CMD Anil Mittal’s recent interview

AGM Notes 08th September 2016

-

Domestic Markets…The Company is seeing good volume traction in domestic markets and growth should be upwards of 20% this year. In next 3-4 years, the management believes the market share of the company in organized market should move towards 50% , around 600,000 MT per year.

-

Export Markets… The management believes reckless lending by banks to this sector has been one of the main factors for disrupting the export market. As many players who were overambitious and non-diligent, were allotted cash credit facilities in the range of 200-500 crs, and they eventually ended up dumping rice below or at cost to save themselves in crisis times. (REI Agro, Bush foods etc)

KRBL has followed the policy of branded and organized sales in export markets and has been diligent to plan inventory in conjunction to the demand of their branded product. They do not want to chase blind volume growth and compromise return/earnings profile of the company.

Going forward they believe, the pricing should definitely improve in the export markets.

(This year they have shared significant data in Annual Report on their market share in big middle-eastern markets like Kuwait, UAE and Saudi Arabia) -

Geographical indicator (GI) tag… The management believes that Madhya Pradesh shouldn’t get the GI tag, as conventionally it has been a Basmati growing region.

Also, going forward they expect APEDA to set up framework for Basmati cultivation and exports covering parameters like quality, chemical residues etc which should lead to strict enforcement of GI tag and will add to the strength of Basmati. -

Grading and packaging capacities are now in sync with Rice processing capacities with new plant that got commissioned in Sonipat, Haryana recently. The location was chosen as such as it is centrally located from rice processing facilities in Ghaziabad and Dhuri, Punjab.

-

Trying to develop new markets like China, Russia etc. Also recently got listed with TESCO in UK

-

Ramp up in advertising/marketing program with hiring of Lintas and also a higher budgetary allocation.

My comments:

The basmati is an inherently cyclical market having mini-cycles in every 2-3 year but KRBL has clearly witnessed the ability to maintain its margins and return profiles through upcycles and downcycles time and again over past 10-12 years. In recent past, Fy2016 was a challenging year for basmati industry when paddy prices were hammered and the average price range was 18-20 Rs/Kg, and lot of millers and processors got insolvent, but KRBL still maintained its margins and showed growth.

The crux of the matter is, this is a ‘Cost plus business’ where the cost of raw material is rupees X and the industry players sell at a margin of 5-7% and branded players like KRBL , LT foods and others sell at a gross margin upwards of 20-25%. So, the cost of paddy produce in the October-November window sets the tone for market prices.

The other positives with the company are comfortable Balance sheet position (D/E in the range of 0.65), low cost of funds, robust cash generating profile and most importantly Promoters who have been savvy guardians of the business.

8 Likes

Aditya, what is your opinion on the power business? Company says it is planning to increasing the capacity by 4-5 MW every year. Can this be a case of diworsification ?

There is a clarification in the last para regarding Energy related investments.

1 Like

Aditya, Thanks for replying. I went through last 5 year annual reports. Company says the order book is good for this year and it could achieve 10% topline growth this year. is it possible to find out the order details? If so could you please let me know how to find ?

Thanks for the summary on their AGM. A few points that still make me re-think on buying into the company:

- Diversification into energy: While I understand this was to do with MAT now, why does management vacillate in this regard? Also almost 1/4th of their capex was invested into this segment, it seems like they are now back-tracking on it. Conversely, why don’t they spend on advertising and marketing instead to take on the other players (backed by known brand ambassadors)

- Dependence on Middle east: Still feel that their dependance on the middle east may cause a supply-demand mismatch and may possible affect their major revenue streams. Would be interesting to know how many Indian households actually end up consuming basmati rice. Recently did a store visit to purchase basmati rice, and retailers were not too picky on which brand they recommended

Would love to hear views on the above points.

Good Article on the ongoing tussle regarding GI tag on Basmati

2 Likes

I calculated the Debt to Equity ratio for KRBL from the latest annual report and it is coming around 0.12 But the screener.in is showing 0.73 What is causing the discrepancy ? Could some one please help?

I think I found out the reason. Screeer combines long term and short term borrowings under borrowing. I used just the long term borrowings to calculate DE ratio.

KRBL looks like a very progressive company with ears to ground. Over the last few years it delivered decent returns to its shareholders.

KRBL is a Basmati Rice miller with nearly 2/3rds of sales from India and balance from outside India. For Fy2016-17, company’s domestic sales grew by 31% and overall net profit (including that of exports) grew by 36%. It also has a small windmill business that contributes about Rs.100 Crores in a turnover of ~ Rs.3159 Crores.

Its annual report of 2016-17 makes some interesting observations and is giving insight into the shape of things to come for the company and partly for the agri sector.

New products:

“…. creating a new business segment of super-premium foods by re-launching brown rice new packaging and launching ‘Quinoa’ a new health-oriented product.” (page 3)

My comment: It will be interesting to see how Quinoa takes off. How much will it add to revenue and bottomline in due course will be worthwhile watching because a 500gm pack retails at Rs.450/- in Bigbasket.

Market share: (sourced from page 30)

In value terms, Indian Gate brand enjoys market share of 32% in metropolitan areas, 35% in Town Class I cities and 43% in rural areas. However, overall for India, it is said that it enjoys 32% market share.

My comment: Somewhere, the maths does not seem to be matching because of the 3 segments two segments have market share greater than the average and the third has market share equivalent to that of the average.

In 2016-17, Vertically, company’s sales increased by 28.66% in volume terms and by 25.55% in value terms in Consumer pack segment. In the bulk packaging segment, company’s sales grew by 26.9% in volume terms and by 43% in value terms. In super premium segment sales volume grew by 19.36% while in value terms it grew by 10.48%. Export sales remained constant excluding a tender sale in which the company participated in 2015-16.(pages 27, 32, 34 & 35).

Marketing:

“The company also created a series of 11 cooking videos with star Chef Kunal Kapur.” (page 29)

“KRBL has identified social strategy as core growth strategy for the future to engage with consumers.” (page 29)

Added nearly 21,000 retailers in 2016-17 (page 34).

“India Gate brand performance has been steered by improving sales in the consumer pack categories of 1 kg and 5kg. “ (page 27)

“In its modern trade distribution channel, the company has enhanced its presence to 6500 stores, while growing market share from 27.4% to 36.9%. Initiatives undertaken by the company towards retail activation and dominating shelf-space, has resulted in improved same-store sales and category share.” (page 31)

“Viewing the huge scope of opportunity from the online distribution network, the company has focussed on strengthening its e-commerce channel. The company tied up with major players like Bigbasket, Grofers, Amazon, Shopfilo, JBL and Flipkart among others” (page 31)

Marketing thrust:

“In India, metro and class I towns account for nearly 78% of the overall packaged Basmati rice demand. However, with these markets nearing saturation, the growth momentum has slowed down. Majority of the growth is now coming from Rest of Urban and rural markets, where the company has devised strategic plans and undertaken initiatives for improving quality of distribution and improving reach. To tap these markets, the company has also launched non-premium basmati rice brands to grab market share from the unbranded players dominant here.”

(page 34)

“In India, the rural category of the basmati rice industry segment witnessed a 70% growth and this is where the majority of the growth will come from in the coming years.” (page 30)

“The premium segment was created with the rationale of capturing market share from the hue unbranded basmati rice market , which by estimates account for nearly 40-45% of the overall basmati rice market in India, and subsequently upgrade them to India Gate.” (page 27)

“The thrust is on continuous upgradation of seed quality, for which the company works in close coordination with the Indian Agriculture Research Institute.” (page 39)

What has driven the domestic growth in 2016-17:

“Consumer pack segment

…….Growth was stronger during the third and fourth quarter of the year driven by implementation of demonetisation which impacted the business of unorganised players who were unable to operate in cash crunch scenario. KRBL with its brand goodwill, robust distribution network and trade investments was able to capitalise on this opportunity and capture a significant share of market during this phase” (page 27)

“In India, the rural category of the basmati rice industry segment witnessed a 70% growth” (page 30)

“The average selling price for branded rice increased by 12.5% to Rs.45/ per kg in 2016-17 as compared to Rs.40/- per kg in 2015-16. As a result, the sales growth in value terms was higher compared to the volume terms.” (page 27)

Strengths:

“Company’s rice milling capacity of 195 MT/hour, the largest in the world, lends it a distinctive edge making operations extremely productive and cost effective. Besides, the company’s state of the art storage and warehousing capacities, innovative marketing approach, expanding distribution network, deep-rooted relations with farmers through structured contract farming……These strengths along with rising brand popularity positions the company favourably to capitalise on the growing demand for basmati rice within and outside India.” (page 25)

“ 250,000 acres — Contact rice farming network coverage” (page 25)

Macro level developments that can impact the company:

As per the table on page 19, India’s cereal exports declined in the last two years relative to 2016-17 both in terms of volume and value. This is really worrisome both for the farmer and the company, though no reasons were given by the company in the annual report.

Basmati rice realisation per ton in the international market for 2016-17 came in at Rs.54,016.58 vs Rs.78,026.17 in 2013-14 — a 30% drop. While optimistically, we can expect prices going back to those levels sometime in the next 2-3 years (this will benefit the company immensely because ~30% of revenue is exports and if that goes up 30% by value terms, it is a straight addition of 9% of revenue to the PBT, other things being equal), company’s current annual report is silent on the prices in international markets though fleetingly it says “ the average realisations are likely to increase which in turn shall boost revenues” (page 20)

“For enhancing the farmers’ income the government focusses on developing a model of contract farming and delisting perishables from APMCs such that farmers can directly sell produce to consumers for earning better margins.” (page 13)

Government of India is seriously thinking about contract farming. Here is the latest news item:

Analysis: (all data sourced from Ace Equity software)

How did this company perform in the last 11 years ie., commencing Mar 2006 till Mar 2017:

Total Income CAGR ~ 14%,

PBIT CAGR ~ 20%

PAT CAGR ~ 25.7%

Net worth CAGR (after giving dividend every year without a miss during this period) ~ 20%

Total Debt CAGR ~ 8.33%

Gross Block (now called, Property, plant and equipment) CAGR ~ 22%

Net Block (now called, Property, plant and equipment) CAGR ~ 21%

Average tax rate ~ 23% (last year tax rate 22.96%) (last five years average ~ 24%)

Average RoCE ~ 15.93% (last five years average ~18.37%)

Average RoE ~19.73% (last five years average: ~ 23%)

Average PATM ~ 7.25% (last five years average ~ 9.29%)

Dividend CAGR ~ 25%

Share price CAGR ~ 33.7% (adjusted to splits, if any)

PE CAGR ~ 7.3%

Current PE ~ 24.28x

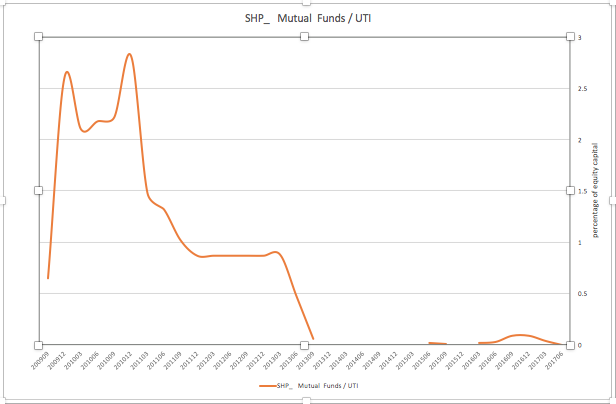

Surprisingly, in spite of such a track record of dividends and earnings, no mutual fund was holding these shares as of June 2017.

Disclosure: I own this stock

7 Likes

@All,

Patanjali has aggressively launched diff variants of Rice, again creating disruption in a new category. What do you people think of this? Stay away from stocks like KRBL & LT Foods?

While Patanjali is certainly a worthy adversary across the FMCG space, I wouldn’t pay as regards their Basmati plans. Other than the brand factor there are a few more things to consider in Basmati rice. One of the most important ones being ageing period. Would patanjali have the patience to hold 500,000 MT of basmati rice in its warehouses for 2 years? Even if it did, would it even be able to procure enough rice in a time when acreage of basmati has been declining year over year and even established players are finding it increasingly difficult to survive?

1 Like

My Notes from AGM

-

We started paying GST from Sept 22 2017 as our products came under GST purview now

-

Aim to get 50% market share in ME.

-

Iran is completely a private label market

-

We are number 1 brand in Canada.

-

We are in top 10 brands in USA. This is a very competitive market and most of the buyers are big retailers like Costco, Sams Club etc, its a negative margin market. Total market size is 90-95000 tons

-

We may export 200k tons this year.

-

We dont have inventory with more than 3 year old rice. We have some above 2 year

and below 3 year -

We have evaluated the top 4 auditors, we are not happy with E&Y as we feel they may

not be good for agri-commodities business -

It will take 6-8 months to come over the GST issues, after that we are likely gain

-

market share from unorganized sector. right now our focus is to maintain our market share.

-

Situation is very fluid now. Any new capex would start only after the GST issues are resolved

-

No capex plans right now.

-

New capex will be after 8 months and will be in rice only. we will not venture into other

agri-commodities like pulses etc -

The paddy procurement season has just started now. Price is around 27 rs compared to 22 rs at same period. Last year we bought upto 32 rs. Management is of the opinion paddy price

should not too low otherwise farmers will not sow basmati next year. reasonable price should

be around 30 rs. We will buy only 0.5 mt (last year 1 mt). This is a cyclical business, one year

basmati prices would go up and next year go down and next year up… This year there is a shortage of 10% in the system whereas last year there was carry forward inventory -

We will maintain the 20% ebidta margins and in fact increase 200 bp due to strong brand and inventory gains

-

Quinnova may hit sales of 500 cr in next 5 years

-

We may take price increase after 6 months

Disc : I hold less than 5% in my pf. I may have noted down some numbers wrongly due to noise in the auditorium, please do your due diligence

7 Likes

Any short term negative impacts on KRBL from this?

I think in one of confidence call krbl has clarified not much business in Europe but still check it

While sales/revenue of KRBL and LT foods are more or less same around 3200 cr…why is that KRBL’s margin is double than that of LT foods ?

Anyone tracking LT foods ? Any views?

A simple check of prices shows that 1 kg of Basmati rice classic of India Gate sell for about Rs.200 while 1 kg of traditional basmati rice of Daawat sells for about Rs.163. This is a pretty big difference considering raw material prices are going to be almost the same for both brands. The difference I think comes from the brand value of India Gate vs Daawat and the fact that India Gate basmati is aged for 2 years. Also, I notice that Daawat frequently gives 25% Free on most of its packs which should also hurt its margins as the numbers show. KRBL seems to be a far superior company IMHO.

Disclosure: Tracking the sector, no holdings.

2 Likes

considering valuation as a dependent variable, there are many predictor variables for valuation. Some of them being growth, leverage, governance, brand power, return on capital etc. Compare these two companies on these metrics and you will have your answer

KRBL ROE 22%, Daawat 20%. not much difference, but mcap of KRBL is 8x of Daawat.

90% of sales come from branded products for KRBL. Its 70% for Daawat. this explains Daawat sells more and at lower margins.

However brand recall of India Gate is much superior and the management has decades of experience in this field and they have more management bandwidth compared to Daawat.

Regarding 8x difference in mcap, I feel the gap will slowly narrow down. Daawat has plans to raise 500 cr soon, e-voting is going on. In my view both are good investment bets, after 2 quarters GST issues will be sorted out and both will gain mshare from unorganized sector.

Disc : Hold both , each more than 5%

1 Like

There is a reasonable amount of irregularity in Daawat’s books of accounts (especially in their inventory valuation). Average closing stock of rice in LT was valued at 45/kg whereas the same in KRBL books was valued at 32/kg. Some caution is advised notwithstanding the steep valuation difference.

1 Like