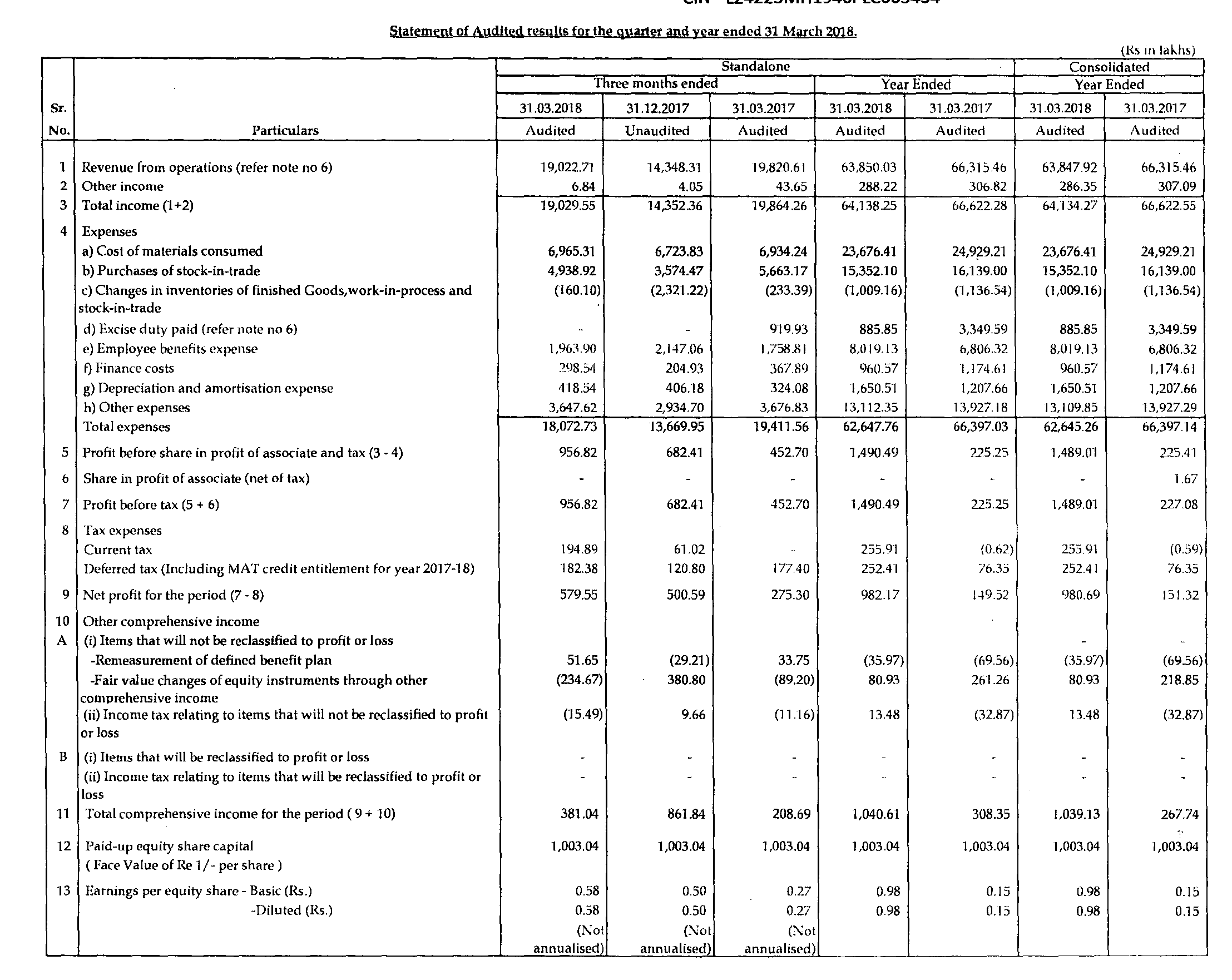

KOKUYO CAMLIN LTD. has reported financial results for the period ended March 31, 2018.The company has reported net sales of Rs.190.29 crores during the period ended March 31, 2018 as compared to Rs.198.64 crores during the period ended March 31, 2017.The company has posted net profit of Rs.5.79 crores for the period ended March 31, 2018 as against Rs.2.75 crores for the period ended March 31, 2017.The company has reported EPS of Rs.0.58 for the period ended March 31, 2018 as compared to Rs.0.27 for the period ended March 31, 2017.The company has reported net sales of Rs.641.34 crores during the 12 months period ended March 31, 2018 as compared to Rs.666.22 crores during the 12 months period ended March 31, 2017.The company has posted net profit of Rs.9.80 crores for the 12 months period ended March 31, 2018 as against Rs.1.51 crores for the 12 months period ended March 31, 2017.The company has reported EPS of Rs.0.98 for the 12 months period ended March 31, 2018 as compared to Rs.0.15 for the 12 months period ended March 31, 2017.

1 Like