end. There could also be a possibility of a private player taking up the license when it expires. They pay IGL/MGL just a toll fee for using their pipeline.

You are right.Services of IGL on png is v poor.They hardly respond .In spite of I being from same industry and knowing several of their top people, it was v difficult to get them to get the connections done.It took almost 1.5 years in our society.u can gauge what will happen when mkt opens up to Pvt players.telecom is in example

Dixit Doshi: Just one question Sir, I understand we have license agreement till 2020 for Mumbai market so if

you can help us with what will happen post that how we will be renewing it and can the other

players also target this market?

Management : As per the PNGRB regulations, the infrastructure exclusivity for GA-1, which is Mumbai city

expires in 2020, but as per the same regulations entities are allowed extension of the

infrastructure exclusivity in blocks of 10 years provided they do not breach any regulations. It is

expected that the rollover will happen of this exclusivity.

Dixit Doshi: So if the rollover happens will you remain the sole player?

Management : Yes because usually the intent is always to have only one operator so unless there is some serious

default, second operator is not put in place or added.

Article refers to MNGL but gives insight into consumer behaviour…

(invested in MGL)

On 10thSo far, August 2018, PNGRB in its 80th Board meeting approved issue of Letters of Intent (LoI) to the 10 successful bidders for the following 30 Geographical Areas (GAs).

Till date- Out of 86 GAs, 78 GAs were announced.

MGL’s all three bidded GAs are still pending for approval.

http://www.pngrb.gov.in/pdf/cgd/bid9/Ninth%20Round%20CGD%20Bidding-Press%20Release-10.08.2018.pdf

“Nothing can stop an idea whose time has come.”

Victor Hugo

I’ve stayed in Pune for slightly more than a year in 2016-17 on rent. Piped gas connections were like a completely alien concept there and there’s residenti construction activity going on at a furious pace - lots of societies filled with young professionals.

MNGL currently has no visibility at all (no ads, no billboards, didn’t even see those small milestone like signs saying “MNGL pipeline here” like we find in Delhi) and LPG cylinders are norm of the day.

But cylinders a big hassle trust me. Whoever I talked with, whether living on rent or not, would any day want to opt for PNG since cylinders are so unreliable.

My landlord couldn’t cook food once because their cylinder gave up and the spare one was lent to someone. New one is not at your beck and call.

Rentiers have to purchase one from the black market so they don’t have to pay for a connection as they know they’re living temporarily.

If the company is saying there are no takers as yet, but they’re ready with infra to provide the connections, that imho is a very positive sign.

If the company invests in improving it’s visibility, carries out awareness campaigns to educate the people on benefits of PNG vs LPG, I’m sure these 2 lac odd pending connections would sign up day after.

The pros are simple and straightforward:

- People need to cook food for which they need gas.

- PNG is cheaper, more convenient (no ordering required, no prediction as to when cylinder will give up required) and more reliable (non stop automated delivery of service) than LPG.

- It’s also safer than LPG (cylinders blow up, stranger in your house etc)

They’ll find these points in any CGDs investor presentation

Just need to pick it up and paste it on billboards all across the townships and housing societies.

Disclosure: invested in MNGL through IGL and see this as a big opportunity. Whether the company is able to leverage it is of course another matter.

Adani Gas wins 21 cities out of 52.

As per below older news, MGL participated in the bid, but no mention of how many bids.

Came across this interesting piece on natural gas supply and demand dynamics emerging because of the trade tensions between US and China: article link

US is becoming the largest exporter of natural gas and China is already a big consumer but as there are trade tensions between the 2 countries, china recently imposed tariffs on US LNG.

This presents a good opportunity for India which can import gas from US at a cheaper rate.

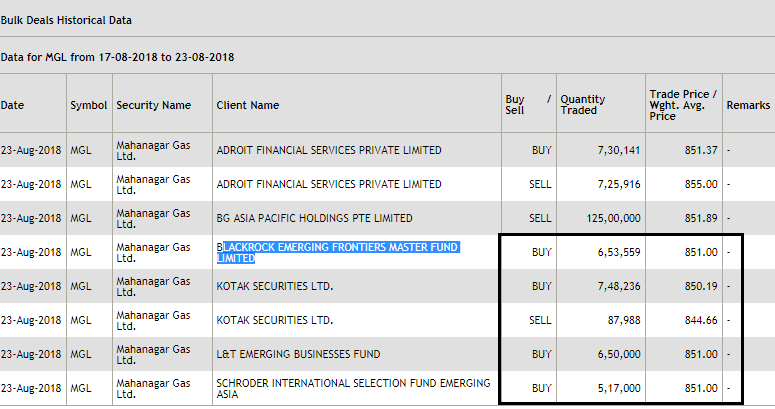

I’m reading some reports that Shell is paring it’s holding once again. Looking to sell 14% stake at floor price of 850 lower than the price in April ~900.

10% remaining stake is still locked with Shell up to mid 2019. Looks likely that Shell will completely exit by then.

Has anyone else come across anything related to the upcoming sale? Looks like investors should brace for more price weakness in the coming days!

BG Asia Pacific will offload 14% tomorrow as per below report. Floor price @ 851. It is bound to fall around 800 after this. Only near term trigger can be winning in one of the three GCDs they have bid for in recent rounds.

Some share has been bought by MF but that account almost 1/6 of the sell quantity .Clarity will emerge on MGL soon.Only NSE data

I believe that MGL is going to be a slow compounder from here on. Though the stake sale is not a reflection on MGL’s business but is a part of Shell divestment strategy worth $25b, MGL is after all a govt owned company and we all know how govt companies work. They have exclusivity in specific GAs and that’s going to remain its moat (competitive advantage) combined with availability of low priced gas and pricing power.

But on the downside, they’ll continue getting notices and customer complaints on account of the slow speed of work. That’ll also reflect on their financials (slow earnings growth -somewhere around CAGR of 5-7% going ahead I expect)

Till the time they have infra+marketing exclusivity, I’m staying invested in both IGL, MGL however slow their growth might be. Slow growth plus capital preservation are not such a bad combination to hold imo!

If i see the numbers for both IGL and MGL, MGL has higher EBITDA margins due to lower gas costs (i am guessing this is due to it being closer to the pipelines and hence lower transportation costs). If and when GAIL starts uniform tariff for its pipelines could it negatively affect margins of MGL and positively affect margins of IGL or would it be negative for both MGL and IGL as their current transportation costs would be lower than the uniform tariff.

Came across this today:

10,000 CNG stations to be set up in 10 years: Pradhan

Lofty targets for natural gas usage but these will be achieved to a certain extent. Which means still a long runway for CGDs growth.

Somehow I see an effort is underway to replace petrol, diesel and kerosene with CNG + Electric. Technology for CNG exists. Tech for EVs is still being developed for scale.

A newbie question. Doesn’t it make more sense to buy a Petronet LNG rather than gas retailing companies?