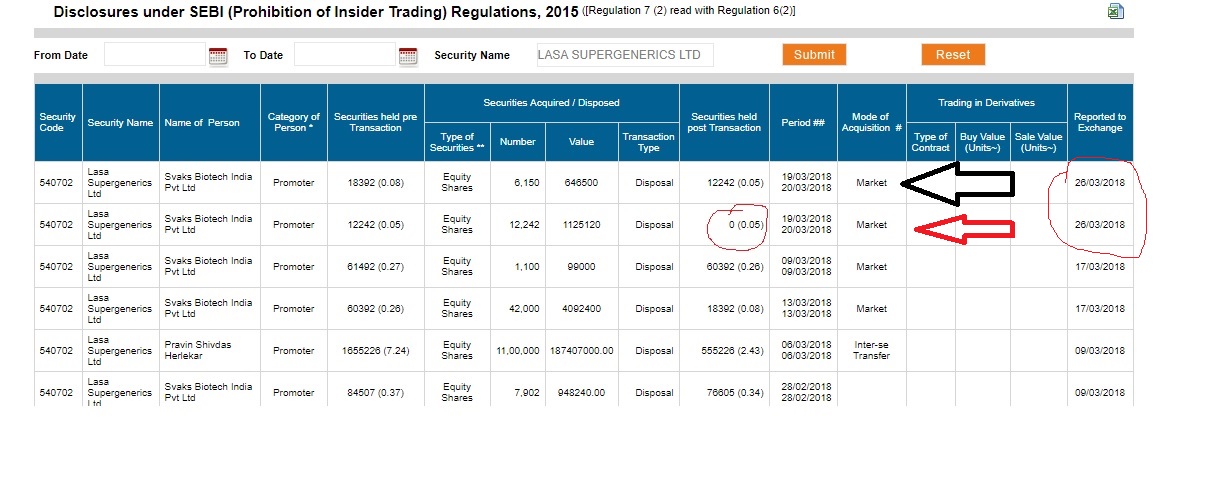

I thought Svaks belongs to father, Dr Pravin. He is not a promoter of Lasa anymore. Why should his selling be treated as promoter selling?

2 Likes

Omkar bought from his father…interse transferhttps://www.bseindia.com/corporates/anndet_new.aspx?newsid=b15b2588-0ec0-4c7c-9848-9bd87d578683

I love your excellent scuttlebutt and the details provided in the thread.

Omkar has been keeping his word regarding the interse-transfer of stake from his father. That is a positive. Business fundamentals so far look decent to me. Still trying to understand the depreciation and R&D capitalization methodology they use in the results though

What is your view regarding the CFO resignation and the change in auditor? Also, what would be the logic for announcing joint audit with the addition of one more auditor recently?

Your views would be highly appreciated. Thanks.

Disc: Invested.

Sir, what CFO?

Did you ever hear about this CFO before this resignation? Did any investor ever meet that guy? Did that CFO attend any concall?

As per my understanding, he was a simple employee of the company in the accounts section. And his name was given as the CFO for official reasons when the demerger happened.

When he resigned, the exchanges had to be informed, as per the rules.

Mind you, Lasa is a 5 year old company and that too, a small one for the first 3 years. A company with less than a few crore annual profits cannot afford to hire a multi-crore package CFO. Good CFOs do not come cheap.

Having said this, please don’t expect me to know things happening inside the company. I am also an investor, trying to connect the dots.

If everything were absolutely clear, Lasa won’t trade at these valuations. So depending on your view on the uncertainty, this is either a buying opportunity or a clear touch-me-not.

Am studying this joint auditor thing. So I don’t have any view on that right now.

My personal view of the company is positive. Added a few thousand more Lasa to my old holdings today at LC. But I am willing to go wrong with my call and lose my money. So bet only what you can sleep comfortably with.

Madhur Kotharay

12 Likes

I am not able to see latest comments

Hi all,

Would like to highlight one key aspect - Quality of Employees and Top Management. I was going through the top management profile and it seems to be quite mediocre and below average (except for MR. OMKAR P. HERLEKAR) Link - http://www.lasalabs.com/board_of_directors.html

Furthermore, it seems that company does not invest much into the quality of employees On a run rate basis, the annual employee cost is around 10 crores on a revenue of 240 crores which is meagre 4% of total revenue. I do take into consideration of the small turnover but you need some technical people to run the API business. Employee quality seems to be one challenge i guess.

@nkgambhir - What exactly did you find informative in the video? It looks like a spam message with someone recommending a buy and carries nothing worthwhile deserving a place in this forum IMHO.

17 Likes

Well just because employee cost is less doesnt mean that they are below average or mediocre. They are the one who are responsible for raising the turnover from 1Cr to 200 Cr, from one product to 15 products. What matters is the understanding of business and process which I think they should have given their experience.

As far as i think this downfall can be attributed to:

- Confusion about promoter holding (father selling continously in Lasa)

- Omkar Speciality promoter history hovering on Lasa (However father Son set apart after demerger but Son has to prove his (Lasa) potential)

(Omkar promoters never kept on their words in past) - CFO resign, No experience person in Board of Directors

- Auditors resigned (managment not clarified on this, it can be symptoms of poor corporate governance) And after that they hired two Auditors one after one. (Need for 2 Auditors, no words from mgmt side)

Management calrified many times about shareholding but still a confusion is there…

Disclosure: Hold tracking position, focus on quarterly results

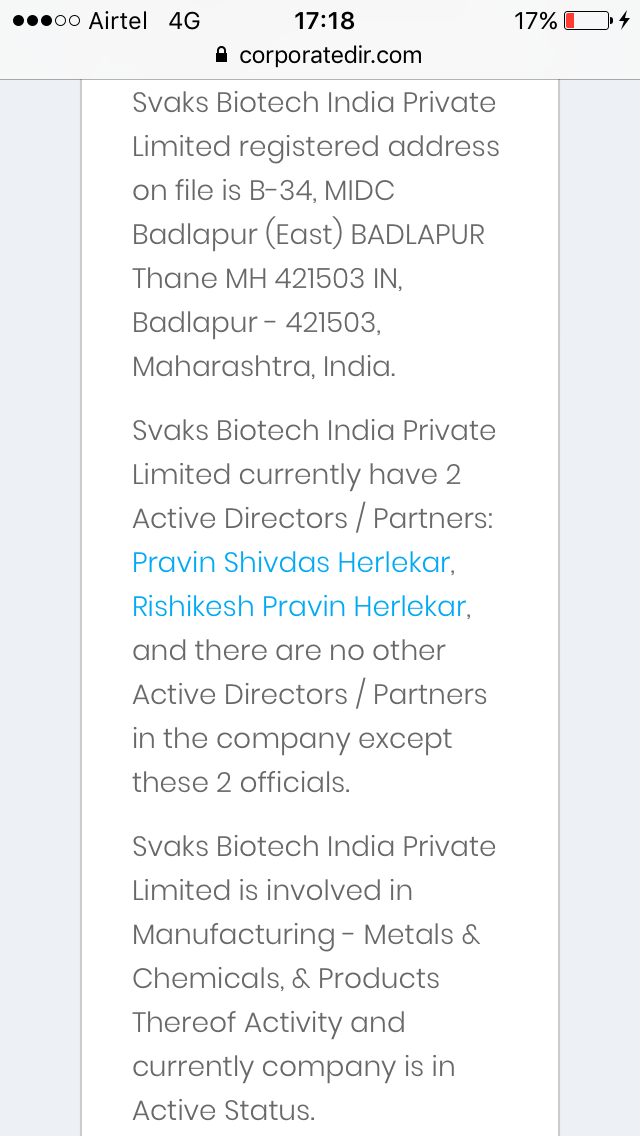

Svaks Biotech India Pvt Ltd has completely sold off there holdings as per the BSE data

4 Likes

Hey thanks for the info for the insider news of promoter selling. Yes Svaks Biotech India Pvt Ltd has completely sold off there holdings.

1 Like

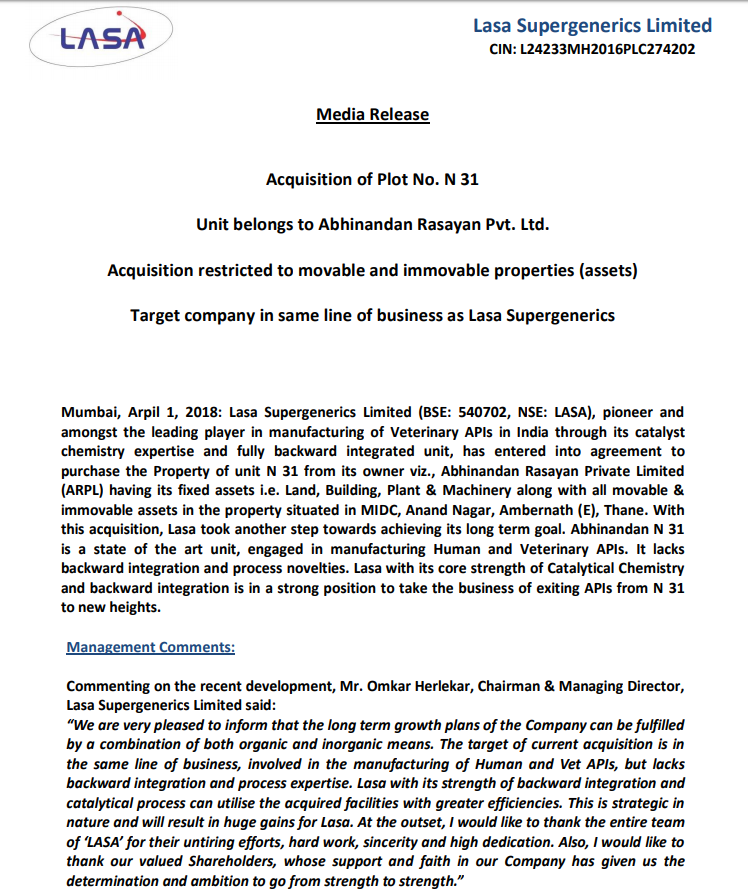

So Omkar Herlekar has walked the talk and acquired a unit, thus embarking on the inorganic growth path. The comments in the press release sound really optimistic. Any inputs @Madhurkotharay ji?

Rgds

Ankit Khemka

The major question here is how much is lasa paying and how is it funding the project?

I think this is their one step into formulations. Abhinandan probably is already selling some formulations. So Lasa gets forward integration for their APIs.

No idea about actual numbers in this transaction. Had heard six months back from someone that Abhinandan was available for 12 cr and had a 40 cr topline.

1 Like

If the 12 cr / 40 cr numbers are true, and I have no idea if they are, here is my crude calculation of the value accretion.

If Abhinandan is already a Lasa client, it is taking API from Lasa and then making formulations. So Abhinandan makes 10% (typical number for formulations) EBIDTA margin on 40 cr, or 4 cr.

If you give 10x for EV/EBIDTA (currently, Lasa is getting 5x for various reasons, though I think if there are no skeletons with the company, it should get 10x), you get additional EV of 40 cr.

If the acquisition cost is 12 cr, the market cap increase should be 28 cr or Rs 12 per share.

If Abhinandan is not a client of Lasa, then Lasa will supply API to it from where Abhinandan makes and sells formulations. So Abhinandan gets 10% EBIDTA margin on those 40 cr and Lasa gets further 22% EBIDTA margin on that (not 40 cr but on the lower value before Abhinandan EBIDTA margin addition). So in effect, Lasa gets 30% EBIDTA margin (1-(1-0.22)x(1-0.10)) on 40 cr, or 12 cr.

So additional EV would be 10x of 12 cr, or 120 cr. Minus 12 cr acquisition cost will make it 108 cr market cap accretive or Rs 47 per share.

Now, all this is just hypothetical but it makes sense to me since Lasa had guided that they will buy companies at 3x of EBIDTA price, minus debt. 40cr turnover, 4 cr EBIDTA, 12 cr valuation fit the bill.

By buying the plant and not the company of Abhinandan, Lasa probably avoided the debt component if Abhinandan has its office as the lien for the debt.

Now, we should eagerly wait for more info from the company.

1 Like

Abhinandan website says they are into API & Intermediates only…No mention of any formulations

Also my guess is since Abhinandan is into both Human & Animal healthcare, Lasa would have acquired only the Animal segment and hence taking over one of the two plants.