Answers are below. But first, they are opinions and may be right or wrong.

Ethics: I believe they are ethical people. I have seen ethical people get into problems and unethical people get into problems. It is the approach that one uses to come out of problems that determines their future (next 30-40 years professional and personal career and where they spend their time, with friends and family or in courts) both the Herlekar’s seem to value their quality of life and to my opinion will not risk it for some extra money. They have answered their personal values question with selling their holding but not doing anything major wrong. The shareholders have been rewarded for keeping faith in OSCL + LASA with the de-merger.

Aggressive: Yes, Omkar is aggressive, and I liked it. I don’t want a patsy running my company, neither do I want a patsy running a business I invest in. He is a very decent person though.

Omkar Herlekar is a professional and professionally respected guy, and is very focused on the business.

Omkar seems to have very well understood the real cost of debt. We know, their family lost nearly half their shareholding in a listed company. Now that it has been said publicly by them, I can also mention that Omkar also said in the meeting as well that, he will wipe out LASA’s debt very soon. That is the magic sauce; they have always been growing, Omkar Herlekar does not want any debt in LASA. Growth + No Debt = I like it. They are going to succeed.

On a philosophical note; I see this many times, when one has no or little money, they still find a way to make things happen, but when they have money, they don’t think and use money as a solution. Then they don’t have a solution and no money either. Then they think. This is what happened at OSCL. Omkar does not want a repeat at LASA according to me; he is going to think his way to growth and not borrow from banks is my feeling.

So the triggers to watch in LASA for me are;

Debt Removal

Sales Growth

Profit Growth

Start of Unit 5

If anyone reading want’s a further hint, they seem to have a clear path and infrastructure to about 450-500 crore in sales and by then we will be able to see what Omkar does next for further growth.

I will also post a report for LASA in some time based on Peter Lynch’s identification system for a growth company, let’s see how LASA stacks up

On your OSCL question, I will post my answer on the OSCL board.

Bring ambitious is good ,and caring for the stock price means he cares for the Lasa investors also. In my interactions with him on social media, I found him to be a very decent, down to earth person , and I hope LASA continues to grow as fast as it has been growing till now.In his CNBC interview he has categorically stated that they will sell only those products with an EBITDA margin of 25 % or more and also expressed confidence that LASA sales will continue to grow@ 25% , for many more years.

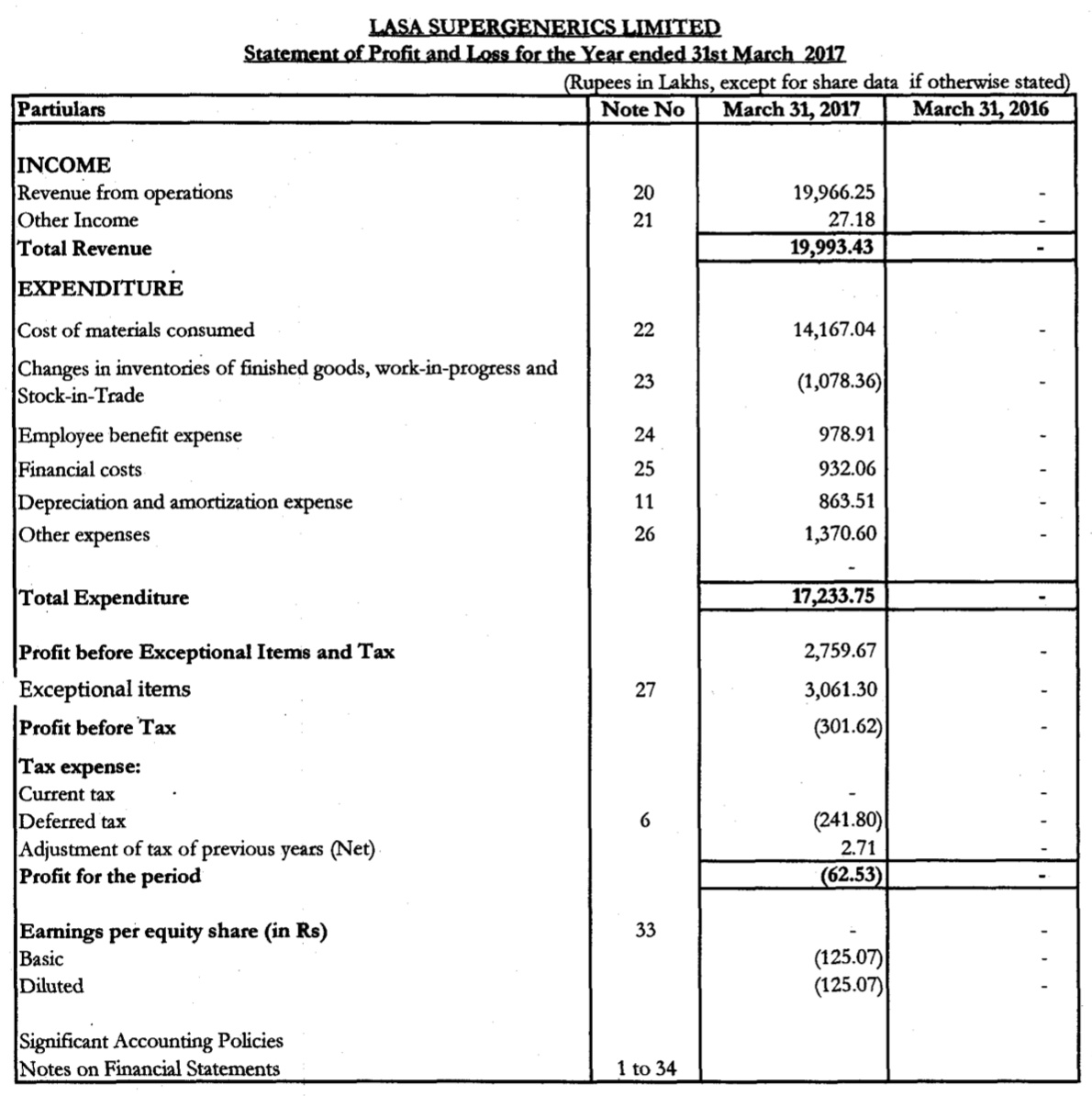

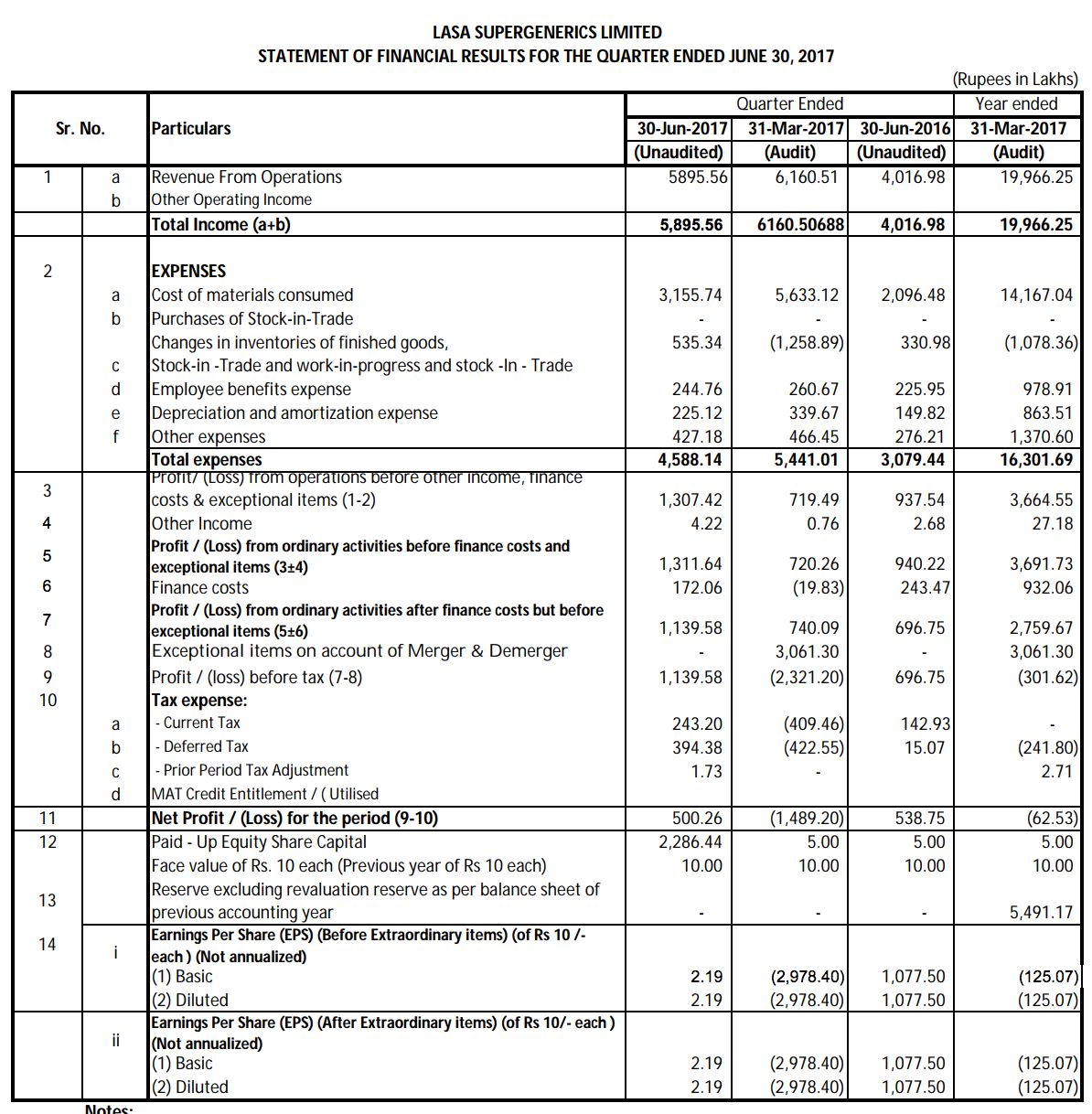

Something doesn’t add up with the numbers for FY17 in the sheet vs what I see on screener. PBT and PAT are negative. Is there an official source for the numbers so that we can verify which of them are correct? Interestingly Sales numbers are almost same in both.

The PAT number reported by the company (I see that its audited as well) is -62.53 lakhs so it looks like the numbers in Screener are correct. The screenshot in your post has a PAT of 30 Crores and an adjusted PAT of 18.5 Crores. Where are these numbers coming from?

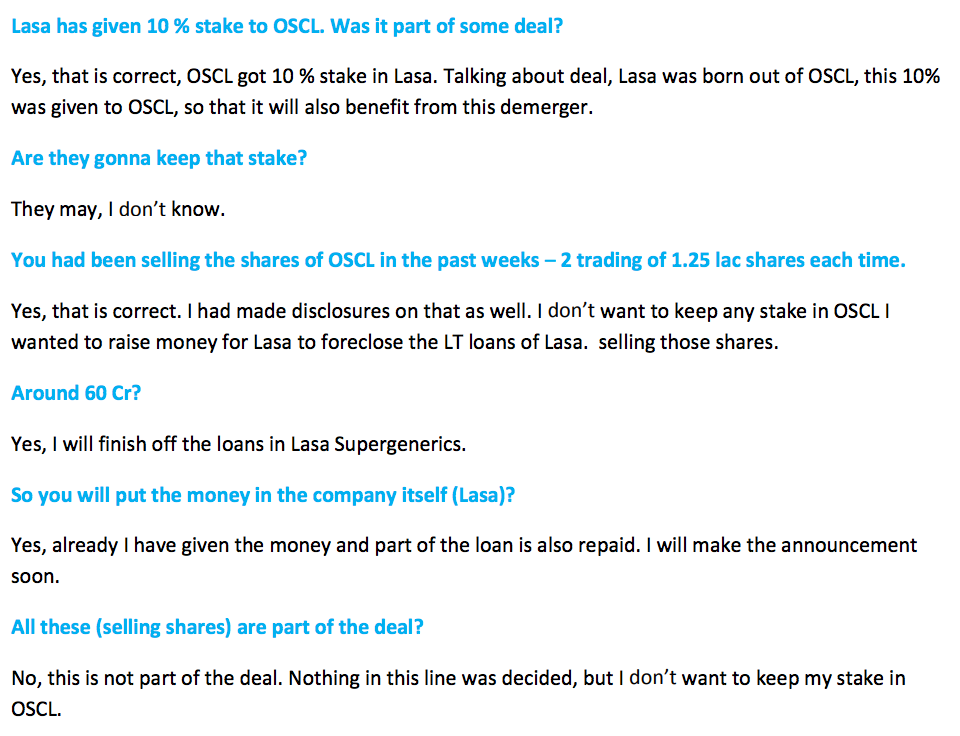

So the company is claiming to have made 30 Crores PAT in FY17 but has written it off probably because that’s a payment it made to its parent. I see long-term debt in OSCL was 220 Crores as of March 2017. Lasa’s Borrowings seem to be at 120 Crores. So if they took out 120/220 Crore of debt and also made a payment of 30 Crores by way of exceptional one-time demerger settlement, was this really beneficial to Lasa?

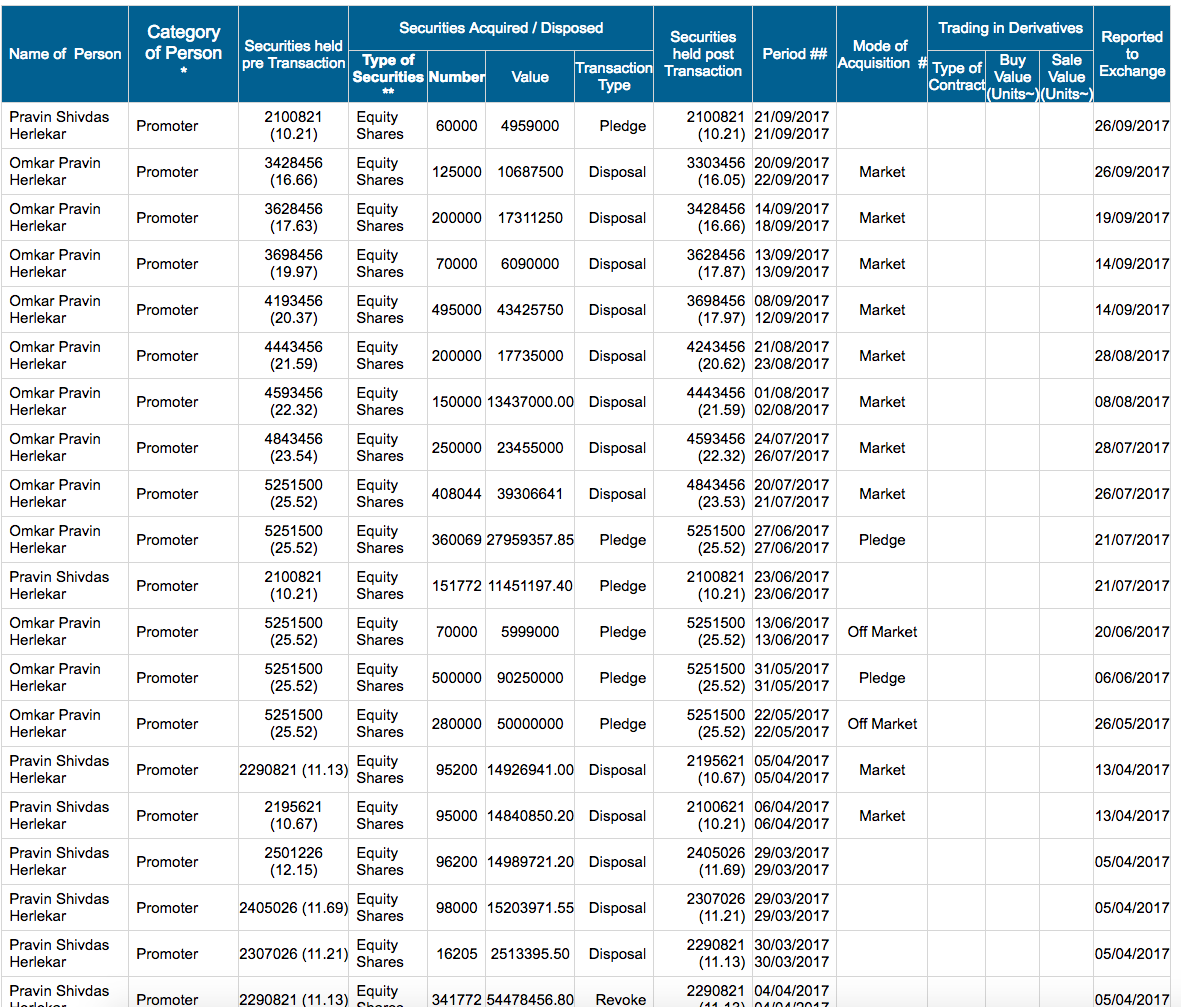

As someone who is not invested here and as a layman, I see it this way. Market cap of OSCL before demerger - Around 350 Crores. Market cap of OSCL post demerger - 160 Crores. Market cap of Lasa Supergenerics - 330 Crores. I understand the fancy “value unlocking” and all that, but one entity which was valued at 350 Crores suddenly became valued at 490 Crores, and all the while the promoter continues selling.

If it is being justified as part of the demerger agreement, just think if you would be OK if the promoter sold stake before demerger when it was one entity. What has changed materially?

To me it sounds too complicated to understand, so I will have to pass this and probably lot of current investors with Lasa shares see it the same way (that it is overvalued) and so are selling?

The immediate triggers would be debt reduction and Startup of Unit 5. Both these events would be solid triggers leading to almost a 100% increase in earnings.

In the beginning there is one company with 220 Crore debt and a 350 Crore market cap which becomes 490 crore market cap post demerger and debt is reducing too - How? Because promoter from one entity is selling his shares in the other entity at these elevated valuations. The same may happen to Lasa too where the father/OSCL sells Lasa stake to repay LT debt of OSCL. Maybe this is why the scrip is in lower circuit? See this.

Isn’t this a bit murky? So where is the money coming from the reduce the debt? From the shareholders of course! They are the ones holding the bag as the promoter offloads at higher valuations. I am also a bit confused how the promoter will use his personal money from his stake sale to reduce LT debt of his company. Is he going to loan the money back to the company? Similar thing happened in Ujaas energy where the promoter sold stake at Rs.40 (7% of the company) and wanted to loan the company the money (which was shot down in the voting by shareholders). This looks to be sort of similar with a bit more smoke and mirrors.

Considering OSCL share price was around Rs.160 in May. Think what would have happened if the promoter offloaded his stake without the demerger and tried repaying the debt of OSCL. Now the share price is at 80 + 140 = 220 (Can compare directly since this is a 1:1 demerger). So this is the equivalent of pumping the price up to 220 and then selling stake and saying you will use it for repaying loans. Would have been very frowned upon if it was done that way.

the stock was trading at close to 250 (before demerger) till the WC / Debt crisis happens. As the crisis is getting solved, so the equity mkt increase will be much higher. the company performance has not deteriorated over the past two years, actually improved a lot (assuming BS numbers are genuine, as of now nothing to prove they are fake)

Secondly look at any demerger in last 6-9 months, all have led to sum of parts increasing by 30% so that way it is not an exception (sintex, grasim, cholamandalam to name a few)

valuation: look at any parameter, it is one of the most cheaply valued stake in chemical / pharma industry

Pravin Herlekar ( promoter of OSCL ) has in the past sold his shares and given interest free loan to OSCL to repay some part of its debts. In previous concalls you can find the details.

Its a valid argument. However, the only business driver for this demerger is that the 2 units of legacy OSCL (LASA & OSCL) are essentially 2 different business and should be valued differently. As OSCL was better known and listed, market was valuing OSCL as a pure chemical play with lower P/E. This was not entirely true as LASA as veterinary API deserves higher valuation - which is what has been visible in the market. What we need to investigate and track is the future performance of LASA and the LT debt reduction (i.e. whether management is putting money where the mouth is

Given the past track record, management does seem to be inconsistent - which is acting as dampner for the stock

Secondly look at any demerger in last 6-9 months, all have led to sum of parts increasing by 30% so that way it is not an exception (sintex, grasim, cholamandalam to name a few)

Hi,

which demerger of cholamandalam you are referring to? kindly clarify.