They will get AGM invite every year BTW, KRBL promoters can just hope now they won’t show up all the time.

1 Like

These are generally sale of mutual funds as they mature and again buying new units. If you look carefully in the notes, you should be able to trace it.

Disclosure: No position in the stock

Hey guys, I wanted to get expert opinion from others on below point.

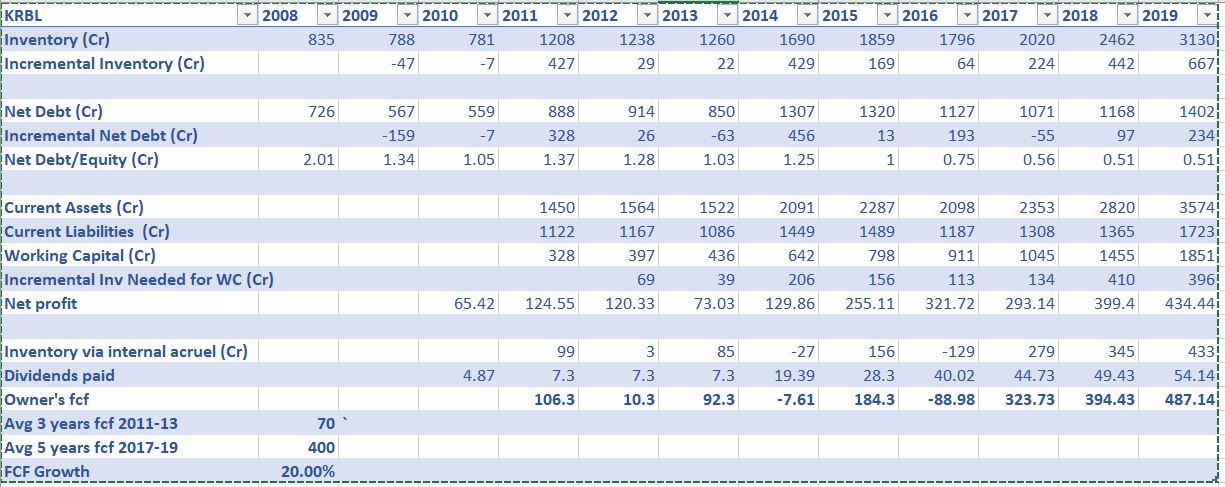

I spent some more time on valuation for KRBL and also read Amit Rupani’s presentation above. His owner’s FCF explanation was pretty convincing. i.e to assume additional inventory bought using internal cash as part of FCF. Assuming that KRBLs business keeps growing at 12% CAGR, I tried to picture the owner’s FCF. I looked at your screen shot and subtracted net debt from incremental inventory to come up with inventory funded through internal accruals. Additionally, I added back dividends to this number. Then to consider for the 3-4 year cycle. I took avg FCF for 2011-13 and 17-19 which range from 70 Cr to 400 Cr with around 20 % growth. I anticipate this growth to drop in next 10 years to 11-12%.

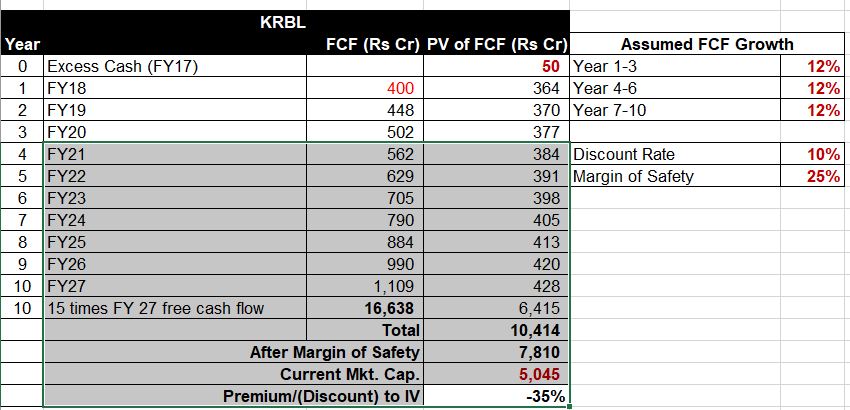

Then I tried to do DCF valuation with fcf of 400 growing at 12 % with 10% discounted rate. It brought Mkt Cap around 10,000 cr. There is no other company in the world that can store this much inventory and yet have as strong balance sheet as KRBL. Thus, it becomes a competitive advantage for KRBL that is becoming durable day by day as they grow.

Do you guys think my assumptions are fair to value the company around 8000-10,00 0 Mkt Cap or around 400 rs per share Keeping the management issues aside. i.e assuming all those issues go away in span of another year or two.

How does your valuation look like?

5 Likes

Rice exports drop 27% YoY in April-July: Govt

Folks, any idea on why KRBL is down 10% today. I can’t see any fillings on BSE.

Is there any news/update on IT order?

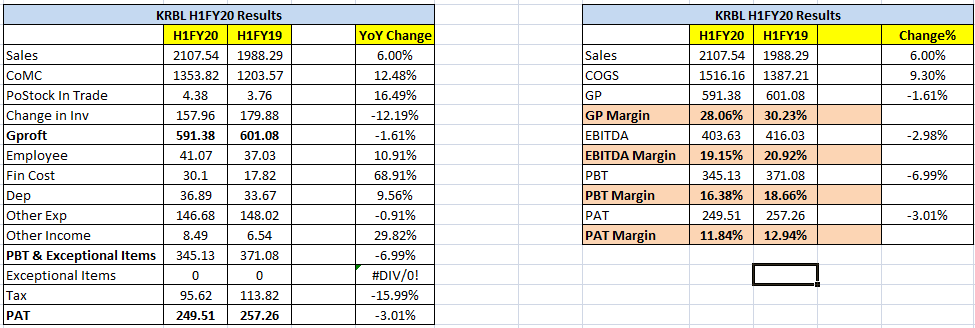

Pretty bad set of results (Link)

Investor Presentation (Link) - Big drop in exports volumes

@rupaniamit Any comments?

Disclosure: Invested

Q2 results look bad but H1 look OK. Margins are in-tact and have not collapsed.

Need to hear from management on tomorrow’s con-call reason for significant drop in exports volume. In Q1FY19, they had 200-250cr worth of cargo lying at the port which wasn’t shipped in-time to be considered as sale for the quarter and it was deferred to next quarter. I wonder if something like that has happened in Q2. Let’s check tomorrow…

147cr payment under protest to tax authorities have put little strain on WC and balance-sheet.

Looking forward to get update on two issues from the management.

5 Likes

Just listened to the concall. Management sounded very bullish on the future prospects. Exports sales fell because of 300cr consignment got stuck at port which has been shipped in Oct.

Company is guiding for strong Q3 and ~10% overall revenue growth for FY2020. Company is confident about favorable judgement on IT notice and saying IT department is unnecessarily sitting on the order.

Story remains intact but the IT notice remains an overhang.

Disclosure: Invested

1 Like

KRBL Q2FY20 Earnings Call Highlights:

Participants:

- Sunidhi Securities

- Subhkam Ventures

- Care Portfolio

- SKS Capital

- Vallum Capital

- Nippon Mutual Fund

Business Overview:

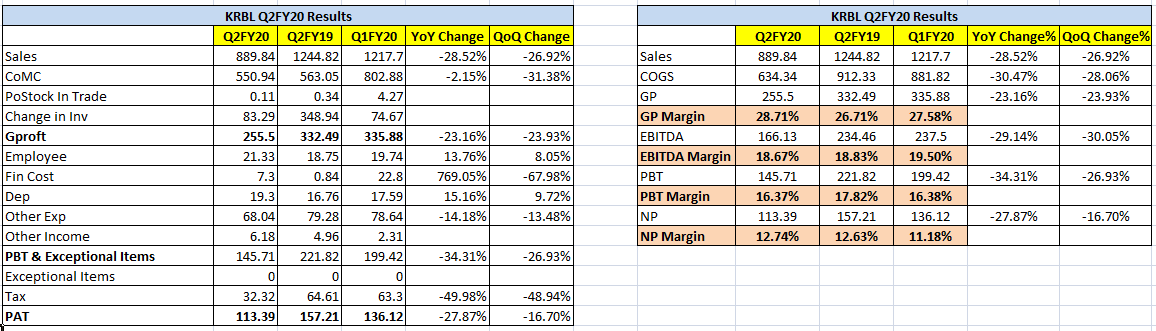

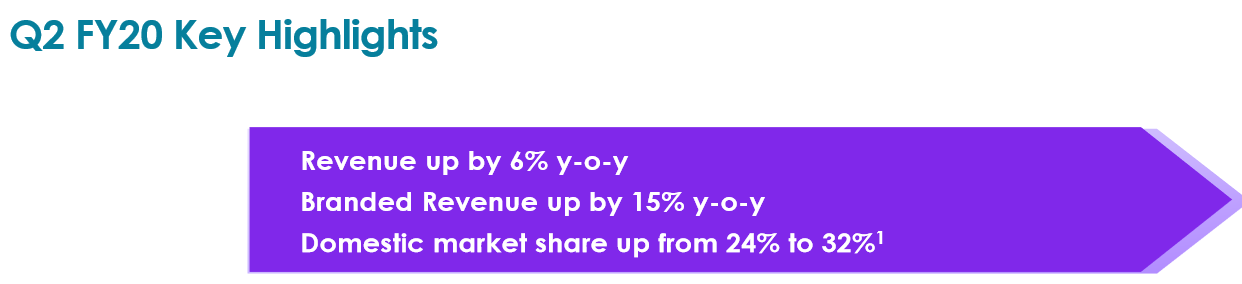

- Revenue at Rs 890 crore vs Rs 1,245 crore YoY

- EBITDA at Rs 172 crore vs Rs 239 crore YoY

- PAT at Rs 113 crore vs Rs 157 crore YoY

- Export revenue at Rs 313 crore vs Rs 635 crore YoY

- Net working capital debt stood at Rs 60 crore vs Rs 1,424 crore in March 2019

- Operating cash flow at Rs 1,365 crore and free cash flow at Rs 1,349 crore

ConCall highlights:

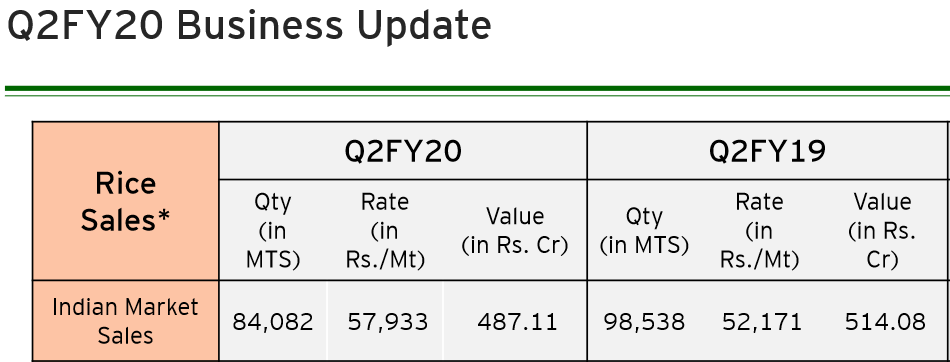

- Realization: Domestic at Rs 57,933/MT vs Rs 52,171/MT YoY; Export at Rs 86,137/MT vs Rs 76,698 MT YoY

- Inventory: Paddy at 104,922 MT; value- Rs 361 crore, Rs 34,432/MT. Rice at 302,290 MT; value- Rs 1,537 crore, Rs 50,836/MT

- Export declined as some of the ordered rescheduled for Q3; orders of 62,000 MT were stuck at port which cleared in October

- Crop production is around 20% higher than last year

- KRBL not reduced any prices despite rice in basmati rice production

- Europe market used to be around 300,000 MT but post the pesticide issue it has come down to 92,000-100,000 MT; 200,000 MT has been taken by Pakistan

- Saudi has introduced Certificate of Conformity (COC) for basmati rice; post 15th December all shipment to Saudi will go under COC. The cost of COC will be borne by the buyer

- Total domestic basmati rice production was 6.5 million tons last year, out of that 4.4 million exported

- Total basmati rice export market is 5 million tons; 4.4 million tons from India (65% to Iran) and 0.6 million ton from Pakistan

- Income Tax appeal outcome: KRBL is hopeful that the verdict will be in favor of the company. Company paid Rs 159 crore till date and will continue to pay Rs 12 crore on a monthly basis till the final outcome is not going to be out

- Net realization will come down in coming quarters as there would be mix of old crop and new crop but margin will remain intact

- KRBL will continue to do business with Iran either via Dubai or Iraq; any negative surprise on US sanction will impact the volume and may impact the realization

- Rs 1,500 crore payment is due from Iran to few Haryana based exporters which likely to be cleared in the current month

- Quinoa division is not growing as earlier anticipated. Domestic quinoa market is not more that 1000 MT and KRBL is doing around 150-160 MT

Capex:

- KRBL is spending Rs 20-30 crore every year to increase warehousing capacity; it has 2.7 million sqft of closed warehouse

Guidance:

- KRBL has guided phenomenal growth for the December quarter as orders of Q2 has been postponed to Q3; full year revenue growth will be 8-9%

- KRBL will achieve highest ever inventory by September 2020

8 Likes

Income tax appeal outcome, Iran issue and ED attachment are key events to watch out for in near term for KRBL. I feel the inventory of KRBL is as good as cash (assuming it is reported correctly). Much worried about the ED issue and involvement of management, intentionally or unintentionally.

1 Like

I truly respect Anil Kumar Goel especially how he is investing with KRBL on the basis the way he is committed with this counter from long time and keep sipping on every dips as he seems to believe with Indian consumption story and growth of middle income segment within India. If anyone tracking prices would have booked profits at many levels but surprisingly seeing him adding(pure sipping) at all levels.

Disclosure: I am passive investor from long time and trying check current market condition. I am holding this counter from long time from 18 Rs level and planning to add more based above conviction like Anil is having.

2 Likes

LT foods has come up decent results yesterday with all-round improvement. It is surprising that it is still trading at about 5 PE despite its good recovery from recent lows.

From LT Foods Presentation:

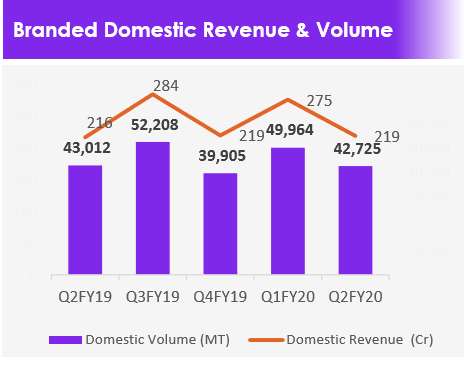

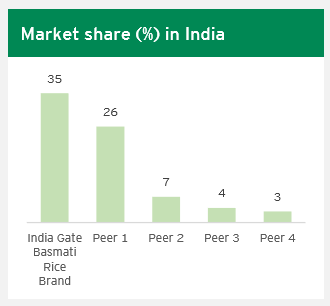

They have claimed (according to Neilsen Survey) that they have gained domestic market share from 24% to 32%. Surprisingly, KRBL did not mention domestic market share (in % terms) details in its investor presentation this quarter.

From LT Foods presentation:

Branded Domestic Revenue & volume stayed flat Y-o-Y.

From LT Foods presentation:

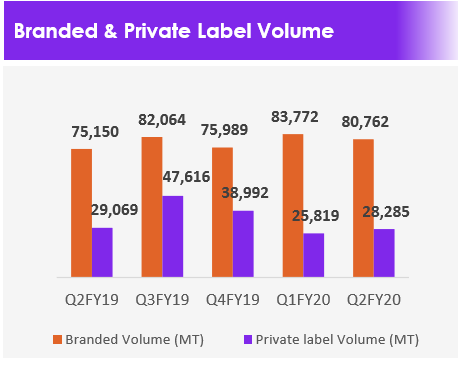

Private Label Volume overall reduced.

From KRBL Presentation:

[Edit]

So, KRBL Domestic Volume reduced by about 15% Y-o-Y. Missed the above slide.

From Q4FY19 presentation:

84,082 MT KRBL’s Volume in Q2 Vs 42,725 MT LT Food’s volume with LT food market share being 32%?

So, KRBL seems to have lost some domestic market share. But, KRBL’s volume is still double than LT Food’s. Can anybody suggest, if my analysis is wrong somewhere?

Disc: Invested in KRBL @440, no position in LT foods

2 Likes

Saw KRBL - India Gate- ricke in UK for the first time. It was priced at £3.00 (Rs 275) per kg, which is what Tilda is priced at. Tilda is the premium basmati rice in the UK.

2 Likes

Some top of mind observations from KRBL Q2FY20 Concall:

- Iran exports at risk as Iran has put condition that India needs to buy oil from it so that it can import goods from india in Rupee terms. The Letter of Credits seems to have completely stopped due to US sanctions. Some part of Basmati demand from Iran will be fulfilled via Iraq & UAE. [Big Risk going forward in short term]

- Management seems to be confident that income tax dispute decision will be in KRBL’s favor (personal opinion is the final tax demand could be about 50% of original demand [middle path]). So far paid 160 cr until end of Oct.

- Accepts & appreciates dawat is clear market leader in US with more than 50% market share but they are not able to figure out how dawat is able to make profit at the prices they are selling [Strange]. KRBL’s market share constant at <10% (??).

- Regaining lost share in Exports to Europe [due to pesticide issue] is still long way away as it seems the farmer awareness effort might not be yielding faster results.

- Management is not planning to cut down procurement this season despite Iran exports threat[ Only in future, we will come to know how prudent this decision is going to be].

- KRBL seems to be the only brand which is paying GST in India. All remaining brands are not paying GST by putting a disclaimer that the brand on the packet is not exclusive and can be used by anybody.

This is the primary reason why despite a great biryani consumption growth, KRBL’s institutional sales are not growing fast (as per management). - No mention of ED case but this is another hangover on the stock price as usual.

The above notes are my understanding from concall & there could be mistakes & misunderstandings.

Disc: Invested

3 Likes

Number of shares purchased is small. May be it is just to support the falling prices. Negative surprises cannot be ruled out.

Disclosure : invested. presently in loss

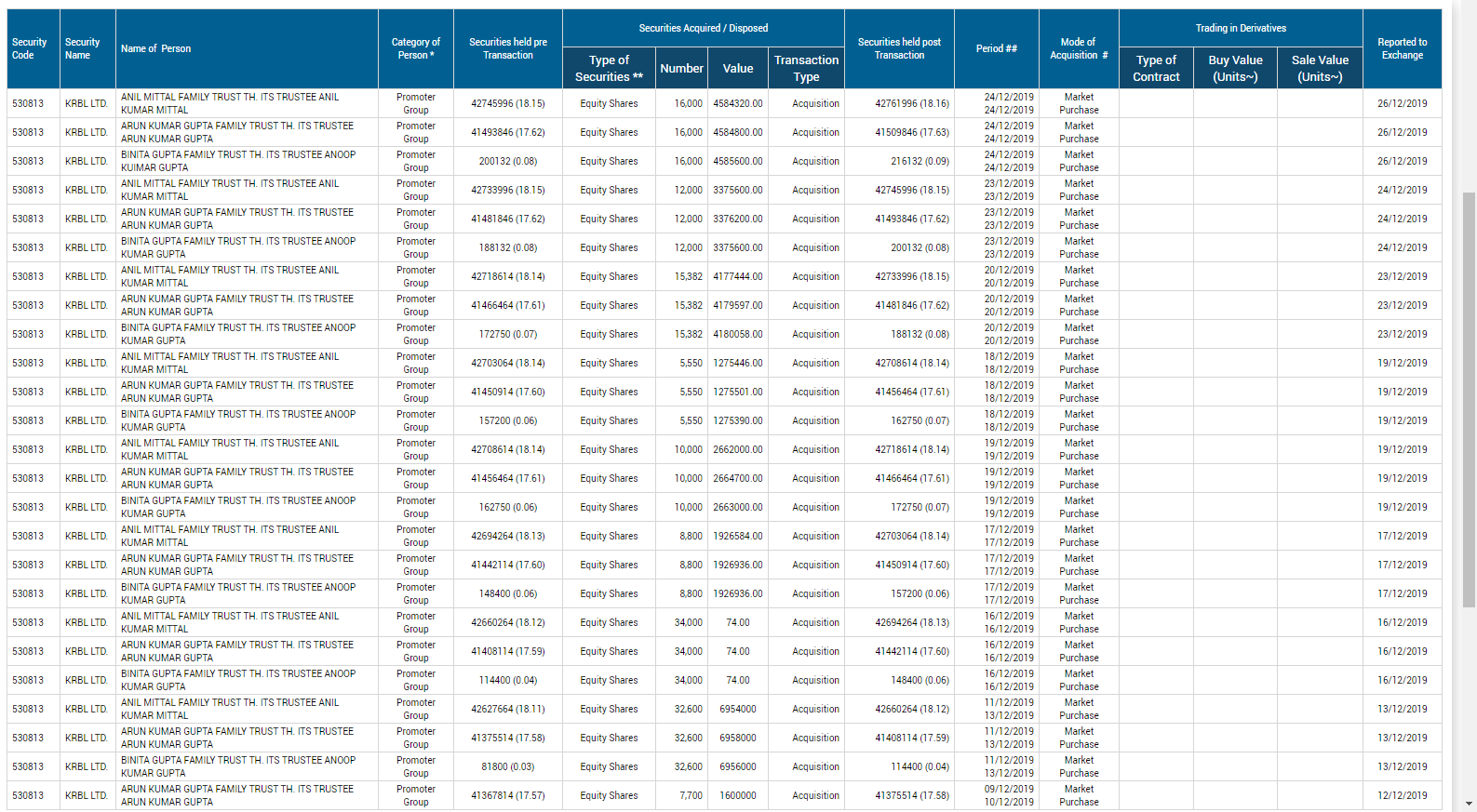

Acquisition of 97,800 equity shares worth Rs 208.68 lacs by promoter groups

Anil Mittal interview

disc: not invested

3 Likes

Strong confidence by promoters in the business. Demerging power business will be an additional catalyst.

Disclosure: Invested