Lemon Tree Hotels Limited (LTHL) is India’s largest hotel chain in the mid-priced hotel sector (2-star to 4-star) in terms of ownership, and the third largest overall, on the basis of controlling interest in owned and leased rooms. It is the ninth largest hotel chain in India in terms of owned, leased and managed rooms.

Company has created three hotel brands to capture middle-class Indian guest’s needs.

Brand

Category

Lemon Tree Premier

3.5 - 4 Star

Lemon Tree Hotels

3 Star

Red Fox by Lemon Tree Hotels

2 Star

Company operates across entire value chain from land to guest which means they acquire land, design hotels, develop hotels, own hotels, manage them and market/brand them.

100% subsidiary which provides in-house project design, project management and project development capabilities to the group as well as third-party owners for hotels that they intend to manage.

b) Carnation Hotels:

JV with Rattan Keswani (former President of Trident Hotels, Mumbai) with 65% economic interest.

Carnation is focusing on asset-light management contracts with third-party owners

c) Fleur Hotels (Asset monetization):

In 2012, company created JV with APG (world’s 3rd largest Dutch pension fund) called Fleur Hotels.

Lemon Tree contributed certain completed and operational properties into JV for 60% stake and APG matched it with large capital infusion by taking 40% stake.

These funds were used to develop new hotels. This enabled company to leverage their development and operating expertise and in the process earn development and management fees from these new hotels.

Company intends to use asset monetization strategy in the future to fund both organic and inorganic growth opportunities and expand owned hotels portfolio without investing more cash from balance sheet.

Strong Pipeline:

Company has very strong pipeline which is 65% incremental to their current portfolio.

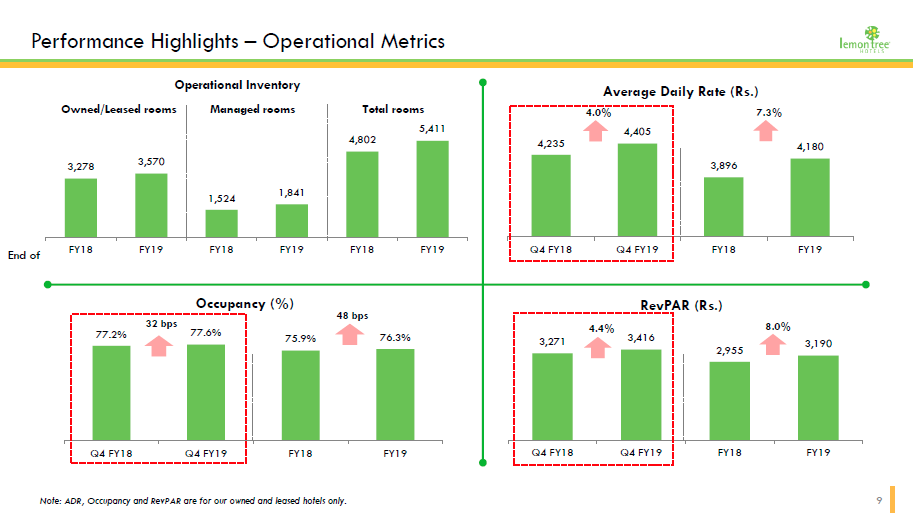

~ 870 owned/leased rooms and about 790 managed rooms totaling about 1,660 rooms will be operational by May 2019 .

The remaining hotels and rooms will be operationalized by FY21 .

Total count then will be 80 Hotels with 8,236 rooms

The project cost of the current pipeline is roughly Rs. 1725 Cr, of this Rs.930 Cr. has already been deployed by the end Q1FY19.

The balance investment of about Rs.795 Cr. will be mainly funded through internal accruals and deployed in a phased manner over the next three years.

Of the above, approx. 1000 rooms are being added in Mumbai which is demand dense and highest ARR market.

Other rooms are also added in locations which are demand dense like Pune, Udaipur.

There are more rooms being added under Lemon Tree Premier which has higher ADR compared to other two.

Company expects significant price hikes and higher Occupancy ratio over next 3-5 years.

All of these put together will significantly improve blended ADR and Cash Flows.

Key Metrics:

Cash Profit:

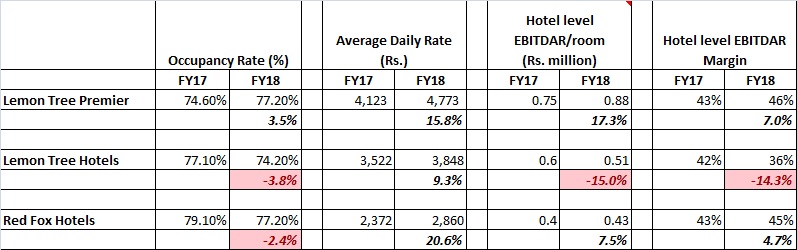

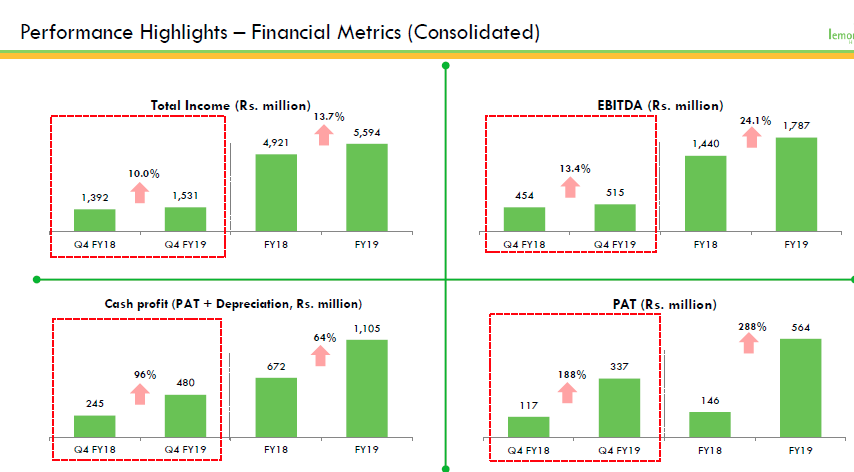

Hotels are appreciating assets and therefore only ~10% of depreciation reserves are used for asset upgrades / replacement. Company made Cash profit of Rs.67.2 Cr. in FY18 as against Rs.46 Cr. in FY17 (increase of 46%)

Average Daily Rate (ADR):

Increased by 13% year-on-year to Rs.3,896 compared to Rs.3,449 in FY17.

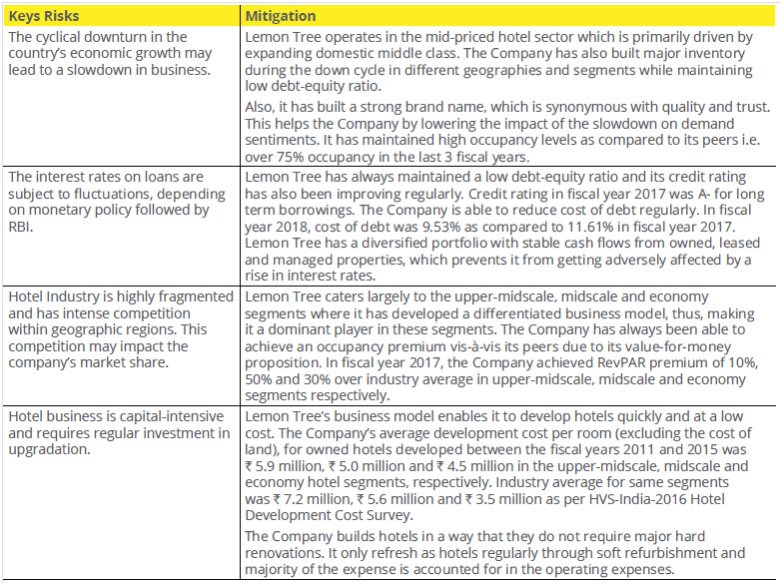

Is there any reason to expect this change? Given the company operates mainly in middle-class segment, I don’t expect them to have a significant pricing power. It can have pricing power if majority of its customers are from business segment rather than leisure. Please check if we can find any data on that.

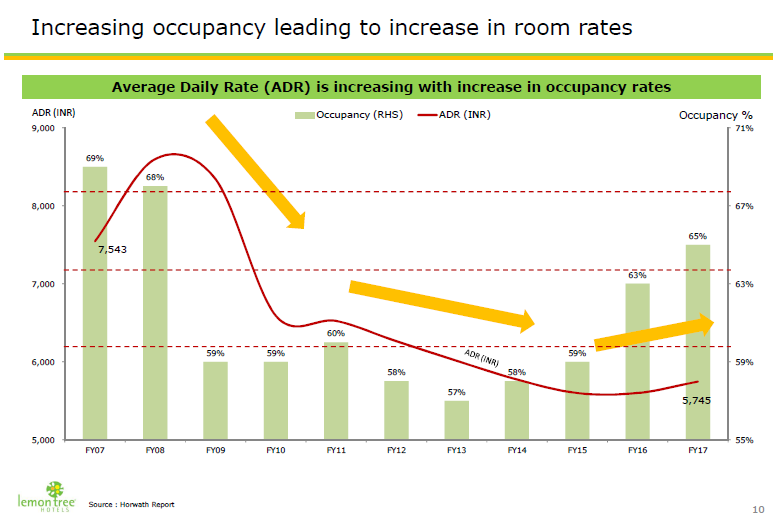

Hotels is a cyclic business. ARR’s and Occupancies were depressed since 2008 as increase in supply was at a faster pace than increase in demand. Now that scenario is changing.

This is corroborate by Horwath HTL in their report “Industry Report – Mid Priced Hotel

Sector” dated September 9, 2017. They are world’s largest and most successful hotel consulting company.

Any new supply takes atleast 3-4 years to come online and hence with increasing demand and limited supply, ARR’s and occupancies have been rising and are likely to rise further. This trend is observed across industry.

It can have pricing power if majority of its customers are from business segment rather than leisure.

Lemon Tree is predominantly a business hotel.

1/3rd of their revenue comes from large corporate tie-ups. They enter into annual contracts and price revision happens annually. Company does not have much pricing power when it comes to large corporate account.

Another one-third is from MSME. MSME’s has very limited pricing power as they will buy rooms in 2-3 hotels. 50% has annual contracts and 50% book directly through call center or website.

Others book either directly through call center or company’s website or through OTA. Typically the ratio is 27% online [20% OTA + 7% direct website bookings] and 7% in-house call center.

However, they adjust the inventory based on demand and obviously a customer booking directly either through call center / company’s website offers better realisation. Management expects that due to this demand-supply mismatch, there will be significant price revisions with corporate accounts as well.

One of the points left out is efficient and tidy worthy CEO who has served with Indian hotels and in a short span of time mage lemon tree such a big brand

Room inventory:

No new rooms are being constructed by any hotel chains except Lemon Tree. If any major player wants to enter / expand in india then they will acquire inventory from an existing player. e.g. If Hilton wants to add rooms then they may acquire it from either a Marriott or an equivalent player. New supply pipeline over next 5 years is approx. 8.5% p.a. whereas demand is expected to grow at more than 12.5% p.a. Given this supply-demand imbalance, management is very bullish for next 3-5 years. Company that has many assets in say Mumbai or Delhi will benefit more than a company that is more diversified.

Price hikes:

In India there is a misalignment of incentives. An operator or manager of hotel is incentivized on revenue and on profits. Unfortunately, an owner is only incentivized on profits. So, this misalignment of incentive is leading to some level of underpricing. Owners of hotels who manage hotels will be more aggressive in taking prices up, but guys who are pure managers of hotel like the international brands unfortunately are not taking prices up and that is the sad part of what is happening in India because we are not aligned in incentives.

Change in ARR mix:

Company is adding 800 new rooms (~25% of existing inventory) in next 1 year in markets where average rate is 1.5x of normal ARR as these are all Lemon Tree Premier (ARR Rs.4000-5000). Mumbai international airport hotel will add another 670 rooms in next 2 years where ARR could be 2x normal ARR.

There is massive mix change that is going to happen which coupled with normal price hikes of 9-10% should result in more than ~14% hike in ARR over next 4 years.

Delay in opening of Udaipur and other managed hotels:

It was to be launched in April which is a down season due to summers and company tool an internal decision to delay it to open in October. They are also upgrading the hotel with a smaller investment to get better return on the entire hotel.

Managed hotels has negligible impact on lost fees.

Competition from Taj Ginger:

Ginger is an economy product which competes with Grey Fox and hence not material competition. The formulation of Ginger and of that market will ultimately help the entire market.

OTA:

OTA’s usually charge between 15-18% commission. Lot of retail customers come through OTA’s and company tries to convert them to their website once they stay with them through loyalty programs. OTA’s are presently offering cashback which is difficult to compete with and company does not offer any cashback but offers other facilities like free breakfast, free Wi-fi etc.

Lemon tree has announced a JV with an affiliate of Warburg Pincus group to enter into student housing, co-living for working professionals/adults.

JV company (Hamstcde Living Private Limited) will construct, acquire, develop, operate and lease short and long stay real estate projects.

Shareholding will be as follows:

Lemon Tree - 30%

Magnolia (Warburg Pincus) - 68%

Mr. Patanjali Keswani - 2%

The JV partners will initially invest Rs.1,500 Crore in equity over a period of time followed by an additional infusion of Rs.1,500 Crore in equity at the option of the partners.

The main purpose of the JV is to develop rental housing projects through a combination of greenfield purpose-built properties, refurbishment of existing under managed/stressed commercial and residential assets taken on lease/acquisition basis as well as management of existing for rent accommodation projects.

Student housing / co-living for working professionals could be a big opportunity but 30% stake will require equity infusion of Rs.450 Cr. into JV from Lemon Tree. The company does not have any excess cash and debt is presently at around Rs.1000 Cr. which is expected to peak to Rs.1,300 cr. for construction of ongoing hotels. This additional 450 Cr. will put further burden on the company. It will be interesting to see how the company will manage it’s cash flows. We may see announcements for monetisation of some of the hotels sooner than expected (like they did with APG in the past).

Promoter Group has been continuously buying and this announcement could be one of the thought process behind it.

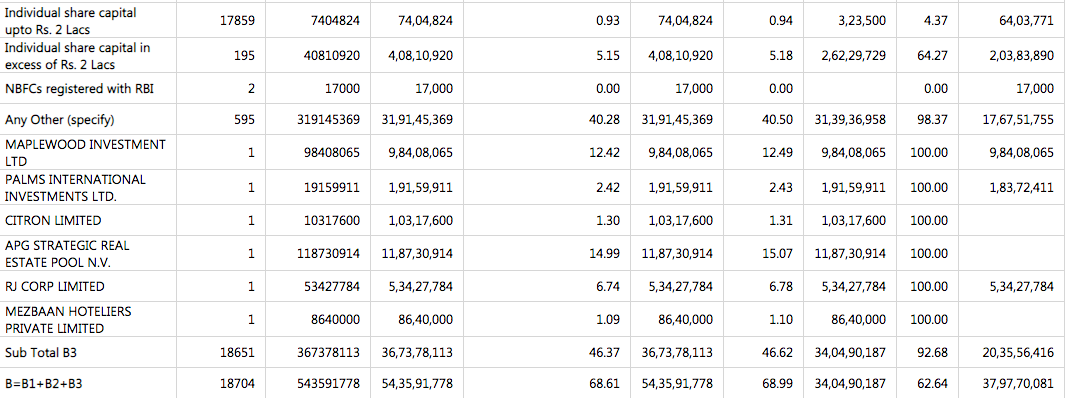

62.64% of shares are locked-in as per IPO norms. ~29% of this (12.5% of total share capital) is held by MAPLEWOOD which made partial exit in IPO. Approx. 5% of total share capital which is locked-in is held by individuals (in excess of Rs. 2 Lacs). These should be released somewhere in 2019 around the time when debt has also peaked out and balance sheet will look stretched. We may see some selling pressure around this time.

Posting some relevant articles to better understand management and industry.

Why hotel chains are unable to increase room rates in spite of robust demand.

Interview of Path Keswani giving insights into his early days at Taj, how Lemon Tree started and the policy of the company to not engage into any kind of corruption, and values on which Lemon Tree is built and operated.

Considering the opportunities and constraints present at ground level, Mr. Patu seems making all the right strategic and operational moves in terms of increasing market share, preserving the brand, bringing in geographical diversification to tide cyclicity etc. Can I request senior members of this forum to provide their insights on what could be the sustainable growth rate and right valuation? Thanks

The promoter holding is just 31.76% out of which 33% is pledged. Patu Keswani has also hinted that if extended Moratorium is not provided then Hotel industry can lose 25% of the room space.

The debt/equity ratio is also 1.41 yet the stock has been gaining in the last one week.

While I am invested and optimistic about it’s future though Debt and pledge on the book is making me jittery on this stock. Any views?

Quite an interesting management interaction earlier today with Nirmal Bang (link)

Total rooms in India ~ 160’000 (by branded players; about 1-2 mn unbranded) as on Feb 2020; Occupancy was 120’000 (~75%) in Feb 2020

Have dropped prices to stimulate demand

Caters to mid-market;

Business breakup (by last year):

o 40% was retail (online + direct + phone call booking); 80-90% (i.e. ~35%) has come back albeit at lower prices. Seeing upgrade from 1st timers (i.e. upgrading from guest houses which oyo serves)

o 15% was foreigners (no recovery until now)

o 5% was meetings + incentives (no recovery until now)

o 15% was leisure travel (about 66% is back i.e. ~10%)

o Balance 25-30% was large corporates (no recovery until now); expect 20% of corporate bookings to reduce due to remote meetings reducing overall demand by ~6% (20%*30%)

80-85% of hotel owners are individual (with incentives such as converting cash to assets + other non-financial based incentives); Expect some level of consolidation through institutional ownership should happen going forward (not a lot though)

Looking to create a 700-800 cr. fund to buy distressed hotels

LTH enjoys ~12% market share in mid-market segment: With ~15 years of operation, LT is already a leading mid-market player (category creator) with ~12% market share as of FY19.

LTH currently operate about 8,006 rooms (5,192 owned/leased and 2,814 in management contracts) in India as of 30th June, 2020, with ~14% share of the mid-market (2-star to 4-star) which is about ~56k rooms. Mid-market is ~40% of the ~140k branded rooms. …. market share to expand to ~20% by FY23E: LTH market share is expected to expand to ~20% by FY23 end as it commences the largest hotel in India with 669 rooms (including conversion of commercial space into residential) in the busiest location of Mumbai. We have estimated the Mumbai property to contribute from FY24 only. LTH is one of the fastest growing companies. With strong pipeline, LT’s market share will expand to ~20% by FY23E. Room inventory to grow at ~14% CAGR. LTH is the largest chain in the mid-price segment: LTH is the largest hotel chain in mid-priced hotel sector in India on the basis of controlling interest in owned and leased rooms. LT’s positioning in mid-market segment in demand-dense CBDs in Rs 3-5k ARR bracket make it well-poised to benefit from the demand recovery in a post pandemic world

Pledging of shares is potential risk and moratorium by government is absolutely critical for maintaining hotel industry

Source Credit Rating reports (Dolat Capital) and Economic times

Disclaimer - I own very small stock quantity

Strong tailwinds in this sector - seems a cyclical uptrend.

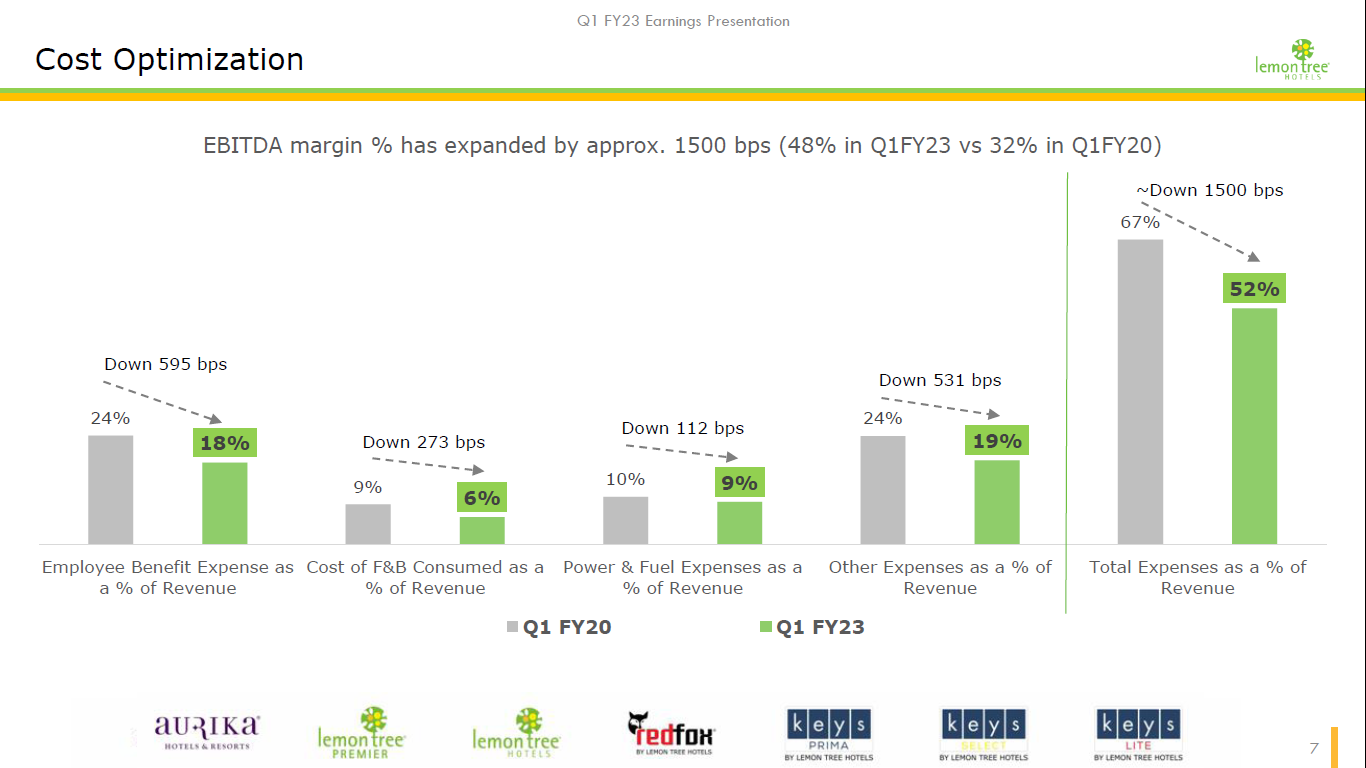

Lemon tree is well positioned across its various brands catering to diverse demographic. LemonTreeHotelsLtd q1fy23.pdf (5.6 MB)

Promoter holding is just 23.9 %, of which more than half is pledged. And 2/3rd of the revenues coming from a couple of dozen subsidiaries & associates which the auditors claim “…we did not audit…”, how does one address governance concerns? Doesn’t look like a stock meant for retail investors. Or am I missing something?

This stock can be a bet on Mr. Patu Kesvani’s business acumen and capital allocation/management skills, sectoral tailwinds and Lemon Tree’s positioning among the peers since it would take few more quarters for the numbers to reflect the same. One should go through the details of concall and investor presentations since 2019 to get an apple to apple comparison of the performance and to see how he has been able to tide the Corona pandemic in a very elegant way (maintained positive EBITDA margin in all quarters when others have struggled) given the fact that the tourism/hospitality industry was the most affected with no support from government and the banks.

Lemon tree seems to hold a controlling stake with 100% in almost all its subsidiaries. There seems some changes happening in the corporate structure as well.

The D/E of 2.56 as per screener is high. Majority of the borrowings are long term with assets and equity shares held as collateral with leading banks of the likes of HDFC bank/Kotak etc. Details are available under notes section in AR 2020-21.

While promoter stake is low, many FIIs/DIIs of the likes of Goldman Sachs/JP Morgan have entered in the recent quarters.

On a lighter note, think yourself to be a HNI (why retail?)

Lemon Tree Hotels --CNBC Interview with MD–10th Oct22 :

Q1 & Q2 are somewhat similar , they a/c for generally 40/45% of total income

–Q3/Q4 --normally its 10/15% price hike and 10/15% Occupancy hike --so if you add the two it will be 1.2/1.4times the H1 income with the expenses remaining the same. hence most profits come in H2.

–Q2 additions --we opened 4 hotels , we have 1/2 inquiries every-day to take over the mgmt of hotels.

–We will cross net additions of more than 1000+ rooms this year and we will cross in total 11000 rooms by the end of next year.

–In 4 yrs we will cross 21k/22k rooms.

–Big one in Mumbai ( Aureka) --it will do around 300/350Cr revenue & it will have a net operating profit of 175Crs probably 200Cr, it will do north of 12k average room rent. Mumbai is like NYC , every-year there is steady growth in Demand.

–Business hotels --85% of our inventory is business hotels , those traditionally do badly during diwali/dushera --so oct’22 will be low demand for business hotels but in Nov’22 it changes completely, in Nov you will do 1.5/2 times your oct revenues. But the average H2 will be 25/35% hike in revenues.