can someone please explain current qtr results, what is the extra ordinary loss for?

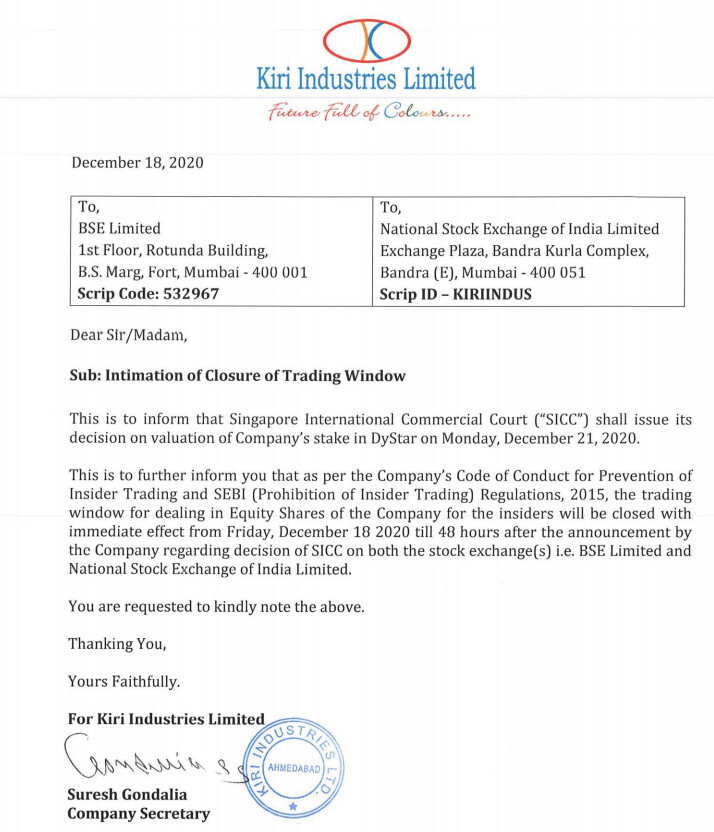

SICC verdict dated 03/12

And BSE intimation:

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=5b40bd05-3c53-402b-9acf-f83e443375d8

1 Like

Good development overall although court has conceded that some minority discount may be applied upon valuation.

This perhaps explains why there’s was anticipatory price recovery n Kiri stock past week.

Any idea on timelines of by when once can anticipate the stake buyout by Senda hapoening?

why did Kiri incur a net loss in q3 after showing a reasonable PBT , can someone please explain thanks

Anyone has any update on the status of Singapore court case? Manish Kiri mentioned he believed it would wrap up by end of May, however there does not seem to be any judgement in sight.

Update on Dystar litigation. Senda claims dismissed.

Court has now ordered parties to submit valuations.

PS: Kiri might also be charged for some amount for claims against KIRI and Manish Kiri in respect of Kiri’s offer and/or sale of products to DyStar customers in Sri Lanka and Japan.

Dystar Valuation coming up in August. The long term fate of this stock hangs in the hands of the promoter - if they distributes a fair chunk of the proceeds to retailers.

Otherwise, the business itself is the lower end of the spectrum and a commodity trading business does not deserve a high PE. Stil, going forward as the sum of parts valuation of dystar does see Kiri gong to higher levels from here.

Disc - Invested

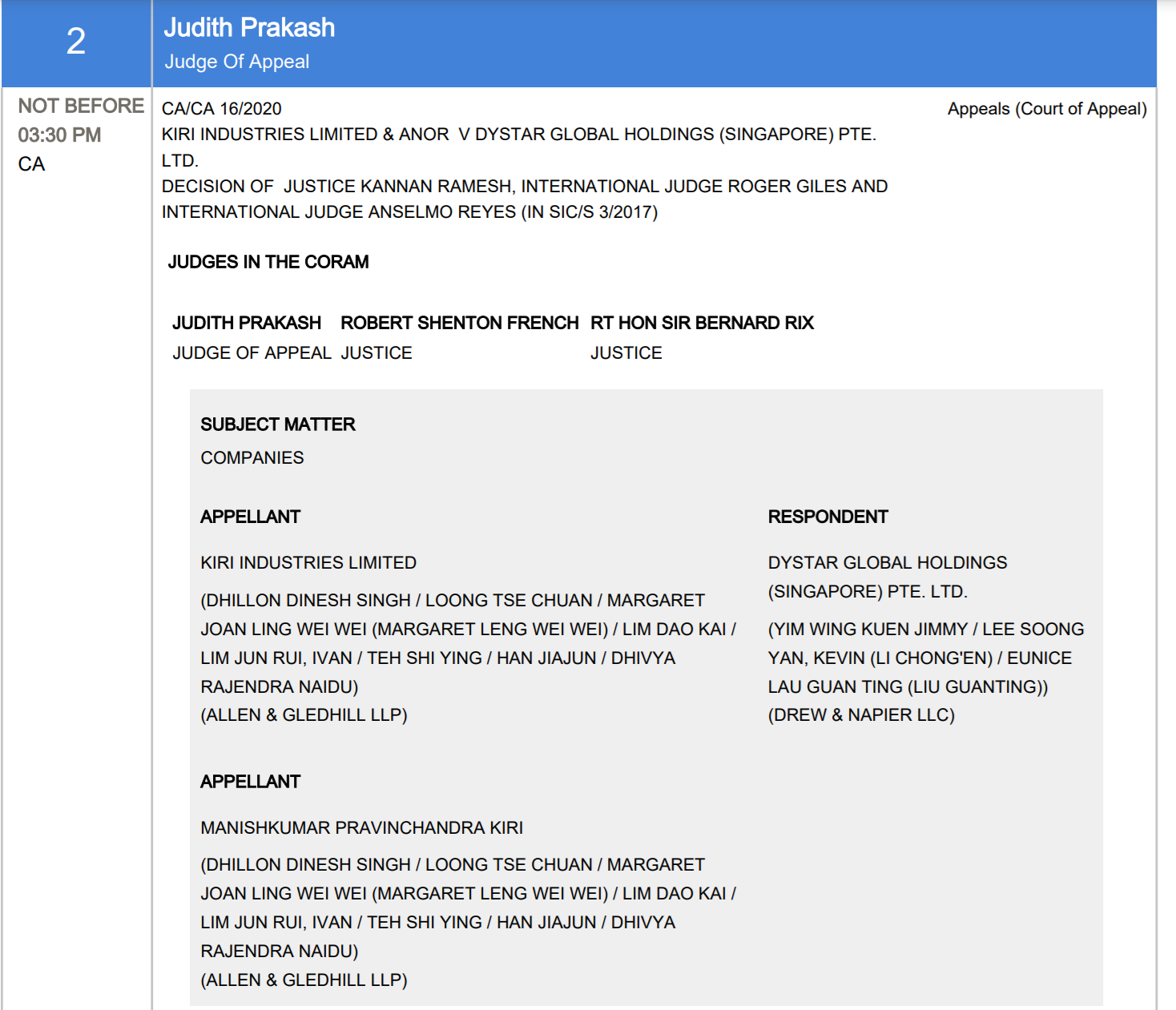

Looks like court decision in Kiri’s favor. Should be very positive for Kiri. Summary of judegement:

- Dismissed the Send a’s appeal on the minority discount on purchase of Kiri’s

stake in DyStar. - Upheld the SICC’s order that Kiri is to be awarded full costs on its claim in Suit4;

- Awarded 50% of the costs of DyStar’s claim in Suit 3 to DyStar against the

Company and Manish Kiri (as against the SICC had awarded 10%).

Please note that award of 50% cost in suit 3 against Kiri for DyStar claim, the additional

burden on Kiri would be negligible compared to the amount expected to be received by

Kiri.

Disc-Invested.

1 Like

Valuation figure expected in a month or two and stock has already moved quite a bit since the march crash.

Seems like light is finally there at the end of the tunnel.

Disc: Holding a large qty.

2 Likes

Presented my takeaway on Kiri Industries in detail.

Covered topics:

About Sector

About Companies

DyStar Case

About Business

Future Outlook

Business Strategies

Fund Allocation

Valuation

Those who are tracking company can surely have a view and can have a discussion

3 Likes

Today may be the big day for Kiri, and maybe the valuation judgement can be expected. The matter is listed in the SICC court for 1pm IST hearing. Last month on the hearing the court had heard valuation arguments from both sides, and should give a decision today.

https://www.supremecourt.gov.sg/hearing/download-hearing-list

A refresher on the valuation:

The valuation will be conducted as on 2018, when the profit for Dystar was at $100mn. Assuming a conservative PE of lets say 10x, would give valuation of $1000mn. With Kiri’s 37% stake, it would come to 370mn (Rs. 2,700 crores).

Added to this would be the interest component, working out to 15-20% of the value, and profit share for the three years that the dispute resulted in Dystar not sharing any profits with Kiri.

Given that market cap is 1850 crores, including the standalone business, this should result in material upside.

However, one should keep in mind, the above calculation does not include capital gains tax (20%), and dividend distribution tax.

Shareholders are also unlikely to get all the cash, as management is expected to invest some in the existing business.

Disclosure: Invested.

3 Likes

Any update on this hearing and the consequent next steps? Did not get any disclosures from the company too…

Update. Disc. Not invested. Tracking.

1 Like

Have been reading about Kiri Industries for some time now. I think members in this thread are aware of the history of course. The valuation of Dystar at $1.6 Billion was on expected lines. So the net figure post adjustments that the MD, Mr Manish Kiri, expects to get eventually is in the range of $450-500 Million (INR 3330 Cr - 3700 Cr). This is a huge amount of cash. Completely changes this company’s fortunes. Many members have mentioned how under valued this stock is. I am an investor in this stock. But I saw the share price has actually declined after the positive news. I expected a rally post this news which will finally enable Kiri to reach its true valuation which I feel should be closer to 750-800 and above. (Maybe even 4 digits as some have speculated, but that could depend on how good the next quarter standalone results are to an extent, and Kiri’s plans of using the windfall of course).

Wondering, what is preventing a big rally?

1 Like

I hold the same view regarding the valuations.

However, the price movement may be not taking place due to two reasons:

a) Appeal left with Senda in Supreme Court, which shall delay the recover by 6 months (as guided by Manish Kiri in an interview) along with some changes in the valuations (personally don’t expect major change, if any.)

b) Recoverability of dues from a Chinese entity- not sure how much this factors in the pricin, but could be a major factor.

Could there be a staggered payment schedule offered by courts given the quantum (fellow boarders inputs invited).

Other than that I see no other reason for the pricing not having moved.

Disclosure: Invested

Regarding

a) Yes, it will take 6 months more. But after 5+ years of this case, does another 6 months matter for such a large windfall? We know the amount more or less. So no uncertainty about valuation.

and

b) This may seem like a concern and a similar thought did go through my mind as I have invested in this stock too. But the Singapore Supreme Court is strict, and Dystar plants are located across multiple countries luckily and not all in China. So any refusal to pay would see Senda lose control of Dystar itself and it can be auctioned by the Singapore court.

I doubt Senda will take the risk of delayed payment or default.

1 Like

Market may also be discounting the possibility that all that cash may not be used in the best interest of minority shareholders. I am not in a position to pass judgment on the motives of Mr Kiri here but having burned my fingers in LEEL (Havel’s buyout of llyods AC), believe it’s my duty to warn

1 Like

Management wants to reinvest the payout in good payback projects.

2 Likes

I read tge whole thread. I find everyone talking about dystar value unlocking. So i believe everyone wants to play only that part. But once settlement done, what is the business prospect of this company. For Dye industries, there are competitors not only from China but from india as well. How Kiri stands there. Any learned member can please provide that outlook please. We should focus on growth of core business rather than holdings of other company that too which may buyout in some time.

1 Like