Lamaze: Sales less than 100 thousand dollar, Already selling to target, buybackbaby

target getting 4th order.

9-10 customers showed interest in Expo. Expect Huge orders in feb-march

Guidance of 20$ mln sales next year : For Little star & Lamaze

Debt: Rs 4 .15 crores long term

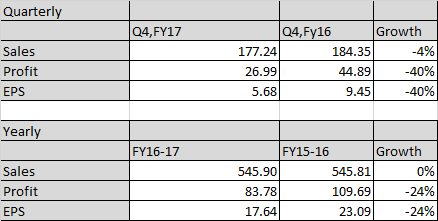

Expectation for Q4 : Rs 200+ cr expected in Q4 ,

Overall, Revenue might increase 5-10 pc YOY. Guidance was for 20 pc but impacted due to US Elections.

Hope next year guidance is not impacted by Border Adjustment Tax @US

Not much effect seen from Tax implication in US as for eg:

Take body suit which account for 40pc of sales,

basic cost is 70 cents and they sell @ 2dollars

cotton price : expect similar price

other operating income: ROSL, MIS .

Lamaze margin expect 15-20 pc of sales,

Expect more brand tieups soon

Customer Outlook:

Carter sales 1.8 bln in fob , kitex supplies less than 1pc

Kitex sales to Carter at 5mln dollars,committed 4-5 times

Gerber buys 15 pc buying from kitex

Sams club second order huge

Investment: Rs 17 cr investment in effluent treatment plan will increase debt but 25% TUFS scheme subsidy

While Sabu is exaggerating it a bit, I believe that garmenting is one business where you can add capacity very fast. It is among the most labour intensive businesses and least capital intensive one. You just need a few sewing machines, skilled labour, and a basic factory set-up to expand capacity. I feel what he meant by ‘adding capacity daily’ is that he might have some extra space where he has moved more machines and workers.

WC is increasing more wrt total assets and sales for last 5 years.

Sales is also decreasing comparatively with respect to the invested capital for last 5 years but its fixed assets is providing more sales than earlier. So other assets are increasing and not contributing to sales and earnings.

Increase in sales = Increase in receivables=> increase in WC.

Decreasing dividend payout for last few years.

I think the company is adding on assets, investing at KCL although sales is suffering. Increase in sales is mainly due to pushing products and mercy of raw material prices but it has been able to maintain and improve its margins->earnings well for last 5 years which is driving its returns and ratios.

Please correct me for any mistakes. Provide your views on point 2 and point 3.

I checked the CRILC report which is reported by all banks for the Sep quarter as well as the Dec quarter 2016.

Sep quarter showed a cash balance of INR 201 Crs but the Dec quarter just showed INR 1 Crs.

My view:

The company has cash in its kitty. So, cash is real but the problem is where is it deploying that cash since it is not keeping in its Current Account.

It is just keeping the cash in its current account at half year and year end to report it in the balance sheet and that might be the reason for so less interest being received for that cash.

What if this cash is loaned off the records for a very short term by a shadow party with vested interest who benefits from showing bloated cash in balance sheet? One of the private investment funds could be the shadow party.

Since the new auditor has come in (auditor change), the results have been reasonably similar to when other companies have declared. Honestly, there was nothing to boast about (by company) being the first one to declare results. Neither do I think there is too much to read, that the results are now declared later, than earlier.

One other advantage - bonus stripping (the loss incurred after selling a stock once it turns ex-bonus can be used to set off against short term capital gains) - was mentioned by someone here. You can find the gist of it here:

Hi Sowmay,

Invested in this few months back but after going through various posts by senior members, found that Mr Sabu doesn’t walk the talk… there was an issue with parking cash (if remembering correctly) while not attending debt. He is found to be glorifying the business and wanted to remain in talks… This is where a small investor start needs to take due care.

Biggest problem 240 cr cash , he had said dont require much capital to grow to double revenues , now he is going ahead and spending huge 250 cr to expand capacity in automation etc . Suspicion is becoming stronger that this money does not exist. . i also want to understand how much money he charges KCL in terms of salary.

how is investing free cash flow linked to raising capital? if the business has to grow and its operating at 90-100% capacity, he needs to 1. increase prodcution efficiency OR 2. increase prices OR 3. invest in increasing production capacity which the promoter seems to be doing. I think there are 2 key issues which needs to be analysed in details: 1. mgmt has been much higher guidance than the ground realities of the business 2. need to analyse reason for lower sales and see if business model getting impacted

This is one company i have followed from a business, technical and capital structure point of view. Obviously when the professor is involved in the stock, it draws attention like it should.

From an educational “vantage point” - This is a great learning opportunity

There are three questions - i invite comments from all at VP. I believe that it may lead to a pattern which may lead to a mental model that will help us all in the future investing activities

Q1 - Is the cash real? ( business point of view) Q2 - Should or should not - a company issue bonus shares in times of a crash in the prices of the stock? ( capital structure point of view) Q3 - is the fall in stock prices a price correction or a time correction? ( technical point of view)

When looking at kitex i always struggle with these questions. I am unable to answer them perhaps the folks here can throw some light and create a unique case study from this unique situation.

Dear seniors - can you use kitex as a case study to illustrate some important points about investing? i personally would look forward to your inputs so that it benefits all here.

Pls note - Kitex may well may be a great business. But since many of the common questions we sonetimes face in our investment process have cropped up in the kitex situation i am using it simply as an example. Strictly an educational endeavour.

In 2015, Sabu formed another company called " Kitex Infantsware Ltd." which is in the same business as of Kitex Garments. Its neither a subsidiary nor associate company. I don’t know what might be the intention here.

It formed an LLC to sell directly through E-Comm @ USA but 50% of that share holding is with KCL and other 50% with KGL. The average price at which Kitex sells the garment to retialers in USA are 45-135/- per pc. By direct selling under their own brand, it will surely going to hit the big profit but I really doubt if the full benefit will be transferred to KGL. The formation of new company and splitting the share of LLC @ USA, it certainly raises the red flag.

I might be completely wrong here doubting the intention and corp. governance of KGL but their record is not spotless.