I was invested in KRBL since 2012- 13 and kept adding till late 2015, exited entire portfolio today. Management will have to put in significant energies to fight ED led cases to conclusion. Even if they are not involved in any wrong doing, law in India is slow and they will have to go through the pain irrespective.

1 Like

It was clear right at the beginning when the controversy broke out that everything was not above the board. One should read between the lines. See posts around this interview here: KRBL- The King of Basmati rice

This also reminds me that Kotak came out with a strong defence of KRBL at that time (that too given above) and compared it to Amazon ! So much for expert opinion…

I think retail investors should always stay away even from “suspect” cases, even if it means letting go of one or two good opportunities. Generally it has been seen that there is no smoke without fire.

2 Likes

Hi Mukul,

Re: Tax Notice - management shared in Q3FY19 and Q4FY19 con-call that tax authorities don’t have a case and its confident that tax claim issue will be solved in KRBL’s favour. There are lots of companies which have cases pending with IT departments under protest. In KRBL’s case - this amount is huge but will have to wait and watch. If they would have known that they have done something wrong, they would not tell on con-call of being confident to overcome this issue in their favour. I’m closely monitoring it and waiting for an update from management.

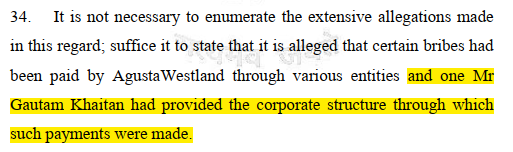

Re: 15cr ED “provisional” attachment - management has denied any involvement but put the blame on ex-director Gautam Khaitan. Here is the link. In Jan 2019 case ruling - court gave clean chit to Balsharaf which shows no involvement of KRBL in any wrongdoing in AugastaWestland case. I encourage you and everyone else interested to read the court judgement here. It is my understanding that Balsharaf has sued ED to claim loss incurred for not allowing their transaction with Pabrai to not go through. Amount is close to Rs. 150-200cr. One can sense why ED would be after KRBL and digging 10 year old case and now provisionally attaching 15cr property. However, this 15cr attachment has taken-off ~1500cr of KRBL’s market cap and brought it to very interesting levels.

Often “better” opportunities in the market come with high stress. And this makes some strategies emotionally challenging. One needs to be check if this falls in one’s comfort zone. I’d recommend newbies to stay away until there is enough clarity on severity of issues and not venture in. One needs to understand the issues at hand deeply, decipher the extracted information, and then evaluate the risk-reward ratio.

In my humble opinion - current issues will definitely have an overhang on the market price until management clarifies and sorts out the issues. It might not see a V recovery anytime soon.

Disc: have trading and long-term investment position and hence biased.

8 Likes

ICRA downgraded KRBL’s rating on long term bank facilities from ‘AA’ (Stable) to ‘AA-’ and also placed it under “ratings under watch with negative implications” after The Enforcement Directorate attached assets worth Rs 15 crore of the company in connection with 2008 Embraer deal case on July 4.

//www.bseindia.com/xml-data/corpfiling/AttachLive/dd455139-e7f4-4cb1-87b9-79a15f80e64f.pdf

Thanks Amit for the detailed reply.

Valuations are definitely attractive but these corporate governance issues are big overhang. As you rightly mentioned, better strategy would be to wait and watch for their Q1 concall.

Interestingly, the management has met multiple mutual funds yesterday in one on one meetings as per their corporate announcement on BSE.

Thanks

-

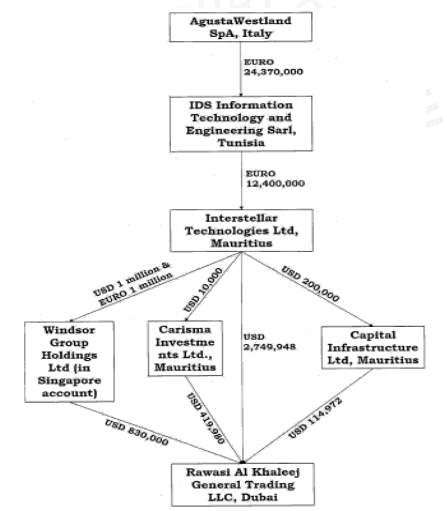

It is further stated in the Counter Affidavit filed on behalf of the Enforcement Directorate that a search was conducted by the Income Tax Department on the premises of M/s KRBL Ltd. During the course of the search, it was revealed that in the books of RAKGT, two ledger accounts were maintained: one in the name of Omar Ali Balsharaf-DO and the other in the name of Omar Ali Balsharaf-GK. As per the said ledger account maintained in the name of Omar Ali Balsharaf-GK, RAKGT had received money directly from M/s Interstellar Technologies Limited and other companies, which in turn had received proceeds of crime directly or indirectly from Interstellar Technologies Limited. It is affirmed on behalf of the Enforcement Directorate that “the proceeds of crime are suspected to be parked in the accounts of M/s Rawasi Al Khaleej General Trading, LLC Dubai under the ledger entries of M/s Omar Ali Balsharaf -GK who is a major shareholder of M/s KRBL Limited…”

-

It is affirmed that Interstellar Technologies Limited also transferred Euro 1 million and USD 1 million to M/s. Windsor Group Holding Limited during the years 2009 to 2012. Out of the aforesaid amount, USD 830,000 were transferred to RAKGT during the period 03.02.2010 to 13.02.2010. Similarly, Interstellar Technologies Limited transferred USD 10,000 to the accounts of one M/s. Carisma Investment Limited in the year 2010 and that company transferred USD 419,980 to RAKGT between 18.04.2009 to 27.02.2010. Further, Interstellar Technologies Limited also transferred USD 200,000 to the accounts of Capital Infrastructure Limited in the year 2009 out of which USD 114,972 were transferred to RAKGT on 18.04.2009.

It is perfectly clear

1)Why KRBL has to maintain two ledgers ?

2)ED doesnt have any personal revenge with KRBL! KRBL had received money without sending RICE

KRBL had received money without sending RICE

3)What is the relation between defence company nd rice miller. Sum of 24mn euro.

4)mr.khaitan was middlemen 15cr worth of land been given to mr.tyagis (former IAF CHIEF) company.

5)Everything was done with out permission of KRBL promotors? R they sleeping?

Disc.:- Not invested

2 Likes

Amit

I all humility, I think you have completely misread the Delhi HC judgement.

First, the petitioners are Omar Ali Balsharaf Vs Enforcement Directorate.

KRBL is not involved in the petition, so the High Court has not at all gone into deciding on the question of whether KRBL is guilty of any wrong-doing.

The limited question the High Court has decided on is since the shares were bought by Balsharaf in 2003 before the “alleged” crime took place, he could not have bought the said shares with the “crime money.”

Thus, ED was wrong in blocking the sale of shares and wrong in freezing (confiscating) the shares.

In fact, during the case hearing ED has been very elaborate of how KRBL was used to route the bribe money.

In fact, have a look at this

Let us try to add 2+2 and try and connect a few dots - I agree the following exercise is pure witch hunting, but it helps to know

-

Brother of Congress MLA (Aditya Khanna) from Sangrur admits to being complicit in the Oil for food scam (2006). KRBL rice mill is located in Sangrur.

Aditya Khanna is also related to Natwar Singh the ex-foreign minister of India.

Khanna admits role in Oil-for-Food scam | India News - Times of India -

Andaleeb Sehgal, close friend and “saala” of the son of Natwar Singh - Jagat Singh is named in the Oil for Food scam by the US Volcker enquiry in the oil for food scam.

Andy's story - Nation News - Issue Date: Nov 21, 2005 -

Come 2016, father of the Aditya Khanna from Sangrur is named in the Embraer defense deal. Vipin Khanna is known to be a defense dealer and his name as popped up almost in all defense scams in the last 15 years

CBI Names UK NRI in Embraer Scam - Asian News from UK

It is pertinent to note that the latest “provisional attachment” of property of KRBL by the ED is in the Embraer case.

So to conclude

- Delhi HC never said KRBL is not involved in the crime that was committed (VVIP Chopper scam)

- There seems to be some uncomfortable connection between the various entities involved across multiple scam. Of course KRBL has not been accused of being a main party to crime.

- Embraer is a new case - we don’t have much information on this yet.

- KRBL is a very robust operating business. Unless there is accounting fraud in the company, these issues should get sorted in the next few years (either guilty/not guilty). In the meantime, the operating business will keep performing well/better.

11 Likes

Thank you for your message, Amey.

I have read Delhi HC judgement at least 5 times from when it was published. I understand the overall scope of this case. However, if I had clarified why I stated that KRBL did not do any wrongdoing in Augusta Westland scam, there would have been less room for misinterpreting my statement. I should have added my reasoning clearly in my above message.

Below is the big question that I ask myself all the time:

If RAKGT proved to be safe haven for parking Bal Sharaf’s “crime money” as per ED’s allegation, why no case has been filed against KRBL by Indian law enforcement agencies so far?

-

No case has been filed so far against KRBL because ED has not been able to ascertain the exact nature of this transaction (money received by RAKTG from petitioner) per the judgement which they were still investigating. ED was not able to explain to the court that on what basis petitioner is recipient of proceeds of crime.

-

It is mentioned in the judgement that the search was conducted by the IT department on the premises of KRBL. During the search, two ledger accounts were found for the petitioners and ED is suspecting that “crime money” is parked under these ledger accounts. But why is ED not able to prove that petitioners have actually parked “crime money” with RAKGT? If ED was able to prove this, they had all the right to “attach” petitioner’s KRBL shares in India. But ED was not able to prove it. It was ED’s pride at stake with this case.

-

Please go through this you tube video https://www.youtube.com/watch?v=--YXWJqx1_E. At 6:20 Annop Gupta has said that petitioner is their big distributor and KRBL has sold rice worth more than $3 billion in last 10 years. So imagine the number of ledger entries that Income Tax and ED would have looked into. But they didn’t find any proof to confirm that petitioners parked “crime money” with RAKGT.

Hope this clarified why I said KRBL is not involved per my interpretation of HC’s judgement.

I will appreciate if you can find and share anything that I may have missed. Together with you and other interested curious VPers would like to get to the bottom of this.

9 Likes

Dug out some more dirt on the routing of crime money in the VVIP chopper scam

What is this 15 Cr commission that KRBL is talking about.

If this “offer” by Gautam Khaitan was received by KRBL around 2009/2010 (guessing) then why did KRBL wait till 2013 after the arrest of Gautam Khaitan to make him resign from the board of KRBL?

5 Likes

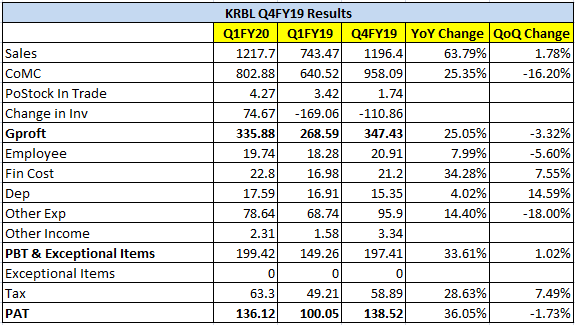

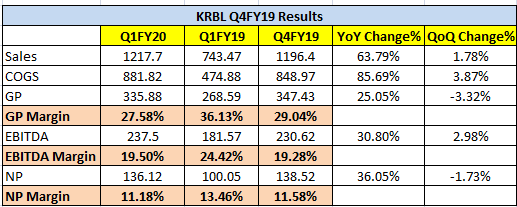

Decent Q1FY20 results from KRBL. Topline growth of 63.79% is skewed because around 150cr worth of cargo was lying in port and they weren’t able to ship it in time because of which that sales was pushed to Q2FY19. So one shouldn’t get very excited with 63.79% top line growth number. Decent margins. Will wait to hear for management commentary on tomorrow’s con-call.

2 Likes

Two important notes:

1/ "During the previous year, the Company had received demand notices under section 153A/143(3) of the Income-tax Act, 1961, with respect to assessment years

2010-11to2016-17, amounting to Rs. 75,744 lacs and interest thereon Rs. 51,176 lacs. Vide writ petition filed, the Company has obtained an order from Hon’blc

High Court of Delhi, that no coercive action shall be taken against the Company. The management of the Company has contested this demand at CIT (Appeals),

New Delhi. Further, the Company is rc<1uircd to pay Rs. 25,384 lacs under protest for contesting such demand. The Company was required to pay Rs. 2,StlO Lacs

per month for first three months till 31 l!arch 2019 and thereafter, required to pay monthly instalments of Rs. 1,200 lacs as agreed with the income tax

department. As at 30 June 2019, the Compay has paid Rs. 11,100 lacs, under protest. The management, based on legal assessment, is confident that it has a

favourable case and that the demand shall be deleted at the appellate stage. The auditors of the Company have invited attention to the aforementioned issue in

their review report for the quarter ended 30 June 2019. "

2/ "Subsequent to the <1uartcr ended, 30 June 2019, the Directorate of Enforcement CED’) has provisionally attached a portion of land parcels and building

thereupon, situated at Dhuri, Tchsil Sangrur District of Punjab, to the extent of value of Rs. 1,532 lacs in connection with its money laundring invetigation. The

said land parcels and building thereupon arc located adjacent to one of the plants of the Company and would have no impact on working of the said plant. The

management based upon the legal assessments, is confident that it has a favourable case and the said attachment shall be vacated at an appellate stage. The

auditors of the Company have invited attention to the aforementioned issue in their review report for the quarter ended 30 June 2019. "

Not able to understand why they are paying 250+ cr to IT department when they are contesting the demand. Hopefully management explain this in detail in concall on 3rd August.

1 Like

To contest the demand at the appellate stage, the assessee has to deposit 20% of the demand to establish his bona-fides. This is as per Income Tax regulations. The amount can be even more if the relevant authority in the Income Tax Department is convinced that they have a strong case.

2 Likes

Latest Investor Presentation:

1 Like

@rupaniamit Thanks for clarification on the IT/ED issue. I have two specific queries which I would request you to put some light on:

1/ Given the tight lending/liquidity environment do you think the competitive intensity for KRBL will reduce? Most of the competitors are in high debt and banks are becoming strict in lending

2/ What is the worse case scenario for ED attachment of 15cr property? Will it have contagion impact on the business i.e. will ED attach more properties?

Thanks Much

My notes from Q1FY20 Earnings Concall. Please note that I may have misinterpreted some of the points shared by management so do your own diligence by going through the recorded call to verify my notes.

IT Issue:

- Have paid 115cr to IT so far under protest. Have submitted all documents and now waiting for the order. Hoping for 90-95% relief in appellate stage. Order can come-in any day and definitely order should come this month.

ED Issue:

- ED case is not sustainable. Attachment will go away. Matter of 3 months.

Exports:

- Iran imported 1.49mn MT this year compared to 0.7mn MT last year. KRBL has been capitalizing on this strong demand from Iran.

- Higher sales in Middle range segment (dubar & tibar kind of range). More export sales have been in middle segment.

- In year 2000 exports from India were 500k MT which has grown to 4.4mn MT in 2019. Two countries responsible are Iran (1.4mn MT, 33% of overall demand) and Iraq (350k MT). Hoping this global market to be 6-6.5mn MT. Growth of 6% every year.

- Iran consumes 3.2-3.3mn MT. At some time they were growing 2.5mn MT and then they were importing 500k MT from 3-4 countries like Pak, Thailand, etc. As time has passed, Iran imported first time in 2007 from India. From 2007-2019, now they are now importing about 1.4mn MT from India.

- CMD sees Iran importing about 2.2mn MT because of urbanization in Iran. And till sanctions are there, India is going to be biggest gainer.

- Have to be aggressive in medium segment to Iran , Iraq to clock 10% growth.

Domestic & General:

-

See strong demand of basmati rice.

-

Spent 2% of sales on promotional activities.

-

Debtors – 397cr

-

Net Debt – 280cr as on date. Expecting to be 0 by month end (August).

-

In domestic KRBL would have done much better, if Indian public was better aware of basmati rice. In next 4-5 years hoping for public to be better educative of what is real basmati rice is.

-

Paddy Stock – 222685MT at 34.4

-

Rice Stock – 325315MT at 49.577

-

Premium (classic range) volume growing at 5-6%. 23-24% EBITDA in premium segment.

-

Basmati needs 40-45% less water compared to non-basmati long grain. Non-basmati is sown in end of May-early June, and monsoon starts from June. Basmati is sown in mid of June and will be sown till mid of August. And that is peak monsoon period. Farmers have shifted to basmati this season. CMD’s guess is that 10% of farmers will shift from Parmal to Basmati rice. Real shifting figures will come by end of August. Expecting bumper crop this year.

-

3 new varieties of basmati; expecting 100k ton of new varieties. 1738, 1689, and one more. Commercial result will be known this year. Yield per acre is more by 20% in these varieties. Just 90 days of crop days and need less water. And big things are these are pest resistant. Will not require any pesticide.

-

In next 3 months KRBL going to offload about minimum 100k MT of rice. Whatever inventory we were holding by end of June 2019, it will be less by 100-125k MT. 60kMT will go in exports. 50k MT in domestic. As of 30th Sep KRBL will have debt free status.

-

Classic grew by 15% in domestic.

-

Nothing is going to influence farmer to sow a particular seed (maize, basmati, non-basmati, sugarcane, etc.). It all depends on how much money would farmer had made in a particular crop last year.

9 Likes

Hi @fundoo ,

I believe competitive intensity from organised competitors should at least not increase (and may reduce) in future given current market conditions. With tightening liquidity, borrowing rates are going to go up for players with stretched balance-sheet. And players like LT Foods have terrible margins compared to KRBL. KRBL management has guided bumper crop in upcoming season. So that means lower paddy prices and lower basmati prices. So LT Foods and other’s margins & balance-sheet should see more pain. I feel current industry developments in organized world augurs well for brighter KRBL future.

I don’t expect any reduced competition from unorganized players. Since they don’t age and simply sell basmati as commodity at lowest possible rate. They keep prices lower and hurt organized players. This will continue even under current tight liquidity scenario.

Good question. I’m not a legal expert. But have a feeling that the max amount at question is 15cr. If it was more, ED would have attached more properties of KRBL. But I would let legal SME opine on this.

3 Likes

i believe ED process will have 2 angles

- Qunatitative Loss - It may be restricted to the actual amount of proceeds of crime involved which is Rs.15 cr in present case.

- Criminal Action - Can anyone throw some light on what could be the Criminal repercussions and likely impact?

Hi

I was just going through KRBL AR 2019 and found below items under Investment Cash Flow statement.

Sale proceeds from investments 58,072

Purchase of investments (57,649)

But not seeing any investment item under Current or Non-Current Asset in Balance Sheet.

Can someone please help me with this query?

Thanks in advance.

ED has not invested in the company:-)

They have locked some of the shares because on going Balsharaf - AugustaWestland money laundering case…

ED has some evidance that this shares purchased with that bribe money…

1 Like