Kokuyo Camlin has more than 80 years operating history in Indian educational stationeries with well recognized brand recall in the segment. In 2011, it is acquired by a leading Japanese stationery player Kokuyo by paying almost double the price of current market price. Promoters holding in the company is about 74%. Considering huge untapped opportunities in india school education system and migration of education stationery segment from unorganized to organized category can offer required trigger for the company. According to some studies in? he categories in which call in is active current market size is about 12000 car and expected to grow in double digits in next few years. More research is required to explore this in detail but from macro level it looks interesting.

Some cons

(1) Cheap Chinese import in this category is putting pressure on the margin

(2) Considering immense potential in the sector many global companies including Faber etc is already active in market

(3) Record of japanes promoters in running Indian companies is not satisfactory due to cultural differences unless Indian partner is in majority. View invited.

Manish i dont think there is any violation in discussing this stock idea. Can you please be more specific about the violation? I can see so many new stock ideas discussed in valuepickr forum.

“Only Caveat isif you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.”

You have posted a broad view. At least put some figures.

Yeah myself doing some more studies on this idea and update with details. Meanwhile i just posted this to get views from more experienced members. My small experience in stock market suggest that companies with inherent latent demand has better chance of outperforming than companies which already showing high level of growth and quoting at expensive valuation. Also i am interested to know how much effect blogs, forums or a famous investors etc has on share price of a particular stocks in short term. Take example of Gati , it was quoting at very resonable valuations , there is nothing to speak about current financials but mere announcement of buy by a famous investor made this stock move almost 3 times. Thanks for your suggestions.

We here at VP encourage new talents but caveat is that he should be putting his efforts in researching the stock not merely putting his few liners thought and ask the seniors to take over. At least put some efforts, get the financial details, balance sheet details of the past and put them. That will help the others to understand the company and then you will get many helping hands. If you put little efforts then nobody would be willing to put their heads into. Hope you got the point.

I was interested in Kokuyo camlin due to Camlin brand. Many of the stuff which i buy for my kid’s stationary is from Camlin brand. But it seems the company is having a tough time.

-Historically the net profit margins have been very low.

)- The stock is still not cheap. It operates in a highly competitive environment and as seen from financials has very low margins. I am not very sure if they have pricing power.

The Mcap to sales ratio is 0.8 and doesn’t seem undervalued to me.

ASSUMPTION - Mar 13 sales was 435 cr. If I assume that sales will increase at 10 % every year and company will have NPM of 5 %. After 3 years sales - abt 575 cr, NP abt 30 cr. PE of 10 will give Mcap of 300 cr ?? At present price what is left for a conservative investor.

The company can perform better if they are doing something which can lead to higher sales and higher margins but then what is it ??

The Kokuyo took over in 2011 and i remember reading from AR that they are increasing sales / marketing team etc but then it has not NOT translated into higher sales so far.

)- the promoters had infused equity in the past and had to go for rights issue recently which increased outstanding shares from 6.9 cr to 10 cr and company recd bat 100 cr from the issue. Now my question if the business is doing well what was the need for rights issue ??

Also due to higher equity base the EPS will be lower.

The rights issue was to fund the capex (new manufacturing plant) over the 3 years period. This new capacity will come on stream around mid 2016. Until then I don’t think there are any stock specific triggers. I own a small stake in this bought 2 months ago around 30/- per share. I would like to watch out for the brand strategy going forward and the kind of scale up possibility from this new plant before taking a fresh call.

**The company held its AGM on 17thJuly’14 and was addressed by Mr. Dilip Dandekar Chairman and Executive Director .**Key Highlights by Capital Mkt;

In FY’13, the company reported losses at bottom line due to higher operating costs and higher competition resulting in company unable to increase prices. Although costs cutting measures were undertaken, higher competition and adverse market conditions affected the bottom line.

As per the management the year 2014-15 will be more of a transition year. It will be a year of increasing spend and focus on R&D, building capability and work toward synchronizing the capacities.

Currently, the company has 5 manufacturing locations spread across Maharashtra. The company will integrate the manufacturing and assembling capacity under one roof in MIDC and the plant will get commissioned from early 2016 onward. This will help in better economies of scale and cost reduction.

As per the management, the synergy of the acquisition has already started in terms of leveraging upon Camlin’s products and kokuyoâs products and geographies and markets. Kokuyo notebooks are already launched in Indian market and management is leveraging the existing brands and distribution network of Camlin.

Management believes while the synergy has already started the full effect of the same will be visible in next couple of years.

Latest annual report mentions about new integrated factory to start production in Q2 of FY 2016-17.

This is big positive for the company. Going through annual report I see following are the key factors that will drive the growth for the company.

Consolidating production at new factory will enhance the cost advantage.

Strong Camlin and Kokuyo brands will help online sales for the company. With significant spending in education sector, Strong brand will help in organised sector to capture the incremental sales.

Parent Kokuyo will play important role in introducing new products in Indian market.

I can see company will increase the sales as will as margin going forward.

Anybody know how much the notebooks contribute to the annual revenue of camlin? What is expected growth of this segment. I sent email to the management and did not get any response.

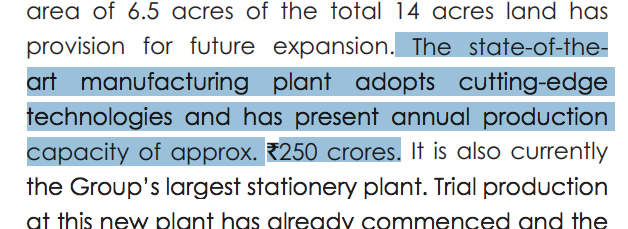

Patalganga Facility which is one of most advanced facility and largest plant of kokuyo int. has commenced operations which will bring synergies in operations… Seems there will be some triggers coming with respect to increase in margins.

Moreover this sector is highly unorganized hope that GST will help this company in gaining market share and thus increasing revenue and bottomline too.

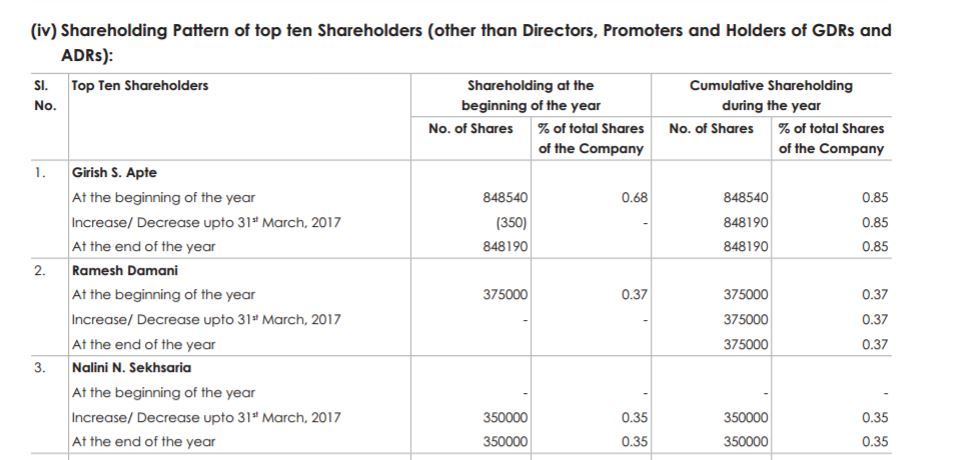

And also renowned investor Ramesh Damani holding 3,75,000 shares as per annual report.

Big improvement in EBITDA margins in a usual weak qtr for Kokuyo. Impact of the new plant? Few questions -

1.Will they still be operating all their old plants? Or they have shifted all operations to the new plant?

With the opening of the Patalganga Plant, Kokuyo Camlin has combined the production facilities that were distributed within Maharashtra, thereby creating a total production floor space that is twice in size when compared to combined floor space of existing factories. Kokuyo Camlin products having a Number One share in the Indian market such as markers, mechanical pencils, crayons etc. will now be manufactured here, which will strengthen the supply-chain infrastructure and enhance production efficiency. The plant has complete end-to-end production capability and this would result in a reduction in the production cost owing to reduced transportation cost and enhanced production efficiency. Furthermore, Kokuyo Camlin expects the reduction in logistics cost by a direct dispatch from the new factory to all over India.

2.What is the optimum utilization% for the new plant? What could be the revenue at peak utilizations?

3.Product mix also impacts their margin? Can these 8-9% margins be sustainable going forward? Can they even improve on this number?

4.Unorganized to organized shift has been the touted theme from last 2 qtrs. Is the shift really happening? Any signs on the ground?

Some back of the hand calculations (Assumptions - Rev growth in FY19~10%, EBITDA% ~9%).

650-700 cr revenue at 9% margins (best case margins?), gives ~55-63 cr EBITDA.

~16 cr depreciation (4 cr per qtr)

~8 cr interest outgo (2 cr per qtr)

~30% tax outgo

~20-25 cr PAT

Current valuation ~1400 cr (@139)

So currently trading at ~ 70x - 55x (1 year forward)

Now, key is how they improve their revenues as that would improve the situation in terms of valuation. I have already taken ~10% revenue growth for my calculation.

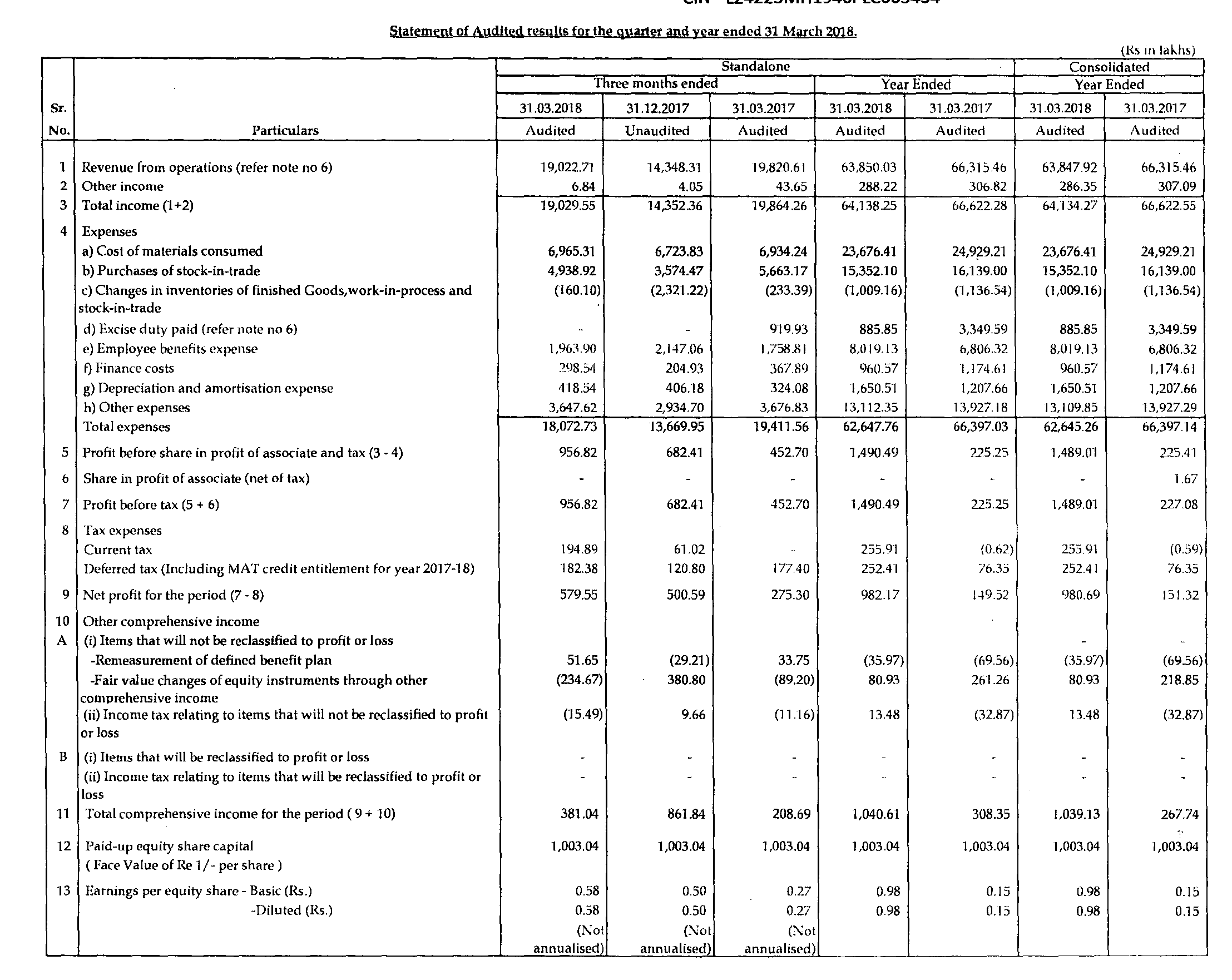

KOKUYO CAMLIN LTD. has reported financial results for the period ended March 31, 2018.The company has reported net sales of Rs.190.29 crores during the period ended March 31, 2018 as compared to Rs.198.64 crores during the period ended March 31, 2017.The company has posted net profit of Rs.5.79 crores for the period ended March 31, 2018 as against Rs.2.75 crores for the period ended March 31, 2017.The company has reported EPS of Rs.0.58 for the period ended March 31, 2018 as compared to Rs.0.27 for the period ended March 31, 2017.The company has reported net sales of Rs.641.34 crores during the 12 months period ended March 31, 2018 as compared to Rs.666.22 crores during the 12 months period ended March 31, 2017.The company has posted net profit of Rs.9.80 crores for the 12 months period ended March 31, 2018 as against Rs.1.51 crores for the 12 months period ended March 31, 2017.The company has reported EPS of Rs.0.98 for the 12 months period ended March 31, 2018 as compared to Rs.0.15 for the 12 months period ended March 31, 2017.

Looks like 250 Cr is peak. No idea about utilisations and product mix. Does this company have any concalls? I don’t see any announcements for concalls or even an Investor presentation.

Nope…no concalls. The thing is that even at 20 cr pat for fy19, at 100 thsi is trading at 50x. I am not sure why Kedia ji added this above 140. What are we missing? That is why i was looking at this company. May be utilization will improve resulting in them improving margins and topline. But cannot find much info on the same. Also, one should consider that base would be much higher next year.

People interested in this company may find some useful info in this analysis by Mr Singaraju.

Discl: I am not endorsing Mr Singaraju’s views on valuations. I find the stock expensive by 30-40% (Considering investors need to have decent Margin of safety) even at 1000 cr Market cap. Not invested.

How do you know at what price vijay kedia has added this?He generally buys a tracking position secretly and only increases his holding to 1 percent after the stock doubles.He bought sudarshan at 40 and only revealed when it hit 80.(Again may not be true always)

U r right…report came when his holding became over 1%, in jan this year. At that time price was hovering around 140. My bad. He could have added at lower levels before accumulating more. Thank for correcting. Though, point was valuation, which still holds.

For the benefit of the people, who are investing in Kokuyo Camlin based on Mr Vijay Kedia’s investment, the March 2018 Share Holding Pattern does not reflect his name (Dec 2017 SHP shows his stake as 1%). Seems he sold off his stake.

Apologies for this message (as this message is not in accordance with Forum guidelines).