Q4 Results and Presentation

Overall good performance but Mr.Market is indifferent to its nos. Stock trades at 8x on TTM.

What is missing here? Any views?

Q4 Results and Presentation

Overall good performance but Mr.Market is indifferent to its nos. Stock trades at 8x on TTM.

What is missing here? Any views?

The balance sheet is not comforting. Loan borrowed to pay goodwill. Surprisingly they haven’t impaired any goodwill yet.

U mean loan borrowed for acquisition…right??

The balance overall is weak. Goodwill is the biggest asset that seems to have sucked up most of the borrowing and retained earnings. No company has 100pc acquisitions done right. Impairment is usually there. In this case, only profits but no cash.

Probably in IT companies… intellectual property and goodwill are biggest cost of acquiring an entity…they dont have much hard assets…

I thnik if i believe the numbers and auditors…this one seems to be undervalued… especially since it is smac implementation zone…

Read on last 20 of history of Indian IT mini hot sector bubbles/frauds starting from internet bubble to education tech to value added services to e-governance to document mgmt system to remote infra mgmt system to the latest phenomenon SMAC. There r N compamies which got butchered due to own mistakes or markets n just read the kind of growth vs balance sheet n cashflow theh carried. Right from pentasoft ssi to teledata to bartronics to tanla to geodesic to omnitech to allied digital to… the list goes on. There were many things common. A hot theme gives rise to many hopes but a poor balance sheet n cashflow could be the reason why hopes and reality never meet. I ve not analyzed tgis company after looking through basic financials n working in this area and hence cant comnent in detail but I am sure if one analyzes the history stated above , it would help in decision making.

Is there any alternative to researchbytes to access concall recordings?

Researchbytes has been blocked by Kaspersky on my PC as a phishing site.

You can download Research bytes App on ur mobile. Its very good.

I too did basic Screening and this stock does not looks well. Receivables are around 3 times of its annual Profits. 5 Year CAGR Revenue and PAT growth is above 75% , i mean this is insane. Tax % is not even up to standard rates (Though i have not analysed deeply for the reason of low Tax). In last 5 years , company did capex of 176 Cr while their operating cash flows are just 112 Cr. They paid interests of about 30 Cr in last 5 years. So to fund this outflow of 96 Cr (Capex 176 + Interest 30 Cr - CFO 112) , they took loans of around 118 Cr. So it is all a case of acquiring companies through debts. It will be a big risk if those acquisitions does not go well. Also too many acquisitions itself is a concern. The bonus issue factor also raises some doubts, Do remember Vakrangee too declared bonus just before crashing. These are only simple screening data’s which raises many doubts.to me and that is why i restricted my search here only. I may be wrong but this company has all the signs of joining the ranks of Vakrangee and other such companies.

It seems “Next Vakrangee” is the new favourite stick for people to beat companies with.

I came across this company and numbers look attractive from a distance. So before going into number crunching i thought to first look at what do they do. I opened the site and wanted to understand their offerings. Suddenly customer support window popped up on the screen. i thought lets see whether a real person sit on the other side or it is just another machine working on that side. I asked some question like what do their company do? do they have the expertise to develop something using block chain technology?(he said yes) then i asked what is your market visibility in block chain expertise. he asked for some time and reverted. As per that person (with kind of answer i received, guess it was human) their center of excellence includes Hyperledger, Ethereum,Coindesk and others.

The point i want to make is if this is true and they’ve such level of expertise in blockchain then obviously the tree can grow bigger.

I am also working in IT sector and worked in 3-4 big and small IT companies. I have seen managements talking about block chains and digital every time , but have not seen or experienced anything much on ground level. Its more like a concept. I even asked a question to my current company ceo , he said the same thing. Companies are not getting much revenue from them, They are just a concept. It seems like a hype to me, I may not be correct in my interpretation but thought of sharing what I have experienced.

I think these are enough to say good bye to further analysis. Hope promoters make themselves rich

oh, forgot to mention, equity dilution within 5 years of listing, bonus issue and promoter selling timing etc…

Hi,

I think a few key facts are really misleading from your statements

_Trade receivables have sharply increased and constitutes 87% of their FY2018 revenue

Kindly see the consolidate B/S it is 187 cr which is about 24% of total revenue

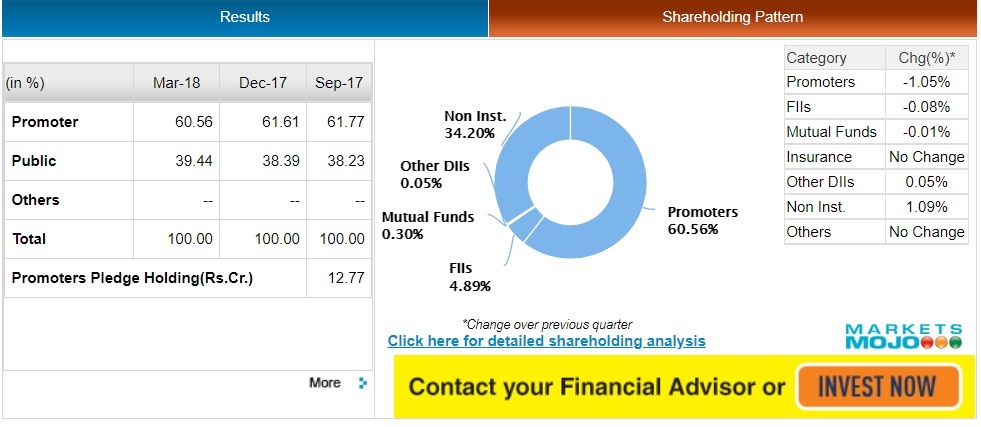

_Promoter sold shares in open market during bull market. and reduced the total percentage from 62% to 60%.

It is showing 61.9 and it has been almost unchanged in last few quarters

And on ur point on Goodwill, although true but that is the way it is since majority of the business were acquired and were not generating profits.

I work in IOT startup and we work with a MNC FMCG on Industrial IOT. The level of penetration of Industrial IOT is still limited. This is a last decade catchphrase.

All the catchphrases sound good on the vision and mission and it is really difficult to make money out of them.

Q1 results date:

The next board meeting of Kellton Tech Solutions is to be held on August 14, 2018 for Quarterly Results

https://www.moneycontrol.com/company-facts/kelltontechsolutions/board-meetings/VMF#VMF

Disc: Invested

This company is a cultural mis-fit, too Americano!

We still expect promoters (and their generations!) to stick with a company. Also, they are forthright and speak their mind! God help them!

Currently, the company has a revenue run rate of about Rs 500 crore and is targeting to generate Rs 2,000 crore turnover in the next three years. “This, we intend to do both through organic and inorganic growth,” said Niranjan.

As for acquisitions, he said, the company was looking for companies that can either give it deeper industry presence or complement its technology offerings.

“We are always talking to companies. We have given the mandate to bankers to scout for potential targets. Evaluating the right company is a continuous and on-going process,” he said adding that the potential buyout could be anywhere between $10 and 100 million.

The three technology firms the duo started and sold had an average time span of 5 years and they intend to replicate the same here. “The idea is to create value and move on if we get a right price. We will not hesitate to exit if the timing is right,” Niranjan said.

I did a high level analysis of this Company in Nov, 2017 and did not consider it worthy of investment.

Following are the red flags due to which I rejected it at an overview level itself and did not proceed to do a detailed analysis:

.

.