Board Meeting Intimation for Results & Closure of Trading Window

16 Jan 2017

Board Meeting Intimation for Results & Closure of Trading Window Board Meeting Download PDF 11:18

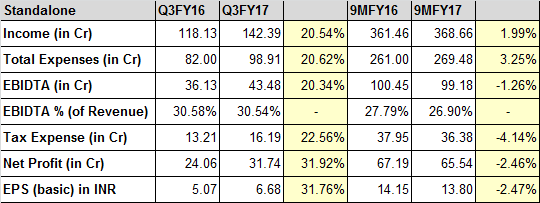

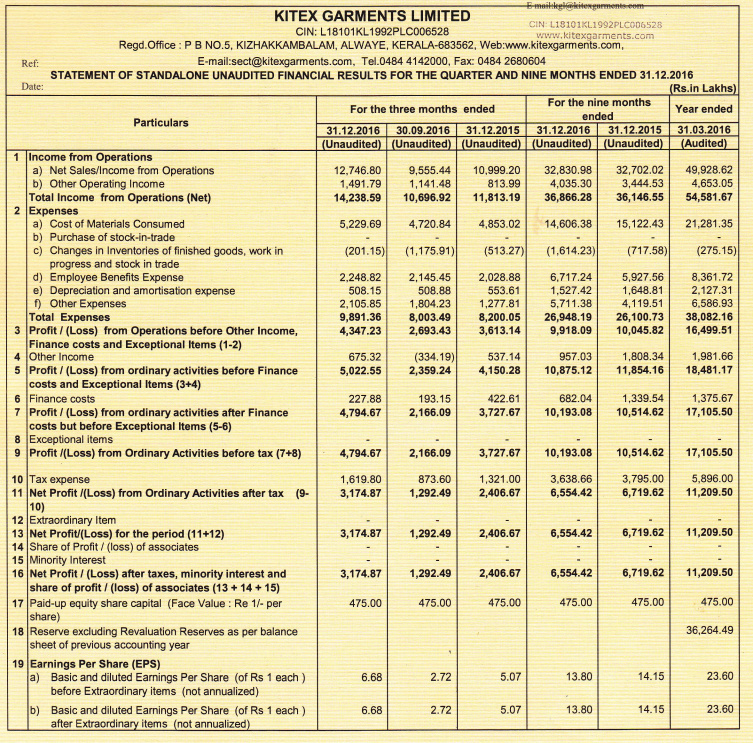

Kitex Garments Ltd has informed BSE that a meeting of the Board of Directors will be held on January 30, 2017, inter alia, to take on record the un-audited financial results of the Company for the 3rd Quarter and nine months ended December 31, 2016.

Valuequest India Moat Fund holds 10.52L shares (2.21%) as on 31Dec16 compared to 7.89L shares (1.65%) as on 30Sep16. At 400/sh, it amounts to approx 10cr additional investment.

So as per Prof SB, the pros outweights the cons discussed in the thread here. Either that, or the fund has received good amount of new investable funds (and still the prof may be seen as bullish, else he would have not done addtl allocation here)

I probably have authority bias but I view this as good sign.

Our one of a kind straight-talking, frank CEO who some would mistakenly term eccentric and over-optimistic. And some have even gone to the extent of politely advising him during concalls “not to give projections”

But can you really restrain so much energy, pride and confidence from being over-optimistic about future?

If you can keep your biases aside, you will enjoy listening to him just like you listen to an old song which refreshes your mood even with repeated lines

For others too he offers a good exercise in mental-models

But on a serious note, do we really have more like him in India

Expect 20million dollar revenue from Lamaze and Little Star in FY17-18

Debt is 4.51 crore (long term borrowing) and NIL (short term)

5-10% growth still expected in revenue for this year compared to last year.They expect 200+ cr sales in Q4FY17.

Cotton prices flat. Expect same range.

Jockey business : closed last year.

Capacity utilization 100%, plan to double capacity by 2020. 30-35% increase in capacity on average each year for next 3 years.

Adding one more block next year, mechanizing existing lines , daily adding capacity by fine tuning machines, resources

20-25cr capex for current year.

30-35 cr Capex for next 2 years each.

Kitex Childrenswear : Fy19-20 to be merged or listed.

Spent 1.5 million dollar on Lamaze and Litte Star till date

Looking for small brands in US having presence in certain regions. Before Q4 result they expect one more brand added.

Focus is to automate

Design Studio in US - buyers can come there and see the designs. This studio is needed for Lamaze and Little Star but additionally using this for existing business. Gives them an added advantage and gives customers some cost benefits.

Ayush can be tough in asking about 240crs cash and yet paying 8 crs interest but Kitex is equally clever in ducking the question.

clearly lamaze concept is not working I. e. organic baby clothing . That’s why none of larger players focused on it. good thing Kitex probably knows this hence looking at other way.

customers dictate pricing and do nt pay penny for your fancy offices n factory. This means no MOAT . All fancy thing s should result in kitex being lowest cost producer and result in better margins.

volume growth is very low in last two year s. intact this qtr was suprise to see kitex salea increasing .Hope they have not pushed inventory to US entity . No listed entity will take delivery in last quarter unless it is gerber who took late delivery of Q2 sales in Sept.

5.they are planning one more acquisition probably small brand

Jay Jay clear competition. although he says no one is real competition but he forgets it is commodity services business.

5.it is good strategy to go up value chain else no more margin expansion.

not sure why they stopped giving volume number from 2012 .USD appreciation and cotto price droo has played good role in sales and profit growth.sewing is major part of manual service difficult to tackle as well

KCL KGL story wi remail supense best we can expect 50:50 merger that’s the best

One thing I noticed is that in this quarter result they did not publish the balance sheet, which they did during Q2. I wanted to know the performance of US business and inventory build up, receivables and cash.

I listened to the con call. The management is very bullish about the future. He told nobody can compete with kitex. Is this the moat here?

There was a question on capacity utilization. He told the current utilization is 100%. And they are adding new capacity daily. Can someone explain how this is possible? Any other listed company that expands capacity every day?

He is using KCL for capacity …right hand and left hand on his wish do the Majic. Go thriugh realted part transactions you will understand. There is excess capacity available in KCL.

Sabu’s interesting take on trump policies affecting the company. He also mentions about the cost advantage and scale of his operations. We may have to take Sabu’s confidence with a pinch of salt as he is known to fall short of his promise!!

It happens in all business. As an investor more important, is he sticking to his commitment of 200 crs in Q4

Remember INFY voluntarily gave up GE business which in 1997 was 25% of its turnover. .

Hi Donald from the MCA filings i could not comprehend sabu salary. He is charging KGL 4crs . Do you know salary he is charging for KCL. I saw zero so was bit suprised.

Well in my view, mr.Jacob is specialised in infant wear under 2 years and he uses cotton and organic for these clothing wears.the fibres are developed in house. Jockey though was a good client but wanted more of synthetic cloths for adults I believe. So here was a dilemma. To leave the focus and long term goal on scaling in a specialised infant wear segment or to diversify into synthetics with significantly more investment and loosing focus.

In my view Mr. Jacob took the right decision and took a hit and exited the segment completely for a short term pain and long term gain. He now focuses on scaling his business and improving the margins further by forward integration of selling the infant wear himself and thorough Lamaze.

I am yet to see how well this forward integration works out.

Disc: Not invested but being curious and keeping an eye.

According to un-audited results, during FY2016, KCL reported a net profit of Rs. 28.3 crore on an operating income of Rs. 205.4 crore as against a net profit of Rs. 19.0 crore on an operating income of Rs. 204.2 crore during FY2015