I read this, points are really sensational and like with all sensational things, if we think deeper each point, we would know that they are not that powerful as looks in first read…simple things, after 5 years if say someone is not putting money in policy, i would dig deeper was it market linked or pure protection before concluding anything…also no one knows what did the customer do with that money…did he switch to competetor or changed his type of policy or upgraded to better policy or simply the same person decided one fine that that he doesn’t need insurance anymore. Was it a corporate policy and he switched job etc etc etc…before concluding and commenting on future giants of India. I believe insurance and pension are basic amenities which with time would turn more basic needs of humans…regarding the sensational number metrics on penetration…well very well presented thought …infact I even know ppl who have 3 policies…so see one person has 3 policies sold to him by his 3 agent uncle’s so this is pinnacle of over penetration…but the same person when enlightened would sell all 3 and buy just 1 better and correct policy when he understands what insurance actually means and which company is worthy of his money…

This is view of Shridhar Shivaram of Enam

Now considered explanation of Ashish Vohra of Reliance Nippon Life

“There are various ways to measure penetration. I would argue that at an average level, the total sum assured that a customer carries today is less than one year’s total income and I would argue that it is not sufficient penetration. The total amount of protection that a customer carries in a Western world is probably 10 years of income

Even in neighbouring Asian countries, the total amount of protection a customer carries is probably three or four times and the word protection is really the sum total of all the policies that he owns. I do not quite share the view that insurance is a completely penetrated item in India. It is way short of what even the Asian neighbours have and some day, we would get to the developed world numbers.”

Personally I feel that Life insurance is still considered more as savings product rather than Protection product , may be as education of need for protection expand penetration will also expand in sum assured way (not numbers of policy)

Interesting interview on the same

Thanks

Ashit

Hello,

Does anyone have data of historical company wise/industry EV growth or can refer to sources which track this? Not able to find anything in milliman reports, swiss re sigma, irdai etc.

@rupeshtatiya @drgrudge have you looked at historical EV growth?

Does anyone know whether future appropriation amount in the Revenue account of life insurance companies should be taken as policy holder profit or shareholder profit?

Case Laws of income tax suggest it is not shareholder profit as it is meant for future use by policy holders but it seems to represent part of a life insurance company’s intrinsic profits so I’m having difficulty assessing this

Hi @rupeshtatiya , @Anant, @Gaurav_Agarwal and others. I had 2 queries about the insurance sector and was hoping for some help.

I wanted to clarify 1 point related to accounting. In the excel sheet that @rupeshtatiya has prepared to compare the big 3, he takes the entire Gross profit (in Policy holder account) of the insurance companies after tax payable by policy holder account. And then adds shareholder expense and income to that to come up with the PAT number. I have noticed that some companies like BALIC do not take the full amount of Gross profit to shareholders account and some others like the big 3 do. Should we consider the entire amount of Gross profit after tax and then make shareholder account adjustments to derive the intrinsic profitability of insurance companies? Or should we just take the reported numbers and consider the remaining residual in policyholders account that has not been transferred to shareholders account as future appropriation for policy holders?

Also, another point I wanted to clarify was that shareholder account sometimes makes contributions to policy holders account. This is done frequently by some companies and is part of Gross Profit of Policy Holder Account. Is any adjustment needed for that? I think in @rupeshtatiya excel sheet it forms part of Other income.

Any clarification would be much appreciated.

Thank you

https://static-

https://static-LIC agents selling pure protection plans are very minimal as they do not receive much commission on term plans. So people who do not want to loose part of their premiums as commissions to agents are looking for other top insurance companies like HDFC/ICICI pru etc. And also LIC does not have much plans which can be bought online and for NRI’s etc. But now with launch of Tech-Term plan which is purely online buying and term plan with comparable rates to peers (even 4-5% higher premium compared peers will still give edge to LIC due to their trust worthy and less troublesome during claims) will definitely give edge to LIC.

Observations from my personal buying experience too and working in Life Insurance industry.

First of all, operating profit i.e. surplus in policyholders account is more relevant metric to measure to strength of insurance companies as compared to PAT. In operating profit, one can adjust for any investments done for new products or one-time brand, A&SP spends to get the strength of the business.

Funds for future appropriation comes from two sources -

- Most of the payouts in policies happen at the end of the year/policy vs. on quarterly basis. So any additional surplus might be transferred to FFA for 2/3 quarters & then disbursed at the end of the year/policy year.

- Additional provisioning as a conservative measure based product specific or macro/industry specific developments. It might just be there even without any development as kind of floating provisions banks do.

There is no easy way to get split between above two.

(1) is an accounting matter & (2) either represents conservatism or incoming worsening in underwriting experience.

Overall, much better to focus on operating profit instead of FFA or PAT.

Shareholders have to contribute to policyholder accounts in the early stages of product so as to cover policyholder liability. IRDAI requires this to be done at product level - instead of portfolio level.

I did go into minute details of the numbers to understand the industry at first but I don’t do it very often now. Operating profit or Surplus, EV, VNB margin and growth, Unwind, RoEV, new product innovations and risk controlling measures are broad things I track.

Hope this helps.

That helps a lot Rupesh, thank you

Hi , @rupeshtatiya , I am novice in insurance sector . My question may be very basic

You suggested to analyze earning growth for insurance companies it is better to check EVOP growth rather than EPS growth for insurance companies .

So if we can check same for HDFC life ,EVOP growth is 20% whereas EPS growth is 10% . So if it keep going and stock price moves as per the function of EVOP growth , one point of time , HDFC life will have like 150/200 PE . Will it be normal as per the insurance company history? Or in future PAT growth will capture the rate of EVOP growth ?

Following is the response I have as of now, I was hoping to find time to write much detailed response.

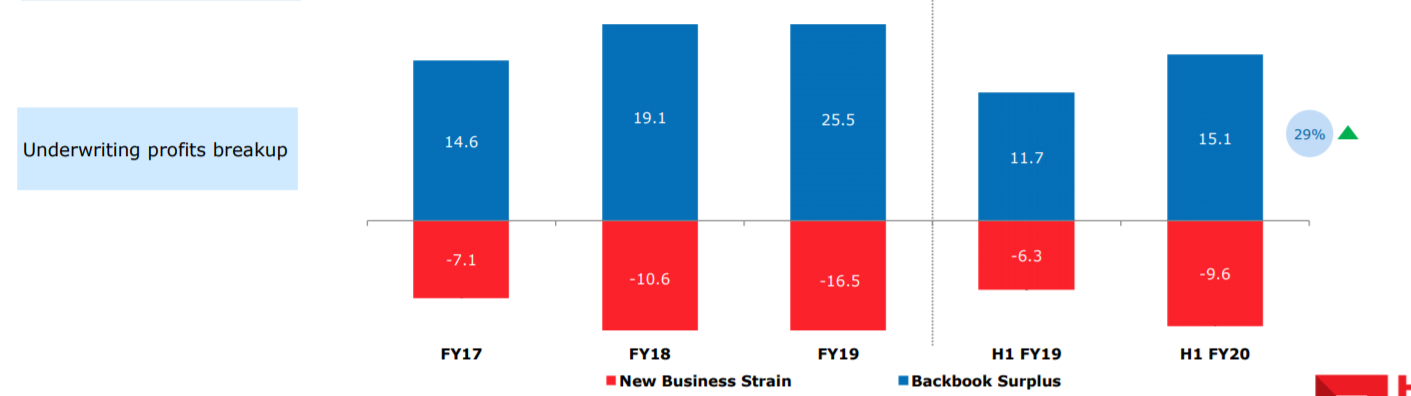

From HDFC Life Q2 PPT →

They have provided breakup of back book surplus & new business strain.

Above figures approximately match with the accounting surplus.

Few things →

As you can see that backbook surplus grew at 29% for HY20 but new business strain grew at ~50%. This resulted in accounting surplus growing at just about 10%. If you see FY17-19, backbook surplus grew by ~75% in 2 years which is pretty high growth rate. But new business strain more than doubled in this period.

This period is marked by several product introductions/scale up - like Credit Life, Sanchay etc.

So PAT growth will be higher if new business strain growth comes down. That will happen when

- The pace of new product introductions slow down or new product introduction with lesser new business strain.

- New product premium will decrease as a % of total premium (e.g think LIC with very large renewal premium & relatively less new business premium)

Over the long term, high VNB margin & high EVOP - shall translate into higher surplus & all the growth rates shall converge.

Just that HDFC Life has been really aggressive in new product introductions as well as new business premium growth.

Two points I was hoping to connect better were -

- Calculation of backbook surplus & new business strain. To calculate this, all the accounting lines have to be split into two parts - existing & new (e.g. actuarial liability for existing book vs. new book). operating/employee costs. This is hard to do.

- Linkage between VNB, Unwind, EVOP & Surplus/new business strain.

May be some other time.

Hope this helps.

Don’t know if it is right thread but this might be the first instance of any private insurance company going bust.

I thank all the VP contributors for making this thread a fantastic pitstop for somebody to learn on Insurance valuation in India. I got interested going thru the some outstanding work done on this topic. hats off!

While going thru Berkshire gyan on float management, i stumbled upon their top equity holdings ( Apple, Well Fargo, Coca Cola , Kraft etc.) .

Is there a place / link that points me to the top Equity Holdings of these 3 listed Insurance companies ( SBI, ICICI n HDFC). I tried a fair bit and couldnt locate anything meaningful.

For example- this is what I could gleam from HDFC Life.

Their AUM is approx 1.2 Lakh crores ( 62:38 split between Debt n Equity). That means - they hold `48,000 crores worth of Equity investments …isnt it ?

While the Annual Report is quite detailed ( 600 pages) and talks about investments at a scheme/ fund level … i couldnt find any aggregated info at HDFC life level.

Any expert opinion please ! thanks

V.good report. Gives broad perspective of insurance business in India.

Does anyone has comparative financial analysis of insurance companies?

IRDAI has not released monthly business figures for October 2019…Any change in frequency of reporting ??