Hi Thanks Rahul.

Yes positive financials, 62% promoter holdings, 4.92 FII holdings(1.2% increase in June Q). Surprisingly No MF holdings, No Big names holding.

Kellton & Cupid both waiting for discovery by some Big Names.

3 days back, Kellton was moved to T-T category on NSE and BSE, which means that there can not be any intraday trading possible in it. If you buy you must take delivery and if you sell you must give delivery. It is being said that this moving to T T segment is done to protect investors.

Seniors on VP, Is it actually a good sign that a scrip is moved to BE series? What sort of manipulations does shift a normal scrip to BE? Are promoters to be blamed for these manipullations?

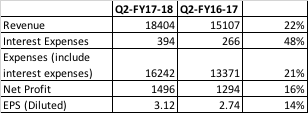

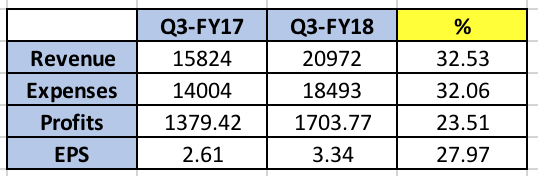

Decent numbers from Kellton for Q2

http://www.bseindia.com/xml-data/corpfiling/AttachLive/8e436a2f-813c-49d6-a0e8-3b1da44ed3f8.pdf

One thing I like is that they been consistently showing YoY along with QoQ growth. Hope they continue the momentum. Huge Goodwill on books looks bad though.

They didnt mention about order book or any significant win, maybe will talk in conf call on that.

Conf call scheduled on Monday at 4:00 PM IST. I wont be able to join , incase someone joins pls take notes and share.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/0a702096-8b4e-4838-a2aa-05af561e067e.pdf

Date: December 11th, 2017

Time (IST): 4:00 PM – 5:00 PM

Dial-in Number: +91 22 3938 1009

The number listed above is universally accessible from all networks and all countries

Local Access Number: 3940 3977

Available in - Ahmedabad, Bangalore, Chandigarh, Chennai, NCR (Delhi, Gurgaon, Noida),

Hyderabad, Jaipur, Kochi, Kolkata, Lucknow, Pune

Accessible from all carriers

India National Toll-Free Numbers: 1 800 120 1221 / 1 800 200 1221

International Toll-Free Numbers:

USA – 1 866 746 2133

UK – 0 808 101 1573

Singapore – 800 101 2045

Disc : Invested

2 Likes

Earning presentation uploaded by company today

http://www.bseindia.com/xml-data/corpfiling/AttachLive/60b71445-328c-4201-bc34-5b18c2a2f94d.pdf

Kellton reports very low Depreciation/ Amortization costs although it spends a lot in acquisitions. What is the reason behind that?? is it an accounting gimmick?? The net profit will be very less if the amortization costs are increased. In the past 4 years, Co has reported a negative free cash flow of more than 100 cr, mostly due to acquisitions.

In Sep’17 quarterly report, It was given

(1) Goodwill includes all future contingent earnouts as prescribed under IND-AS

(2) “Contingent earnouts towards acquisition of subsidiaries is accounted under Other Financial Liabilities as per the requirement of IND-AS”

If these additional payments are recorded in P/L statement, net profit will be less right.

Any suggestion is appreciated. There must be some reason for this stock trading at very low P/E although showing good growth every quarter.

3 Likes

The major issue is the debt funded acquisitions at a premium for entities that generate sub 10% net profit. If the KPIs are met, the contingent consideration will lead to further cash outflows and lower profits.

PE is low given no cash flows, weak balance sheet and no tangible assets.

Secondly they haven’t impaired goodwill which surprises me. No company can ever have investments that don’t fail.

Unless the balance sheet is cleaned up and cash flows pick up this is a risky investment

Is there any place where we can see when will Kellton be out from TT category ?

Also the list of companies which are in this category.

2 Likes

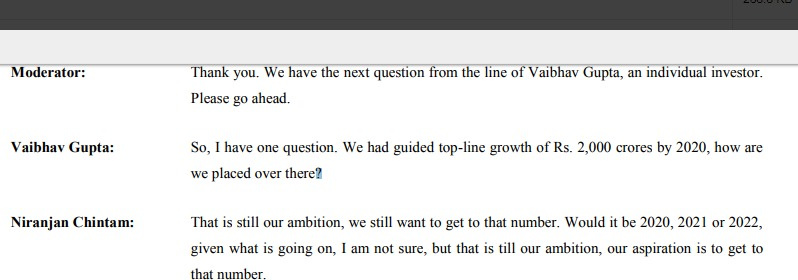

Few snippets from Q2 FY18 concall, which i find amusing -

They earlier said by 2020, 2000 cr revenue. Jacked up stock price to do QIP, which didn’t materialize. They say they have set these lofty targets with an insurance banker. Amazing! Straightforward formula…give lofty guidance, jack up the share price, so QIP, add more goodwill to jack up Balance Sheet…

Out of 450 cr assets, goodwill 212 cr and receivables 143 cr form 345 cr. Goodwill is a problem with lots of IT companies.

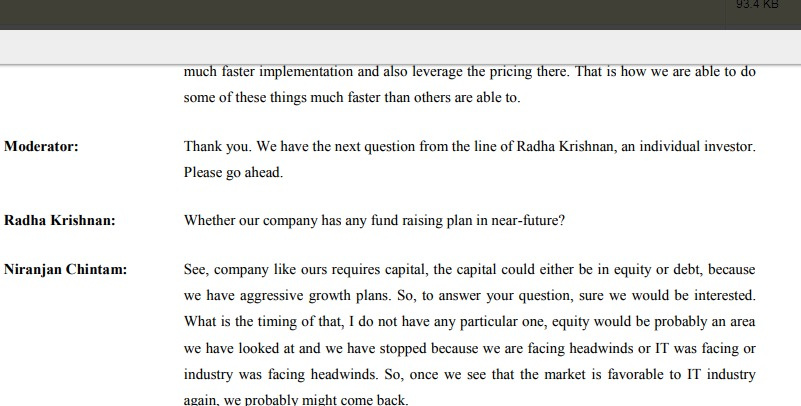

- About QIP - Well, as they said, they are still growing at 20% pa. What stops them from doing a QIP? They keep on saying 20% is an amazing growth number.

- They keep moving on to newer technologies just like that!

As many of you guys have pointed, serial acquisition led growth fueled through debt or dilution is a recipe for disaster. They are pledging their shares in order to do acquisition in order to maintain steady growth. If the numbers lack consistency, they will not get higher valuation. If they will not get higher valuation, they won’t be able to do QIP at desired price. Vicious circle!

4 Likes

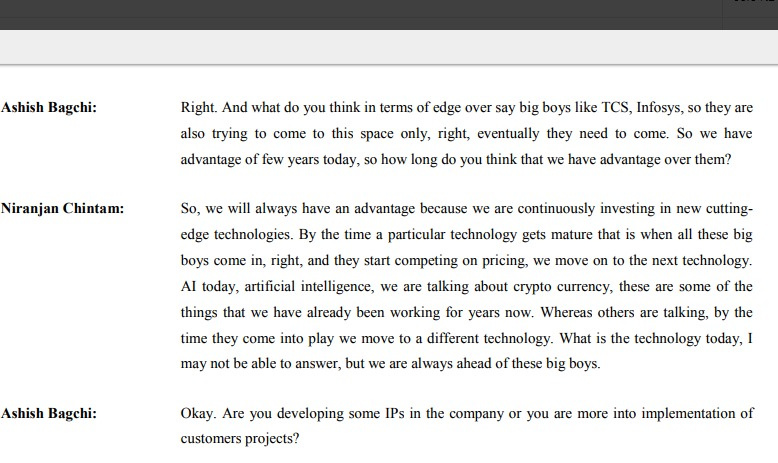

Adding to Mridul’s view for Concall Transcripts . As per Mr Niranjan

1)When quizzed about “developing some IPs in the company” nothing other than platform advantage for quick implementation. Definitely not sustainable moat in long run.

2)Company likes hopping on to different technologies …they are silently betting on crypto stuff and already trained substantial number of people. It may or may not work out

From what i concur company seems to be betting heavily on identifying future trends before Big Boys(read Infosys ,TCS) do. Moreover IT companies of our country have already lost long cherished cost arbitrage advantage. Unsure of long term prospects.

Disc : Only tracking position

2 Likes

I was trying to assess the impact ( +ve or -ve) on the revenue of Kellton due to US tax cuts however could not conclude anything.

If someone has good understanding on this subject, could you please help us on this.

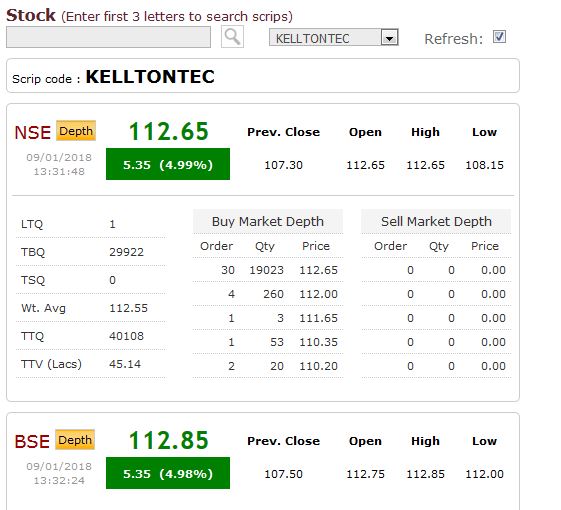

There was no seller for this today

Kellton to consider bonus issue as per press release today - at results on 6Feb

This is too much from Kellton. Why they want to dilute equity further. Share price is not that high for considering a Bonus issue.

2 Likes

And here you go, another good quarter

Board declares Bonus 1:1 ( I didnt like this move, not sure why they did this)

http://www.bseindia.com/xml-data/corpfiling/AttachLive/9bd78f30-7bb0-4caa-a3b8-195a5cb751af.pdf

I was looking at buying this stock.

But this bonus has put me off.

A bonus for what?

Bonuses used to be a nice bait for gullible investors a few years back. Not a rule but wondering why this bonus!

1 Like

I agree with you and have exited the stock due to same reason. So far, the consistent sales and profit growth along with perfect predictions of the same by the management was creating doubts in my mind about genuinity of results. But, this bonus share issue without giving any logic behind the same has been the decisive factor for the exit.

Another acquisition

It mentions Kellton tech as one of the Key Manufacturers of Digital Transformation market among HP, SAP, Google etc others

I would appreciate your thoughts.

2 Likes

Aegon life insurance company partners with kellton tech solution.

1 Like