Very nice presentation @leon_lph. Thank you for sharing.

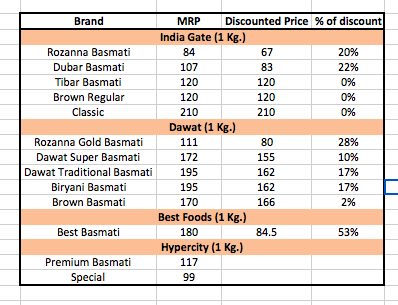

Some scuttlebutt on customer prices:

KRBL is not giving any discount on their high end products - Tibar and Classic.

Dawat is giving around 17% discount on their premium tier.

In general, market is very bad as can be judged from Best Foods which is giving 53% discount.

In the Hypercity I went, the shelf space and display/marketing of India Gate products was inferior than Daawat. Need to check other stores. Request fellow investors to check as well.

I would do scuttlebutt for 5kg/10kg packages next week hopefully.

Thanks,

Rupesh

2 Likes

Indeed, I invested in LT foods along with KRBL, because in the Supermarkets, the Daawat and Kohinoor brands have a) Better and more premium packaging b) Better Shelf Space c) Better Customer Recall and d) Higher Pricing

However, the price action has deviated from this, because I bought KRBL around 42 and at around the same time LT Foods at 80. Similar sort of PE ratios too. And KRBL has given much better returns. Just tells you that financials are important too.

1 Like

Looks very good from all angles…

Branded product available at the price of a commodity with long term growth prospects that too without limited capex. Current plant in Dhuri is still under utilized. No need for much capex for next 5 years.

They have promised to reduce debt levels from 2015 onwards which is again encouraging although I couldnt find that statement in the latest investor ppt. Nonethless it is still highly undervalued, following are some areas of improvement:

- more capex in renewables may be unwarranted, not much value add there, why dont they pay more dividends or repay loans, I am positive this would improve

- not to compromise on margins despite difficult times especially this year and focus more on branding in middle east etc

- need to verify whether its somewhat insulated from paddy prices or can they pass on the prices in the long run

1 Like

Good summary @atishay1 …

Also,the agm is on 28th of september . Interested people can join … the management is willing to take reasonable questions from shareholders .

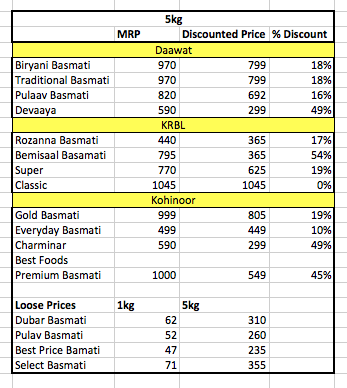

Did some more scuttlebutt on 5kg pricing a while ago.

Below is the table:

1kg and 5kg India Gate Classic brand was either absent or had very poor shelf space in Hypercity, Spar and More stores. If somebody can check two biggies - Big Bazaar and D-Mart that would complete the picture.

I don’t see domestic sales of KRBL picking up and Export remains the saviour for coming quarters. Even there, I think similar story will play out. These are testing times for India Gate as a brand.

Further drop in paddy prices means that KRBL has to manage high price paddy procured 18-24 months ago.

I think when paddy price cycle turns - then KRBL might be an attractive play for 1-2 years after that.

Disc: Sold partially yesterday. Looking to sell half holdings on rallies.

2 Likes

CAG Blows the Lid on Rs 100,000 Crore Rice Milling Scam

http://thewire.in/2015/11/25/cag-blows-the-lid-on-rs-100000-crore-rice-milling-scam-16183/

I don’t think government sell costly “basmati rice” in the PDS…Therefore KRBL should be minimally impacted…

CAG is over exaggerating things. This is what happens when accounting ppl who don’t know have field experience try to evaluate things.

The value of by-products taken by CAG is of too extreme amount. The by-prodcuts market value fluctuate a lot which even a rice miller can’t estimate. Sometimes they raise 200% in a month and same time goes to 25% of value the other month.

The major scam is going on other side i.e the p.d.s distribution side. There are many ppl who buys this p.d.s rice from distribution ppl at Rs.2 repolish it and sell it for around Rs.10. This is a major scam.

& there is other scam. Officers who give paddy for custom milling directly asks millers to take a kilo extra(101 instead of 100) while taking paddy and share that amount with them.

1 Like

Hi @leon_lph

What are your views on the q3 results for KRBL and how it compares with other players?

I am interested in knowing whether the difficult pricing environment is across the industry or just for KRBL?

From the concall, q4 also looks to be tepid and growth will come from FY17 only (probably in the lower half).

Also what are your views on continuing energy expansion i.e. will they continue to do the CAPEX going forward like they will do in FY17?

Hi,

Did anyone attend the Q3 earnigs con call? It would be very helpful if someone posted the key points that came out of the meeting. Specifically wanted to understand if the company had shared any updates on:

- pricing situation and what it looks like this year wrt the demand/supply/acreage

- Impact and possible timelines for the Iran exports coming back on line.

- Capacity utlization of Dhuri plant.

- What are the economics of the investments into renewables?

Thanks

Kaushik

Disc: Invested recently

- Regarding pricing : My sense is market prices should be seen in conjunction with raw material prices. But, yes in a broad sense, both prices have come down this year.

As the RM prices come down, so the market prices have also come down and KRBL has also adjusted its selling price accordingly.

But as you can also see form the results the margin at gross front or operating havn’t been affected.

The crux of the matter is KRBL sells ‘non-aged’ rice at market price plus certain premium which my sense is should be around 15-20%. And if this statement holds true over time , their profitability shouldn’t be affected by difficult pricing situations

For aged rice, i checked in the market, the prices havent changed … i would urge you to do the same

- Regarding the demand situation, mgmt has said that due to extreme volatility seen in mandi prices of basmati this year, both millers in India and exporters abroad have been baffled … the prices moved to and fro between 18-30 Rs/KG and hence many exporters have been in the waiting mode as they didn’t want to purchase at a price that might at the end appear to be too high.

But, again the mgmt’s sense is rice stocks should be depleted in middle east markets and the exporters will return in a month or two’s time for purchase.

- Renewables: Krbl mostly invests in Wind energy and with more efficient wind turbines in the market , the IRR for producer has been improving .

Also, the IRR calculations for wind energy in many wind industry reports is also being shown around 20% , which is the figure KRBL mgmt has also been guiding.

They always stated their intent for continuing renewable capex to the quantum that Consolidated tax rate comes around MAT around 20%.

2 Likes

Hi @leon_lph

How do you read the Q4 results for KRBL. They are saying that 70% of the paddy has been already procured at the lower prices last year. And as the farmers are moving away from cultivating rice (because of lower prices last year), they expect better realizations this year.

Looks to me that they should have some margin expansion in 2017. What will happen if rice prices don’t recover? Will the margins remain same or under pressure?

Thanks,

Mukul

Hi Mukul

Based on the Total Basmati market volumes and expected supply in the coming crop season, the management expectations of prices moving higher looks reasonable…

These kind of mini cycles happen in basmati every 2-3 years… check previous 10-15 year history

If the rice prices remain the same, then the margins will also remain the same most likely… they have given out data for cost of paddy/inventory and average market prices

Best,

1 Like

alphainvesco continues to hold with no fresh entry

https://www.alphainvesco.com/blog/annual-letter-2015-16/

Q1 results out:

The article says, total basmati exports fell from 29,000 crore in 2013-14 to Rs 22,714 crore in FY16 due to a decline in shipments to Iran.But Sales of KRBL improved from 2,791Crore in Fy14 to 3,358Crore in Fy16.If I understand correctly only 30% of KRBL’s sales are from export.This makes them to have only 4-5% market share in the overall Basmati exports.

Can someone pull up numbers for exports of REI agro, Kohinoor, LT? I am just inferring from above posts, feel free to correct my numbers 4-5% looks too less. Is the size of unorganised sector outside these big ones so big?

1 Like

Hi Ishan,

Since Kohinoor, LT foods etc are all listed companies. Its should be easy to find numbers and it is mandatory by accounting standards to give a geographical breakup of sales.

Also, overall basmati exports in quantity and value terms can be found from APEDA website.

Best,

Krbl has mentioned in their con call that they got a big one-off order from Iraq last year which is not going to be repeated this year. Some of the impact already happened during Q1, rest will come in Q2.

1 Like