I am seeking advice whether this is time time to invest in long term bonds given the interest rates are going down. If they don’t what will happen will these sustain the current returns on 8-9 % if the expected tenure is 1 year. How will dynamic fund be a better choice, if it will be.

Yes, this is a good time to invest in long duration bonds. Though some expectation of rate cuts are already priced in. But if rate cuts do materialize you would certainly benefit from appreciation of bond prices as yields drop.

You can look to invest through long duration MFs, theres few that hold 2050 and 2060 papers. Also it would be easier to exit after 1 year when you have gained the requisite price appreciation.

Thanks Shail. Really appreciate your message. But let’s say that market(equity) takes a plunge in the intervening period - can I exit these debt funds without any losses to go into equity as I understand that longer the duration more the volatility (I’m checking is there a real chance of downside volatility in the intervening period)

If markets plunge, you would realize an instant price appreciation in bonds. Bonds react positively to a market crash. The longer your duration, the larger the gain.

A market crash usually is also accompanied by an economic downturn and a drop in inflation which helps in propping bond prices as yields adjust to the possibility of a lower inflation regime. Secondly, bonds being a safe haven asset, a market crash drives capital to safer avenues again propping bonds.

So to answer your question, “yes” if market crashes you can just redeem your bond funds without a loss (infact a gain) and move to equities.

Have there been instances where bonds also fell along with equity, other than 4 years ago? Doesn’t equity market fall also suggest a declining economic activity, and as such, sales, profits of listed entities will go down, and many debt funds hold paper of listed companies, listed groups, so is there a possibility of entire bond market going down? I am not particularly concerned about a single bond default, or a few, but can the bond market too go down with equity, if indeed there is a big fall?

FDs in banks, in PSBs to be precise, are safe compared to debt funds, but as debt funds score more over FDs, I also choose debt funds, but as I do not know to whom my FD money is lent, I am not and cannot be concerned about NPAs, but with debt funds, I know what is done with my investment, what paper is in the PF.

And also, obviously, I have no control over the returns of debt funds, as I don’t manage them unlike my stocks.

Hi Shail. Thanks a ton! Since I don’t come from financial background and thus go into analysis paralysis even though answer is apparent. I also appreciate this forum where people are discussing such quality matters where and discussions are quite coherent unlike other forums where group thinking is degenerates into utter chaos.

Check for traded volume. Also, check for duration of bonds it holds and if that suits your investment needs. I guess it holds medium tenure like 5-10 years duration.

Challenge with ETF is volumes and in extreme volatile situations there may not be retail buyer on other side of trade. Remember buying close ended Morgan Stanley Growth Fund (it was listed) at 30% discount during 2008 crash. With normal mutual funds you are assured to get redemption at NAV.

I am emphasizing this point because whole purpose of buying bonds is safety and lack of trade can jeopardize that safety. So I am not a big fan of bonds ETF unless market/liquidity becomes large enough so that I am always assured NAV.

I should have clarified. When I said long duration funds, I meant funds holding longer tenure Gsecs. No corporate bonds.

Bonds and equities would go down together during periods of rising inflation, since inflation leads to a drop in valuations for every single asset class.(except commodities)

Falling inflation improves valuations for every asset class, so in theory they all should appreciate during such periods. But if inflation is falling due to economic downturn, the earnings would fall too, so equities correct despite an appreciation in valuation. But government bonds on other hand appreciate.

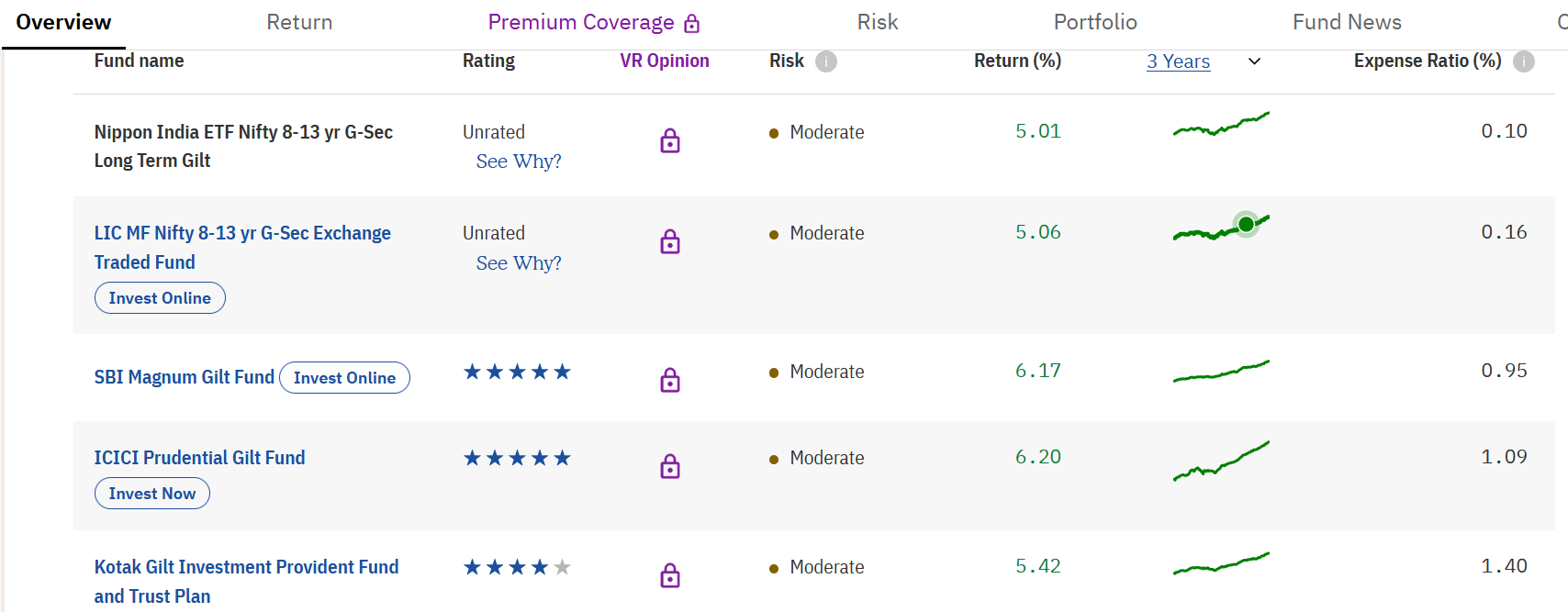

LTGILTBEES is a good choice but the average duration is close to 10 years. If you want 20+ year duration HDFC Long duration bond fund could be another fund to look at.

But if you wish to strictly invest through ETFs then LTGILTBEES is the only choice.

ETFs do not work the same way stocks do. The market maker has the responsibility to buy if someone is there to sell. just that you would have to take a hair cut on the value that you are selling at. The market maker can gather enough ETFs to form creation units and redeem the underlying securities. You could do it too, if you have enough units that they can form creation units to get the underlying securities.

Secondly, if you are unable to find a buyer you can always contact the fund house, and the fund house will help you facilitate the trade. They could direct their market maker to buy them off from you.

ETF units can be created and redeemed, but what you get is the underlying securities and not cash.

Are you referring to retail investor of institutional investors.

e.g. I have 100 units of the bond ETF and people are bidding for it at 25% discount to NAV.

What am I supposed to do? How will fund house help? How long will it take? What will I get in the end.

If I take a haircut, how much will it be? Doesn’t this defeat the purpose of investing in debt securities?

This was a hypothetical question. I don’t like Debt ETFs for reasons mentioned above.

I don’t want to be on mercy of fund house. When I invest in debt instrument as a small investor, I want it to be legally binding on fund house to redeem at NAV and credit my account next day. I used debt MFs regularly.

Also, why should one invest in these ETFs as returns are also lower that actively managed funds despite much higher expense ratios.

Thanks for the reply. My choice of LTGILTbees was mainly on liquidity, low expense ratio. I am thinking of combination of LTgiltbees, some long duration funds.

HDFC long duration would be a preffered choice since it doesnt have an exit load. you can exit anytime you want. as far as i remember sbi and nippon both have an exit load.

SBI long duration would be the best fund to allocate to if it didnt have an exit load. it holds 2060 and 2050 papers giving the maximum duration exposure.

Nippon Lakshya nivesh holds 2040-2050 papers thus the targeted duration is shorter thus gains from rate cuts are likely to be lesser as compared to sbi and hdfc

But Shail, I have a question. In the declining interest rate scenario even equity will also be rising, and if yes will it also not give good return? ( Apparently there are no easy answers in equity)