Hi everyone,

I have benefited a lot from learning about the thought process and reasoning of fellow members who have shared their personal portfolio. In the same spirit, I invite comments which can help me to understand better my reasoning and investment rationale.

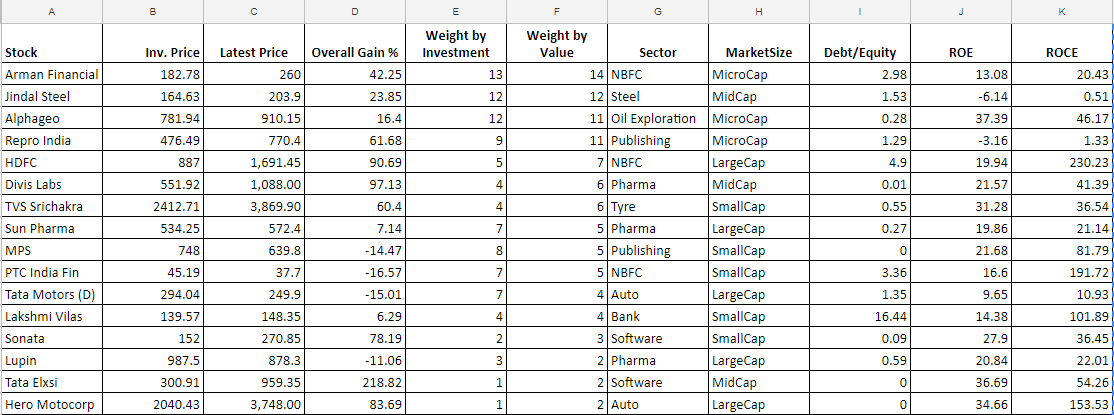

Arman Financial:

Excellent management, big opportunity, conservative lending practices and better valuations due to demonetization. It was a contrarian bet on micro-finance and given the last quarters results of various MFIs, I am bullish on the current opportunity.

Jindal Steel:

After the new steel policy, where the aim is to double the current products of 165 mt tonnes is nearly 300 mt, the sector will have a major boost. Only 5-6 players will have nearly 60% of the market. Jindal Steel, which went into JLF because of Rs. 45000 crore loan was an ugly-duckling. After its Angul facility, there is no further capex to be announced. Growing steel prices, potential order from Indian railways, stake sale of Oman plant and power plant to JSW Energy and environmental concerns in China are some growth drivers. Promoter bought warrants at nearly 145. They intend to bring strategic partners in few years which will reduce the debt further.

Alphageo:

I like businesses in unique segments. Seismic activity is a business which might not see high competition. Company has got big order from Indian government as they want to reduce the crude bill. Market feels that this business lacks potential to grow so it is giving a very low multiple to it. The cash from the current order will also reflect high dividend or bonus. The promoters have good domain knowledge.

Repro India:

I have two publishing stocks in my portfolio. I have bias for the industry as I work in a publishing firm. Print-on-demand, growth in e-commerce, proxy for online publishing market, low working capital are some of my reasons for investing in Repro.

Divis Labs/Sun Pharma/Lupin:

I invested in the Pharma basket. The valuations were very good, companies are generating FCF and have presence in multiple markets. After the plant approval, re-rating will happen. Speciality chemicals is a growth trigger which might happen in 2020-21. Also, I don’t think the share prices will go down any further. Infact, markets with a PE of nearly 27, does fall, these will be good defensive stocks to have to protect from downside.

TVS Srichakra:

The company from TVS group has very good presence in two/three wheeler market. They are focussing on branding and marketing with TVS Tyres now the sponsors for sport teams in pro-kabbadi. Highly competitive segment, but a captive customer is an advantage. More research needs to be done.

MPS:

This was a wrong investment. I thought that the CEO will be able to buy a company and turnaround. It has been a painful wait for the acquisition to happen. The 3% dividend yield was the trigger point but even that has stopped. Last quarter, they have given a specific timeline for acquisition. The lesson here was to be very skeptical when inorganic growth is being promised. I am still unable to make my mind on the next steps.

PTC India Fin:

High dividend yield, low valuations, better management team and reforms in power sector attracted me to this stock. Last two quarters have not been good for the company and the stock price has corrected and is in a range. Perhaps, the NCLT cases and the new bankruptcy laws will assist the company to recover dues and start the new credit cycle.

Tata Motors (D):

Low valuation, turnaround in Indian CV cycle, growth in passenger cycles and new products by JLR were my prime reasons for the investment. The electric variant(yet not disclosed) of JLR will give tough competition to Tesla. Also, Teslas crazy valuations was another point I had in mind. Again, painful wait, but still bullish.

Lakshmi Vilas:

Change in management, regional nature of the bank(closer to customer), cross-selling of products, improving casa ratio, good dividend yield were some of the reasons for my investment. I have also applied for the rights issue. Max as a potential promoter, NCLT cases and improving capital base might be the next triggers for the stock.

Sonata Software:

I invested mostly for dividend yield and low potential downside of the stock. The company is in niche verticals, mainly travel. I think their strategic approach of platformatisation is in the right direction. And the recent results have also been decent.

Tata Elxsi/Hero Motocorp/HDFC:

Grandfather’s gift ![]()