Yes, ideally he has to. But he will have to pay the original price, otherwise the Saudi investors will be at a loss.

But if he does, he will be in a severe loss.

Interestingly, the court has allowed the investors to sue the ED for damages caused. So, we’ll have to wait and see how this unfolds.

This is a lesson in many ways. A lesson about tailing famous investors, a lesson about not giving into the market’s mood swings and most importantly, a lesson about a good investment always coming with a certain amount of discomfort.

As I’d expressed in my blog post long back, I think KRBL is a good buy at sub-₹315 levels. I still stand by the statement, despite all the criticism I faced back then.

As per court order ED had released the blocked funds of pabrai after one month from the date it had asked exchange to not complete the transaction… So Pabrai was already free and lucky… Source _twitter posts

Any transaction by balsharaf now will only take place as per prevailing Mkt …also ED can appeal the court order

Yesterday, In interview with CNBC TV18 Mr. Anil Mittal (CMD) was sounding very bullish… Looks like KRBL will gain its glory back after the judgement of HC (Major overhang on the stock)

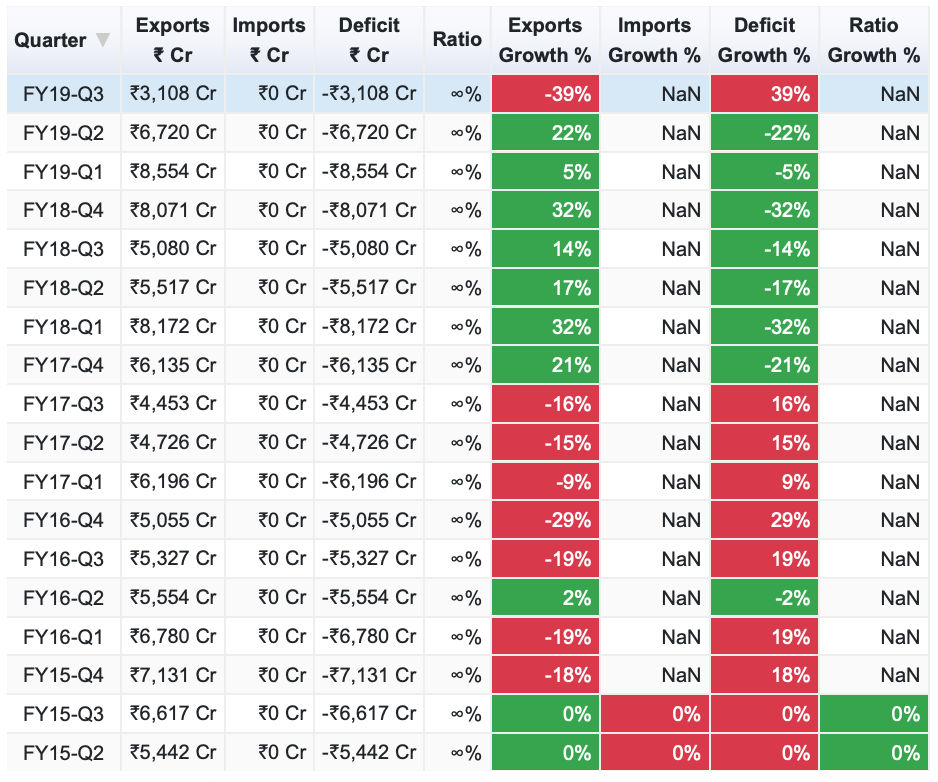

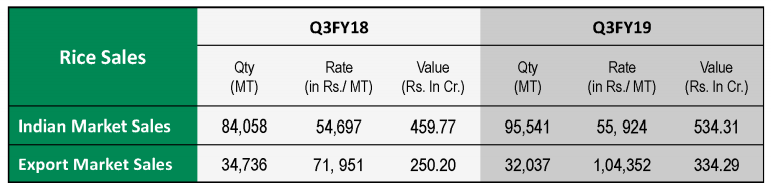

Ref. to data from @phreakv6 's website. Seems like multiyear low for basmati exports in the last quarter.

Am I interpreting the data correctly?

If yes, any reason for the massive down trend ?

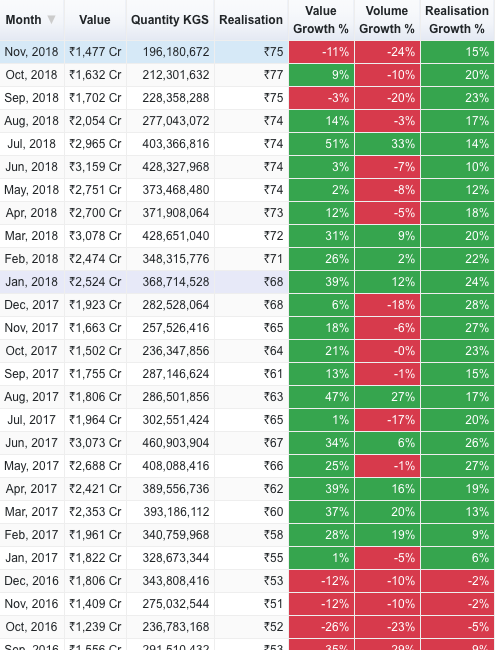

@dipen01 - Q3 data is not yet complete so please refer to the monthly. It is not as bad but though there is growth in realisations, volumes have been shrinking.

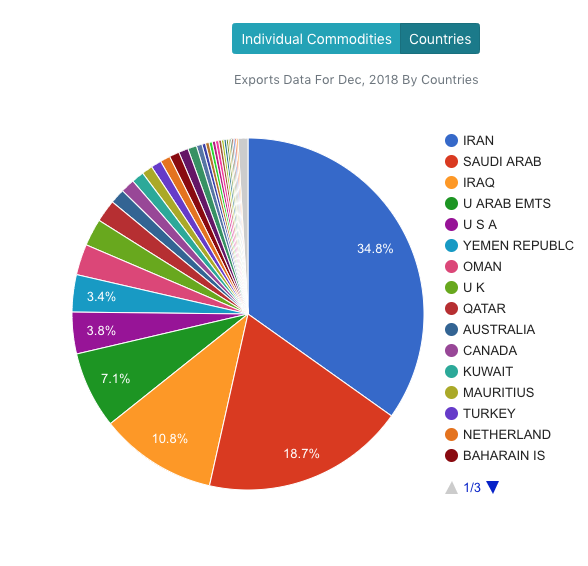

Iran ban would have been in effect during the past several months. It was lifted sometime in Dec 2018. That could explain the drop in export figures. Iran is the world’s biggest consumer of basmati and has the greatest share of imports. I could be wrong, but just trying to back trace.

A quick search on Iran in this thread, calls out <3% of exports to Iran by KRBL.I remember reading that same or even lesser was applicable to Chaman Lal Setia. There might be other countries that are witnessing slowdown in volumes

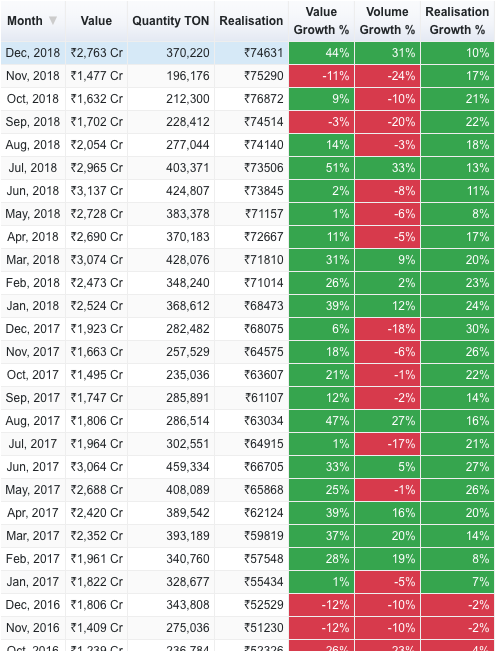

I have updated principal commodity data for Dec-2018. This for basmati rice corresponds to individual commodity data as is, so it can be used for comparison.

Decent Quarter. 9M numbers looking good. Management started giving realization numbers in Corp Presentation which is great. Good to see increase in volume for domestic market by 14% and increase in realization for exports by almost 45%.Strong inventory position at 3364cr compared to 2712cr same quarter last year. Investor’s should carefully read note #4 to financial statements pasted below.

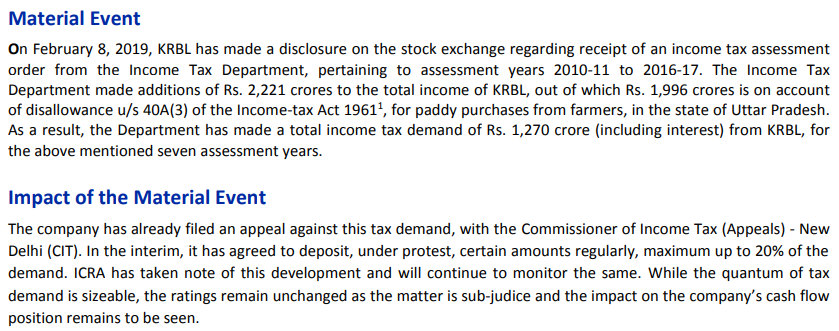

I just did a quick calculation - PBT from FY10 to current is 2891 Cr and in the same period they have paid a tax of 675 Cr (from cash flow statement) which works out to 23%.

A demand of 757 Cr makes no sense. But the IT dept is making this claim after raids and assessment so this is backed by something strong. The IT dept is claiming an additional income of 2220 Cr which implies a massive underreporting of numbers. This is damning on two fronts - A claim of 1268 Cr of tax + interest can sink the company if upheld. If the IT dept’s assessment is in fact right, what happened to this 2220 Cr? Has the management siphoned this money off?

Lower tax rate because it invested in energy business to take advantage of MAT. I have a feeling this claim by IT department is because of their business in energy segment. Hope BTV host asks management about this in interview on Monday so that management can share more details.

Hi @phreakv6 thanks a lot for the brilliant analysis on this sector but my experience is Market never going to give a premium value to a stock whose management is having some integrity or corporate governance issue.

So I think we should discuss other stocks in the same area like LT foods or chaman lal setia who has also suffered the industry down cycle. Not sure if we are already having a separate thread for them if not we can initiate one as well.

The video is available now on YouTube. Was impressed to see the level of technology they have adopted to ensure best quality rice is delivered to the consumer and how quality obsessed they are. The video also provides a glimpse of the next generation team that is gearing up to take on the responsibility from the legendary founders.