True, there are many complexities regarding standstill view till Dystar case, which don’t seems to be only view point. There many factors which may turn company bigger.

Initially there were some anchoring bias that valuation of Dystar will come out to be 3-4 billion dollar which was sort of impossible. As an investor we have to look from different aspect as well.

Value unlocking would not be the factor only till Dystar case. Important aspect to look out is the post the case how the management will allocate the funds.

Many analyst are taking rough estimation that Kiri will get 2000-3000 crore and standalone value is 1000 hence stock can be double from here in a year.

But according to me this is not the way things work.

Imagine (even said by the management team) from the fund 50% will go in expansion of the Kiri’s business in other chemical segment.

While company has also taken necessary steps for the same (EC approval taken, registered to expansion).

Any new expansion and proper allocation will lead to additional value of Kiri. Expanding new plant will have its own multiple. Take it case where they expanded in flavours and fragrance business or Aniline manufacturing, and the business turned will.

Market will atleast 5 PE multiple to that plant which will turn the value of Kiri at much higher level than normal expectation.

Disc: Not SEBI registered. Already Invested.

Views are already mentioned in the article.

Hi skimmed through the thread ,i personally thank you for doing such a detailed fundamental analysis of the company making my work easier

since you have been tracking the company for a while here are few questions i want to ask you about the management of the company i believe that is what is important and what will matter mainly going forward.

This is a checklist which is followed by DR vijay malik(How to do Management Analysis of Companies - Dr Vijay Malik) i will go through it point by point and write what i understood and it would be great if you can add any further info that you might know

1)Promoter background(past decisions)

*i didn’t find anything wrong in this front for kiri infact i liked that the fact that the acquisition done back in 2010 was a great value investing and it will reap its reward in a decade fingers crossed ,so i am assuming the managment can invest the money in a great way they get from the dystar

*reducing debt year on year funded by operations

(please add anything else you want to in this front)

2)Promoter salary

*i find the salaries reasonable(4.64 cr for net profit of 376 cr in FY 2020) and (4.49 cr for net profit of 164cr in FY 2019)

*in-fact remuneration for pravin kiri and manish kiri was 12 lakhs to 15 lakhs from 2012 to 2015 despite company becoming profitable in these years directors didn’t take huge sums of money at the expense of minority shareholders.

3)related party transaction

Didnt find anything of concern here if you did plz add

4)Warrants for management analysis

i consider this a red flags here company has been exercising warrants back in 2016 and 2018(plz comment the reason for this )

5 promoters faith in business

i see promoter shareholding decreasing in the recent quarters any specific reason for this

on the contrary they have also mentioned about buybacks from the money received.

5 promoters faith in business

i see promoter shareholding decreasing in the recent quarters any specific reason for this

on the contrary they have also mentioned about buybacks from the money received.

since sep 2019, promoter stake is constant 41.61% so the isn’t an issue anymore I guess.

Kiri industries seems to be stuck in the same range for a very long time. Luckily I completely exited this stock a few years back. Or else it would have proven to be a massive opportunity cost. The overhang of the Singapore court case continues. The end result of the court case also may not be entirely in Kiri s favour. The standalone business is a pure commodity business not worth looking at when there are much better speciality chemicals and niche businesses to invest in.

I couldn’t get hold of the Shareholder’s Agreement (SSSA) so don’t know whether an “Exclusive Jurisdiction” clause is there or not. Does anyone have any information about this?

If hypothetically, there were a “Non-Exclusive Jurisdiction” clause, could Senda take the matter elsewhere to protest against the judgement? Or would they have done by now if that were the case? Is there anything else that can potentially go wrong from here?

That could be the only hindrance. Otherwise, it all seems very rosy indeed. The funds received would “at least” make the then standalone book value 80-90% more than the current market cap.

They would have surely done that by now.

Game is over for Senda.

They can appeal in SC, but I doubt SC would contradict respected SICC judges.

Only worry is whether Senda will go rogue and just refuse to pay, (this will fall under contempt of court order) and take harbour inside Chinese border.

Then Singapore SC will have to seize Dystar assets outside China and auction assets to pay off KIRI, and that may delay the money by a year. Senda will lose all credibility globally. Doubt they would take this extreme route.

Hey Keshav, can you share the link here? From my research, senda had appealed against the minority discount which the supreme court had dismissed. As a ploy to delay proceedings, Senda can still pick up elements of the order and appeal against them.

Final order of Supreme Court available at BSE. Approx Valuation comes at 3500 cr (Pre-tax) as it would cut the amount drastically, still sizable amount. Further it would take some time to get the money in hand as a saying - there’s many a slip between the cup and the lip…

Submission at BSE as under:

We are pleased to inform that the Singapore International Commercial Court

(“SICC”) vide its final judgement dated June 21, 2021 has confirmed the final

value of Kiri’s 37.57% stake in DyStar Global Holdings Pte Ltd (DyStar) at

US$481.60 Million (approximately Indian INR 3,570 Crore), after giving effects of

two minor adjustments. The buyout order to be executed at value of US$ 481.60

million as ordered by SICC vide their judgement dated July 3, 2018.

I think the management is on right track. Based on my understanding, it will take a few months for the money to come into the kitty. With current cash + investments equaling to 1200 Crores, 3800 crores settlement is an icing on the cake which will take the total to 5000 crores. The company also has negligible debt. This can be a potential value unlocking opportunity unless the promoter messes it up. A hefty dividend also is a possibility to reward minority shareholders.

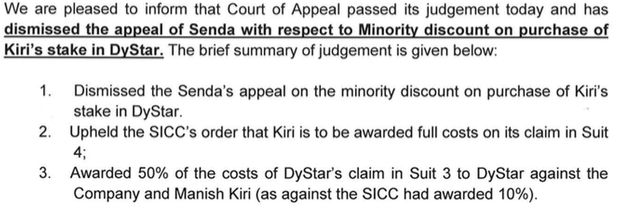

Minority discount was one point. The second point in the above being independent and encompassing within it the valuation work that had to be carried by SICC, I think this is an indirect way to think that the Supreme Court has already given their verdict.

The Minority Discount thing that you’ve mentioned was also contested which the court dismissed and at the very same time as you can see above, they’ve upheld SICC’s order on Suit 4 (stake sale to Senda).

Hey! The ~1200Cr investments are on a Consol level. We should see only from standalone level as most of the accruals have been notional (cuz of DyStar). The Consol Book Value is nearly ~2000Cr but the standalone is only ~600Cr.

After tax they’ll get something like ~2500-2700Cr, which takes their then Book Value up to ~3100-3300Cr. That’s roughly 50% more than the market cap. Good thing is their cash value of assets will still be 25-30% more than the Market Value. So there’s at least that much margin of safety if we’re not focusing on Kiri on a going concern basis and purely as arbitrage.

Building a specialty business in this highly competitive industry would be quite challenging and fraught with high execution risks but there’s quite a lot of scope to not mess up with the kind of cash they have.

Great. The value gap will close keeping the arbitrage involved in this case. If they are able to grow their topline and margins also, then it will be a jackpot for minority investors. However, that is uncertain as of now.

The company has outstanding FCCBs, as a result of which the outstanding number of shares of the company come to 5.18crores on a fully diluted basis, against current 3.27crore shares.

Given the same the per share amount to be received would come to Rs.521 only (2700/5.18crore), not leaving a very high upside on a cash basis alone, as the current market cap does not account for the pending dilution.

Please let me know as to how the above argument is wrong?

The company has outstanding FCCBs, as a result of which the outstanding number of shares of the company come to 5.18crores on a fully diluted basis, against current 3.27crore shares.

Kiri’s standalone EPS at last 3 year avg around 14.8, diluted EPS after FCCB conversion will be 9.34.

Since Kiri’s standalone business hasn’t shown any signs of growth last 3 years, assume we are generous and give even 10PE value, standalone Kiri is worth say Rs 93 a share.

Given the same the per share amount to be received would come to Rs.521 only (2700/5.18crore)

so dystar on diluted based if we get Rs 521. share, then the total value of Kiri will be Rs 614.

So don’t see much upside from today’s price of Rs 614 unless Management uses the cash well to beat competition and grow business.

Kiri is also having 40% stake in subsidiary Longsen. so consolidated yearly PAT with this subsidiary can be around 130crs, if we consider last year as exceptional. Plus Kiri has completed around Rs.200-250crs of expansion on standalone basis so we will get uptick from these expansions too. so I thing giving valuations of Rs.93 except Dystar is not reasonable. + its other expenses were also more due to Dystar case legal fees.

I think they will see uptick in their standalone earnings in coming years.

Company is expecting Rs.1500crs of sales after completion of capex on standalone business with EBITDA range of 15-18%. Most probable of this targets is Fy2023.

I think the latest Q results are positive for Kiri. If they continue this path, standalone EPS expansion will really make this worth buying even at 600 levels for holding next 4-5 years.