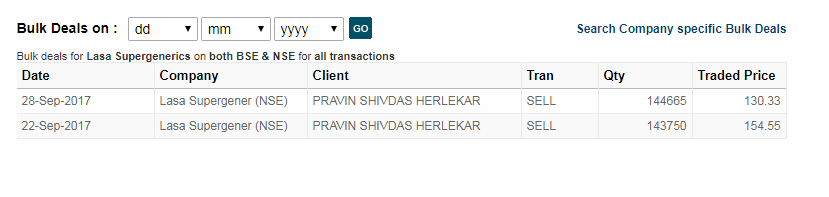

Pravin herlekar sold shares on 22 September

http://www.moneycontrol.com/stocks/company_info/blockdeals_query.php?sc_id=LS06&post_flg=1&myexchg=Both#LS06

Interestingly there is no disclosure yet to the exchanges about this sale in Lasa but both the father and son have made disclosures about their pledge and sale respectively in OSCL made on the same date (21-22nd Sept).

On 22nd Sept, Pravin Harlekar has sold 1.44 lakh shares of Lasa at a avg. price of 154.55, very close to the 52 wk high of 156! (Current price is 132) On this day, the total volume was 2.95 lakhs. Clearly the demerger and value-unlocking has benefitted the promoters more than the minority shareholders here wondering why the scrip is in lower circuit for third consecutive day today.

These demerger value-unlocking plays seem to be pure gambles because if everyone is looking for the value-unlocking, its going to be a mad rush to unlock value in the short-term at least, leading to very few capitalising and the rest trapped at higher prices. These invariably settle at pre-demerger valuations once the dust settles. In the long run however, if one or both the demerged entities does well, they may undergo re-rating that they deserve but in the short-term it seems to be driven by irrationality more than anything.

7 Likes

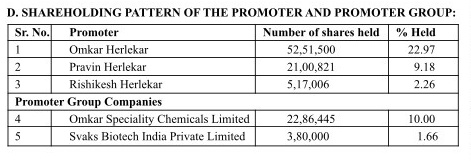

Mr. Omkar Herlekar has clearly said that while he does not keep his sake in Omkar, he will increase his personal holding in LASA to 40 %. Let us wait and see , ow they manage the mutual share swaps between Lasa and Omkar promoters to achieve their objectives. The rerating triggers for LASA will be debt reduction, promoters stake mgmt and startup of unit 5. Let us wait and see.

1 Like

thank you.

the demerged entiry again is a holding company with part ownership to 1 listed and two unlisted financial companies.

Most likely because Pravin Herlekar is not categorised as a promoter in Lasa.

Could someone clarify what is the total debt on lasa and omkar separately. Screenr shows debt to equity of more than 2

Hi @sta

LASA has total of around 120 Cr (60 Cr is promoter provided and 60 Cr is external)

OSCL is around 220 Cr (60 Cr promoter provided and 160 Cr is external)

1 Like

Hi @nkgambhir All of this will take 2 years to play out. Generally, if it works out that is what might happen in the business as far as sales etc. Don’t know about stock price.

1 Like

True. No one can predict the stock price. But if the company grows and performs as expected and if the irritants like excessive debt, low promoters stake , pledged shares etc are taken care of , then it should be valued like other veterinary API companies are valued by the market.

All veterinary api companies could also be devalued to a PE of 5. It goes both ways. Sorry to be direct but please be a little more careful of statements and stock price predictions on the forum and to yourself. Go slow with your posts and request you to please contribute only when you have something constructive apart from price predictions or generic statements which are repeats.

13 Likes

Pravin Herlekar is busy cashing Lasa Shares. What is he trying to tell the minority share holders?.

Also there is a disclosure on selling of shares on the 26th.

On another note, Omkar Herlekar claims in the interview that he is the sole promoter and he will get his shares up to 40 % (without including the holding of OSCL).

I tried math, but even with inter-se transfer at the current holding, Omkar wont be able to make it to 40 % - more difficult with Pappa Herlekar selling it continually.

Would thank @phreakv6 for shaking me out of anchoring bias and look for the unfolding of events more objectively.

“Hopefully”, this is just teething problem, and will finally even out.

1 Like

Father is selling Son’s company shares and Son is selling father’s company shares. In midst of all this we are getting both the stock at good valuations for fresh entry. Why are we complaining?

4 Likes

Not sure if your comments are after fully understanding and analyzing the points raised in the earlier postings by @phreakv6 - which no one answered yet.

First of all, father and son agree to split the company for unlocking the value. Then they sell their shares in the other company and cash the money. Who pays for it? Those who feel that they are getting the 2 companies at good valuations.

If I put the 2 entities together again ( as the story is intertwined yet)

- Unit V is yet to commence operations. All we hear is Soon - How soon is “soon”.

- We still dont know how is OSCL debt issue gonna be resolved.

- No details on rights.

- Share holding in the entities is not clear in black and white ( while talking interse transfer- there is concurrent sale of shares).

If it is the case of good valuations at the current price for fresh entry, why would the promoters sell ( they should be holding it as family silver)?. I could see 2 reasons:

- They want to raise fund for their respective companies by selling the cross holding(who is paying - the minority holders)

- They could be selling to make hard cash for themselves (laughing at those buying at this price).

I am playing a devil’s advocate here and would be glad to be wrong.

Please counter these points.

Discl: Invested in both entities.

7 Likes

Points raised by @phreakv6 are not related to financial performance of the company.

My point is related to value of the company. Is the company undervalued? In my opinion it is.

Lasa is a (soon to be) debt free company, trading at 11 PE, expected to grow at 20-25% for next 3 years. Operating at 40% capacity. With industry size of 4500 crs.

Key risk remains selling off of 10% stake in Lasa by OSCL or inter se transfer of shareholding between Father and Son not materialising which can result in depressed stock price for short to medium term.

It is pointless to guess what promoters will do with their respective shareholding. We have the choice to believe Son will raise his stake upto 40% through various means. Son could have easily issued preferential shares to raise his stake and retire debt, but then we minority shareholders would frown upon that too.

5 Likes

If their aim is to enrich themselves at the cost of minority shareholders, they would have taken much higher salaries and would have charged a lot of interest on the debt they gave to OSCL. They could also have converted their debt into equity to increase their holding without giving any chance to minority shareholders.

This is a serious fundamental issue and needs to be watched carefully. Unit V has taken almost 2 extra years to commence operations. Investors need to physically go there to see its progress.

6 Likes

Atleast now we can safely assume that there will be no selling pressure on Omkar Speciality , since Omkar is done with selling his stake in the company. However, this may continue in Lasa until Praveen is done with selling entire or most of his personal stake.

From where did you get the bulk deals data. I checked on BSE but it did not give any such data.

and

The questions are correct. What is causing the change and what is the benefit to LASA? But is there a more important question? What is the benefit to me? The student investor? And then also to me, the guy who has put his money at risk.

First. This story is not a story for accountancy investing ![]() please bear with me till you read the post.

please bear with me till you read the post.

This is a story of special situation(s) plus turnaround, and has no basis in mathematics alone. This is a classic case of investing is art + science. More art. Not that I have the art, but this was the best opportunity I could find to learn as much as I could about the art side of investing and I jumped in.

The investing in this story is not about steady compounding etc so it is not suitable for everyone as not everyone can take time from their schedules to follow all the moving pieces and there are many moving pieces in this story. Usually, there are picked up one by one on the forum, it makes no sense to pick each moving part unless the whole picture is followed and mostly understood. There are much better candidates for vanilla investing. Why I liked this one is that it has the most to teach for further investing as it covers so many angles of investing.

I will point them out.

- OSCL - Debt (Then you have to study, why did OSCL get caught up with so much debt (will make us study debt situations)

- OSCL - LASA Demerger (Then, why the de-merger and how do the de-merger stories play out, we learn about de-mergers)

- OSCL - Turnaround (Will it happen, how will it happen, what all can one expect if it does happen, we learn about turnarounds)

- OSCL - Rights Issue - We learn about rights and propotional equity dilution, re-calculating EPS, rights issue pricing etc.

- LASA - Growth (We learn about growth investing)

- OSCL (Speciality Chem) LASA (VET API) - (Follow separate industries and markets and learn about potential of each)

- Patience - In the light of so much evidence, data and noise to the contrary, this much noise does not happen with most companies, how do you keep your conviction? (One trait needed to learn to be able to hold on to this story).

This at-least to me was a case of patient learning. Of course, price is everything and I don’t want to pay a tuition fee in money and happy to pay it in time, so entry prices were of utmost importance. Thus also - learn Value Based Investing.

Throw in some family drama (brothers splitting up, father selling shares in son’s company and son selling shares in fathers company)

Also some serious pledging and de-pledging.

We threw in something new, and went to the final frontier; we also met the management of both companies. So doing management meets.

The learning has been immense.

I think, OSCL + LASA were the best teacher over the last year and one must love these stories if one wants to really learn investing. They expose every danger and also every reward of the investing business.

If one is going to invest over the long term, it seemed to me it is crucial to study stories like this, money is mostly always around to be made in the markets.

Now to the answers you wanted;

Why the de-merger, it is a scam by the promoters to get rid of debt?

The de-merger is to the best of our knowledge because of the two sons not getting along. It is not because of promoters taking investors for a ride.

This is best captured in the answer from @Akhil_7306. Really, closes the issue without argument. We all know very well, what listed company managements who want to take shareholders for a ride do. These guys have not done that.

Now, on the selling pointed out by the promoters, the selling was done by Pravin Herlekar. He is not the promoter in LASA. He is a shareholder like you and me. Why is he selling his shares. Well, there is about to be a rights issue in OSCL. Does it make any sense for the promoter of OSCL to have shares in LASA but have low and partly pledged shareholding in his own company? If it were me, I would do the same. I think he is selling LASA shares to collect and further subscribe to the rights issue of OSCL so he can increase his shareholding in the company in which he (Pravin) is the promoter, which is OSCL. If this is the case, it will become evident soon. We would all like to see Pravin arrange funds and increase his shareholding in OSCL actually.

One of the questions was the increased market-cap. Do we know who decides the listing price for the de-merged entity? It is not decided by the promoters. There is a price discovery process. So, why are we blaming them for manipulation?

Even after listing, the fluctuations are so much that the promoters don’t have the cash to manipulate stock prices in most companies.

Now, why did LASA give 10% shares to OSCL. Well, again, no manipulation. OSCL funded the unit 5 that LASA has received. So why will LASA not have to pay OSCL? They will have to compensate them. Does that not make sense?

Now, start of unit 5.

Yes, a very valid question. Personally, as mentioned, I think it will start soon. Now more specific, personally, if the Unit 5 does not start by end of october, I might exit LASA because there is now no reason as to why Unit-5 is not starting. I could understand till now that even if it unit might be ready to begin operations, they were just listing and might not have had the time to put the efforts in parallel starting a complex unit.

Best Regards.

Criticisms and Questions welcome.

35 Likes

If you are just relying on Dr Omkar’s interview to come up with the above and then using this as justification to be invested, then best of luck. The promoters have time and again promised many things and not executed on them so take his interview with a bagful of salt.

disc - invested in Lasa from demerger of OSCL, had exited OSCL some time back

1 Like

I have also read management transcripts where they have guided turnover of 500 Crs. in next 2-3 years.

Having said that, I don’t believe much in management projections, unless the management is conservative. In this case it is not.

But key thesis is that Lasa is one the low cost backward intergrated domestic API manufacturer and is also trading at discount when compared to peers. Management has shown good leadership in scaling this business from scratch in the past few years and therefore I am reasonably satisfied with their execution skills.

After the write off of Assets and taking a hit on P/L, Balance Sheet looks a lot leaner and therefore going forward we can see improved return ratios like ROE and Asset Turnover.

Overall I feel downside is low, unless Management risk is triggered.

4 Likes