Zero mutual fund holding. Quite puzzling considering it is a well known business. What are they seeing that we are not?

Note: I don’t believe MF participation is a high quality yardstick to measure business quality; we know how many MFs participated in Avanti since last 4-5 years.

One reason which I can think is there is not much available in market to buy 100 entities hold 91%. And probably this is the reason that Pabrai paid top price as you can buy material quantity only in one to one transaction.

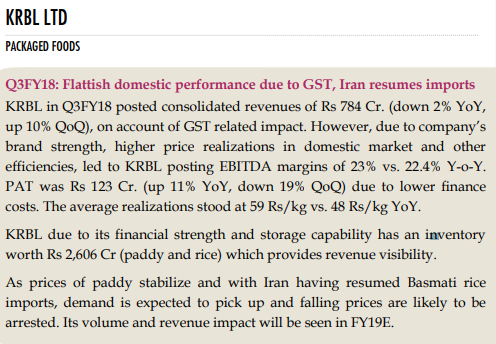

The key to higher OPM is the strength in sourcing, availability of cash and capital management for inventory, deep relationships in the sourcing ecosystem and early input framework on market disruptions.

Invested in KRBL for many years and will see it grow for many more. Having a known a lot about KRBL and Basmati sector, i must say that there was a lot i could learn more from some of the inputs shared here

Logic tells me that the clinical numbers especially on revenue-topline in the past few quarters is a indicator of inventory build up for higher realizations as well as holding to the premiums when markets were over competitive.

As the effects of demonetization, GST and now operational/banking challenges in Imports/exports stacking up and contributing to sustainable higher prices which will work against the unorganized segment the macro tailwinds for KRBL are gathering speed.

I was reading KRBL’s annual report. They claim to be the largest rice millers in the world. However, there’s an American cooperative called Riceland that also stakes a claim to that honour. A quick search reveals that Riceland is a major food company in the US. Could anyone guide what the correct position is?

I’m sharing my experience pertaining to rice consumption. If it isn’t value additive, please guide me.

I belong to a West Indian family. My entire life, until recently we’ve eaten Surti Kolam variety of rice. Consumption of Basmati rice was restricted to restaurant visits. I must say I enjoyed eating Basmati. My meals were dominated by Rotis instead of Rice. But, one fine day, I switched to just rice, Basmati rice to be precise.I eat approximately 400 grams of Basmati rice everyday. The rice is from Dmart. And, i must say i have a high opinion of it.The sole motivation behind my rice brand choice was price. There were multiple brands but my decision was based solely on the price. I belong to a typical Indian middle class family. Hence, the Basmati rice consumption may increase. But, even today, despite the tremendous growth in our economy and elevation of millions from poverty to the middle class most people decide on the basis of price rather than brand. The possible reason could be that the significant price differential may not be worth the increment in happiness, joy derived from the food.

Fully agree. People from West Bengal love to take another form of Aroma Rice, we called it ‘Gobindo Bhog’. Little expensive that normal rice. We use it for Pulao and Biriyani etc. So I am little doubtful of mass migration theory of Unorganized to Organized.

You have to understand, farmers will continue to sow these local high quality rice. No GST can prevent them from sowing it.

Going through above discussions, I understand that basmati can be grown only in some regions. In that case there can’t be much growth in supply. So long term growth for KRBL should come mainly due to price increases. But I don’t think prices will increase beyond some extend due to substitution effect. If the relative price of basmati is so high compared to other varieties, many people would shift to other varieties. So in my opinion, we should not expect very high growth rates. I would expect a growth rate of 10% CAGR max. for next 10 years.

A test in which the person sampling is not aware of what they are sampling.

For eg. in the case of basmati rice, they do not know which brand of basmati rice they are eating. This way you can check if the person can identify the brand by taste alone rather than by seeing the packet.

This is my understanding of a blind test, please correct me if I’m wrong.

For the Cash Amount, I honestly don’t remember now. I made a quick valuation because someone asked me to. Look at their Current Assets and make a judgement call on what looks like it could be converted into Cash immediately. That’s the figure you should use.

Again, the denominator in the Capital Turnover figure contains Cash. So that might have caused the difference. In the excel, if you input the amounts, Capital Turnover will be automatically calculated for the Base Year (Under Assumptions). You can then make a judgment call on whether you think that Capital Turnover looks reasonable. I calculate the Capital Turnover across 7-8 years and see if the Base Year figure makes sense. If not, I take an average (3 or 5 years), excluding extraordinary figures (Like I mentioned, extraordinary figures can come because of a sudden jump in cash holdings).

ITC enters Rice segment - Gives me more CONFIDENCE on KRBL - ITC entering the market means

Overall market set to grow rapidly and chnage in cinsumption patterns towards premium rice.

Higher prices and Higher margins are sustainable.

ITC would have conducted a detailed long term market study and hence this Industry is now just about in the beginning of becoming a mature corporate Industry segment

Its moving from unorganized to organized rapidly triggered by demonetization, GST, brand awareness, Super market formats…etc…

ITC will spend money to create new segments as well as exoand existing markets…a big benefit for all participants.

Blind tests are typically carried out amongst your most loyal customers who are passionate about your products to see whether they can identify your brand ( after consuming it - for e.g Consuming Lays Cheese & Onion v/s a similarly flavored one from Balaji ) from amongst other unbranded ones or other brands without knowing which is which beforehand. We test the consumption experience and strip away the imagery. Products are consumed via different senses and what constitutes consumption is in itself a challenge sometimes.

After the test results are revealed to them likelihood scores are taken to see whether their preferences change pre and post. It is interesting to see the impact on preferences once they realize that they are unable to identify the brand they deeply care about from an unbranded one. In the tests that i have been associated with these preferences diminish significantly indicating that even the most brand conscious customers can be made to change their choices if they realize that the extra money they are paying is for imagery and general product narrative. Indians may be brand conscious but they are a rational lot.

The broad conclusion is that brands that are built on imagery are difficult to sustain and the scores indicate that they can be made to switch.

Not saying that that is applicable to krbl and its margins are unusually high to be simply a product of imagery. But its true in many cases.

You cannot build a brand on imagery or product alone. both go hand in hand. one without the other is incomplete as far as building a good brand goes. creating a brand with a poor product and only the ads and messaging around it will never find any takers. on the other hand having great product without anyone

Blind tests are good tools, but unless every consumer is being taken thru it and as a result realizing that there isn’t a discernible diff in the product, the conclusion you have drawn will probably not be true.

A blind taste test is often used as a tool for companies to compare their brand to another brand, not necessarily to send a message to consumers.

A couple of years ago we were doing a series of blind tests for pidilite amongst Carpenters. Carpenters were asked to use 7 adhesives one of which was fevicol and ofc they didnt know which is which. The sample size was 150. Of the 150, 141 were able to identify fevicol correctly. There were no other imagery cues just plain use experience. Some of them didnt even have to use it, they just eyeballed it. Thats a strong brand advantage to have.

Users of krbl branded basmati rice should be able to identify it after using it from amongst other ones because of many things krbl does like ageing it properly.

While not a blind test the following test report gives good insights on the quality attributes of the several brands tested, i am guessing sometime in March 2016 post GI tag approval for basmati. One can clearly see that India Gate while good is not the best. There are other rice brands that score above India Gate and are priced lower. The Sensory Panel results are also interesting.

It largely depends on what a brand stands for. Me and a group of other fellow investors were having a discussion around Maruti a few days back brainstorming on what makes Maruti retain its leadership year after year. It evolved into an open ended discussion and we could not conclude on anything except we all agreed that we need to find out if the brand Maruti represents superior cars or is it all the other attributes ( trust, reliability, availability, etc ). I would wager that its the latter. Now, lets see if we could have a blind test for cars. Obviously since the car’s external looks would give it away, what if we had someone like Renault build a replica of any one of Maruti’s models and have Maruti customers drive both vehicles. I would guess that most customers would just take a blind shot.

Even as far as Fevicol is concerned, i dont think its impossible to develop an adhesive that would be as good as Fevicol or even superior to it. What may be incredibly difficult to do is to build the trust in the minds of the customer. We did have Blue Coat a few years back that was considered to be superior to Fevicol but then Pidilite just bought it out.

The point being - if the brand or the competitive edge is just the technicalities of the product ( taste in the case of food products ), its not that difficult for a competitor to take away that edge. But if the brand represents a whole lot of other attributes, it then gets incredibly difficult for new entrants to dislodge the incumbent.