Rakesh Jhunjhunwala has increased his holding into Lupin from 1.89 to 1.92%. Though we should not try to copy ace investors , however it gives a bit of comfort in tough times.

Disc : Invested

Investor Presentation

http://www.bseindia.com/xml-data/corpfiling/AttachLive/536d267b-c277-46a3-9691-6c177d87989b.pdf

Along with the current general sell off, the results also didn’t help. Need to further dig in to see if there is a reversal of numbers on the horizon or not…

Position: Not invested, interested.

The way pharma companies have been posting big profits has been through steady pricing increases which improved their margins to the high 30s (35-38%). This is true for pretty much all pharma companies that have grown a lot between 2009-2015.

Companies like Valeant pharma have killed the golden goose by making mockery of drug pricing and ever since that Daraprim case came to light, the whole sector has gone downhill and has continued so. It has become political with Hillary Clinton taking it up and the drug pricing crackdown has been underway since.

Now the gross margins have dropped to high-teens which is almost half of where the margins were couple of years back. This requires serious derating and seeing how Lupin’s profits have nearly halved and margins dropped to around 17% from 27% a year ago, I don’t think the US is done with its battle on drug pricing and the price correction has still some ways to go. Buying Pharma (and IT) as a value proposition I think comes with a big risk.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/23a92169-19ec-41e8-87bd-7ca565c68346.pdf

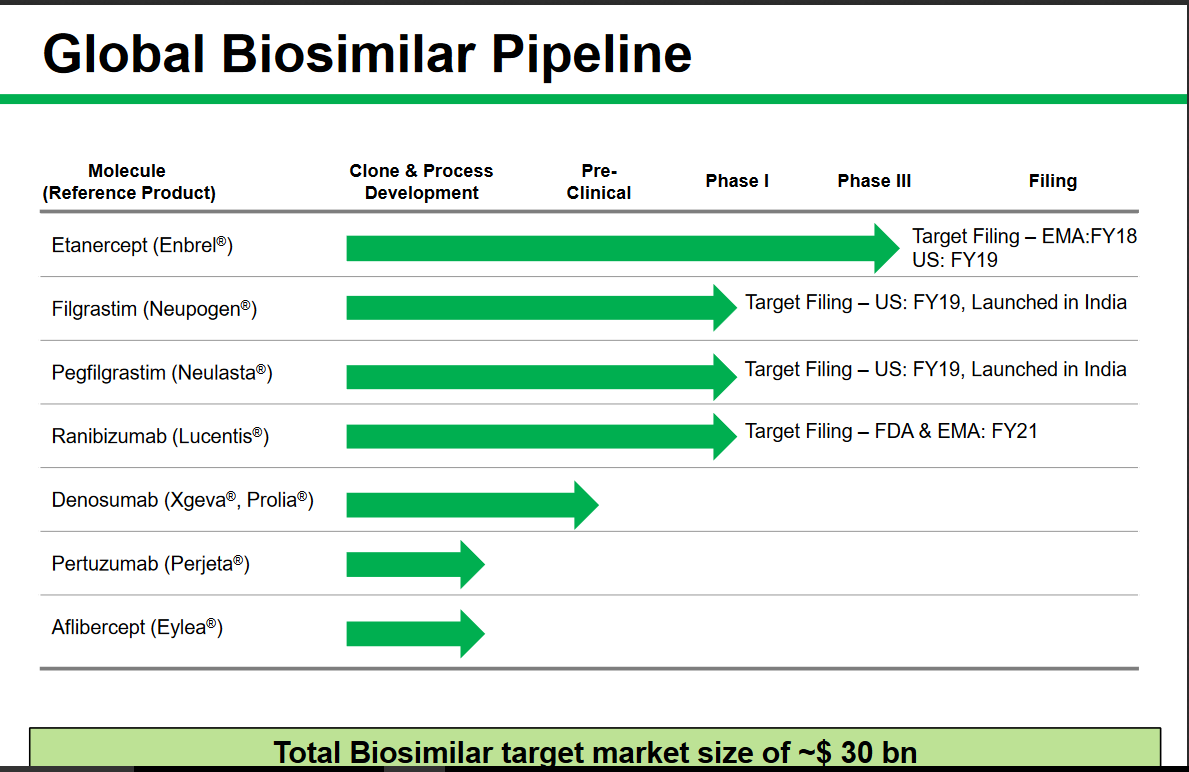

Lupin and Yoshindo’s JV — YL Biologics announces successful outcome of global

Phase Ill study for Etanercept biosimilar in Rheumatoid Arthritis

" YLB is the joint venture of Pharma major Lupin and Yoshindo in Japan. The Phase III study of YLB113

was a multinational randomized double-blind controlled trial of 52 weeks duration which included more than

500 patients with rheumatoid arthritis (RA) in 11 countries. It compared YLB113’s efficacy and safety directly****against Enbrel® (of Amgen/Pfizer) which has a global market of USD 11 billion (IQVIA MAT 032017), and is a widely successful biologic agent globally used for the treatment of multiple autoimmune disorders including RA. "

Can this be a big opportunity for Lupin. Competing with a drug having global market of USD 11 billion ? Can they gain market share from them ?

Etabercept Biosimillar will take minimum 18 months to launch in Europe.

US requires additional study to launch this in their market,

There seems to be a lot of push for biosimilars from Lupin. I keep seeing this from Lupin more than any other company in this space (except Biocon who is the leader in that space of course).

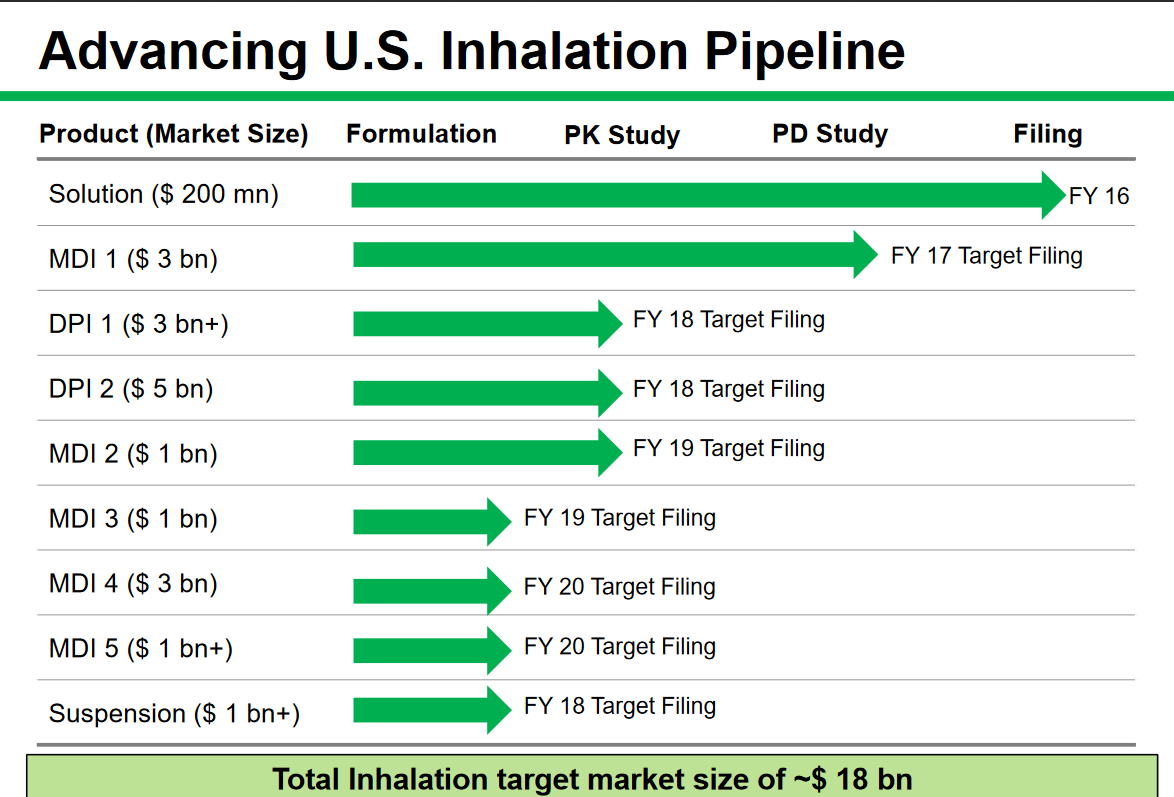

currently Lupins TTM Revenue is 16000 Cr. Since Etanercept biosimilar has completed phase III, out of 11 bn if Lupin can get 3 bn in sales, then it would mean we are getting a revenue of more than 20000 cr from this biosimilar itself. That is revenue could potentially double in 3 years from now. We are not even considering the other biosimilars in pipeline or the inhalation pipeline that I have put up above.

Assuming a minimum of 30000 Cr of revenue in 3 years and an OPM of 20 % ( currently 19 % ), assuming other things more or less same would translate to 3500+ Cr in PAT. That would mean we are getting Lupin at 10 PE now.

Disclosure - Wishful thinking. Have taken an initial position today.

Lupin Case Study on Value Investing

https://www.linkedin.com/pulse/lupin-case-study-value-investing-varun-aggarwal/

What you said is true @phreakv6. However, I do believe that opening up of generic market with FDA granting approvals at record rate and the gradual + painful but steady uplift in the systems and processes in Indian pharma creates opportunity.

The winners may be few and possibly new names but ten years from now, I reckon we may have a Pfizer or Amgen from India. Because really the sector overall has huge tail winds with demographic and disposal income shifts

In my view folks who have geographic diversification, head start into complex generics, biosimilar, investment in process and tech and partnerships on marketing and technology know-how - will succeed. And those that have money and ability to grow inorganically. Me too companies will fail.

I am invested in -

- biocon for their biosimilar lead.

- Natco for complex generics and potential of few blockbusters

- Ajanta for Africa and being disrupter in US

- Auro for sheer ability to file more Para IV than others

I have taken an initial position on Lupin. Trying to understand their future plans.

I would think this is overtly optimistic for following reasons -

- The initial trend on biosimilar suggest that the price erosion is worse than expected

- Biocon example shows that promise to reality can be a long walk. Plus, Anything that is not in phase 2 is purely speculation in my view. Those drugs may never see light at end of tunnel.

- Legal hassles and marketing costs, know-how may impact both ability to get due share and also cost of business

I am actually more optimistic of Lupin’s portfolio on inhalation

Lupin has aquired 8-10 company in last 2-3 year which is not a good symptom for a value investor. I am a new to this Sector. Can anyone explain me logic behind this. Senior comment please.

Dis. Small exposure…

a quick read of that rates makes you feel that quotes are repeated too often without the actual reasoning why the company would do well, or how can the investors be protected against further downside.

Generic pharma story is similar to what’s happening in IT services industry. Margins for effort-based services have peaked and IT companies are now focusing on value-based stuff to survive and improve margins to previous levels.

Most generic players are doing the catch-up in biosimilars; US pharma buyer consolidation isn’t helping things either. For Lupin, things won’t look up for at least next 2-3 years. One can get an idea if one goes through last few con-calls. Margins have shrunk considerably to 17% (back to 2010-11 ebitda margins), sales are peaking off, pipeline doesn’t look great, biosimilars are quite some time away. Biosimilar gestation cycles are pretty long and certainty is not guaranteed.

Price anchoring is dangerous. Just because it has corrected from 2200 odd levels to 740 levels doesn’t mean it is cheap or is a ‘value buy’! One has to look at the current business prospects to evaluate valuations. At 20-22x, with growth coming down, and not much growth visibility either for at least next few years, this is not cheap.

I have high regards for the management, though. They have milked the generics cycle amazingly well but failed to notice the change happening in the industry. Lupin might bounce back, but there is always an “if”, when you are not among the early entrants in a knowledge based business.

Is this video really reliable?

I flagged the above 2 posts for moderation yesterday. I guess the moderators are on vacation.

The video is a rant by some trader trying to make a quick buck by spreading rumors without any proof and the following post repeats it again. In fact, RJ upped his Lupin stake in Sep-Dec 2017 quarter and participated in the latest conference call.

I dont quite agree that pharma story is similar to the IT services industry currently. I think Pharma is currently at where IT was in 2002-2003. If you look at lupin its market cap is just 7 billion dollars. If you compare it to market cap of large pharma companies in US its pretty small. Pharma companies in India will over the next few years will close down the this gap with large pharma companies in US as they move up the value chain. Similar to what India IT companies did.They may not grow as huge as US pharma companies but the gap will narrow down. So there is still a large wealth creation opportunity for Indian pharma companies. However its might take time and needs lot of patience.

Disc : Invested in Lupin

One, i said generic pharma. Two, i compared two set of industries on a specific phase in their life cycles where companies need to evolve completely or perish irrespective of their market caps (by the way Lupin had 1 lac cr market cap at 2200).

Disruptions are coming quickly in every field be it IT, be it pharma. If giants like infy, tcs or generic pharma giants like reddy’s or lupin do not evolve their strategies towards value based services/complex generics…biosimilars…nce dev…outlook is grim.

Many of us didn’t understand this when lupin’s mkt vap was 1 lac cr…down to 50000 cr and we are still not getting it probably even at 30000 cr. Giants fall, unless they evolve. These giants have missed the trick…and next few years are going to be dull.

May be huge growth opportunity still left out for prudent pharma players of Indian origin, however Lupin"s case is different, as undercurrent negetive development will pull them back to tap the opportunity. When the core management team is breaking down, hope is diminishing. But other players like Ajanta and all will fill the gap.

People in general spread rumor undercover. It will be stupidity if someone posting own video to spread false news, since there may be by laws implications. This guy posted video about Lupin, should have done some research and study. Otherwise he will be in soup.