It’s 7.78 Cr on the cash side. But they do have cash equivalents and overall cash is 337 Cr as per the conf call.

1 Like

I will disagree with the re-rating part. Typically high ratings are assigned when markets believe that the growth will be there and that too secular growth for an extended period of time.

A lot of times markets during the initial growth periods of a company assumes that the growth is secular and will continue ahead and thus high PE multiple are assigned. But once the growth slows and market realize that the growth actually is not secular, the multiples are de-rated- first for lower growth and 2nd for nonsecularity.

The same happened with Avanti Feed, Kaveri Seeds. Wherein during initial growth periods, markets thought that the growth is secular and will continue. But as soon as grown broke, markets realised that these are not secular businesses and thus even if these companies go back to old growth rates, they will never get the old p/e multiples which they got in their first cycle.

4 Likes

All points are valid. Having said that I would like to list a few points below which may support valuations re-ratings.

- Overall Mr Market’s current Narrative is shifting gradually. In this main narrative, Agri sector’s story and the role is very positive. This will be perceived as per the main narrative by market participants.

- The market may treat the entire Agri sector is immune from COVID19 implications thus may command high valuations on relative basis to other sectors in the interim until final solution is found for COVID19.

- Finally, Kaver’s Balance Sheet is very strong and business is better than normal. So it’s exhibiting some of the resilient’s business characteristics amidst the current uncertain times.

Regards,

Ramesh

Disc: Kaveri is part of my Satellite portfolio with 2% allocation of my total direct equity.

1 Like

IMO Kaveri and Avanti are secular growth stories. The company has been guiding a 15-20% sales growth with a 18-25% profit growth for the next 7 years. This guidance has existed and been delivered for the past 2 years. Few data points to support the claim.

The company maintained its volume growth guidance of 15-20% for cotton business and 20-25% for non-cotton business for FY20

-

Hybrid Seed industry as a whole is expected to grow 8-10%/year over the next 10 years (was 12%/year for the last decade) as claimed by Mithun Chund. So it is a secular tail wind.

-

Market share of Kaveri Seeds is quoted to be 10% overall and 15-20% in Cotton. They are expanding dealerships to the northern states to drive more market share. Hybrid rice, they have 10% market share right now and market itself is only 10% penetrated. So they are growing fast on that, on more hybridization of market as well as expanding market share.

Overall there are 4 sources of growth for Kaveri Seeds, which has been quoted in the other posts in the thread as well. In the order of importance:

-

Hybrid seeds market overall growing by 8-10%/year for the current decade vs the 12%/year for the past decade.

-

Market share expansion in the north with the addition of more dealerships. This drives market share both in cotton and non-cotton seeds.

-

Faster growth of non-cotton wrt cotton with relative market share expansion. Company has gone from 60/40 cotton to 50/50 and has guided 40/60 in 2-3 years. The other varieties such as Maize, Rice and Vegetables, management claims could be as large as cotton in a decade. Hybrid rice for example, grew 60% y/y this year. Vegetables grew 30% y/y. Keep in mind that non-cotton is twice the margins as cotton, since they are not price controlled by the govt.

-

Exports. Just started exporting to Myanmar, Vietnam, Bangladesh and the management expects this to start materially contributing in 2-4 years.

The secular growth is also very clearly visible in the numbers. Kaveri grew 60% y/y for the 10 years before 2015, when the cotton price control happened. The next 2-3 years with additional price reductions of cotton seeds, Kaveri Seeds was in a tough spot and its profits halved. It took a while for the company to compound out of that, halving in profit, but looks like the engine is back.

15 Likes

Has anyone done DCF analysis on this based on FY20 trends ?

so much business talk…yet no one talks about the pending audit reports by NSE the company had promised years ago; Wirecard took 10 years to play out, not saying is so, but how come company says yes we will do audit years ago and then no follow up. ?

With reference to the above, please find enclosed herewith the information in the

prescribed formats under t}le provisions of SEBI (Substantial Acquisitions and

Takeovers) Regulations, 2011 the Company has received the intimation on 23.d Juty

2020 from M/s. Pabrai Investment Funds in connection with the disposal of 18,97,577

(2.23%%) Equity Shares of the Company in the open market

1 Like

Kaveri Seeds – Q1 Conference call summary/ Takeaways

Solid set of numbers from Kaveri Seeds – PAT has grown by 28% and revenue by 15%

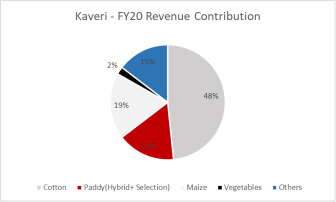

Rice as a segment is growing very well. In the next 3-5 years, it will be a bigger segment than cotton and with higher margins. They are already in the Top 3-4 players in India and are constantly gaining market share

Vegetables as a segment is also growing very well. It will conservatively grow from a sales of 20cr to about 30cr in the coming year. From a low base, the growth is expected to be 40-50-% for the coming few years, again with high margins

Cotton has de-grown this quarter, but since they have grown market share, they have shown minor growth

Maize prices are low and hence hasn’t grown too much

They are gaining market share in almost every crop

Due to Covid-19, there were some difficulties in transportation of seeds. Because of this situation, illegal seeds have gained some traction this quarter. This trend however, should not have an impact on them

Vegetable crops for Kaveri primarily include Okra, Bitter Gourd, Cabbage, Cauliflower and Hot Peppers. In Okra, it has already established market leadership

They have 500cr+ of cash and they have no major use of it. They have done 3 buybacks in the previous years and are likely to continue this policy

Their 3-5 year strategy is to constantly add new hybrids, expand in the northern and central regions, increase exports, and expect high growth with high margins in rice and vegetables. At the same time, cotton and maize will see growth too but lesser than the others

They compete with mostly MNC’s in non-cotton crops and with domestic players in the cotton segment

The risk in their business is lowered cause of crop re-balancing. Which means that one crop is sown at the expense of the other. And they aim to be market leaders in many crops

It will predominantly always remain a Q1 heavy company, since all their field crops are sown during these months i.e. Cotton, Maize and Rice. But in absolute terms, their Y on Y performance will improve in the other quarters too, since some of their vegetable crops are grown all year round

Govt. policies have been very helpful and it will ensure that agriculture will grow well in the coming years

Their guidance is that revenues will grow by 10 - 15%, and profits by 20-25% in the coming 3-5 years

My view is that Kaveri is in a dominant position in the seeds markets and its market share is only expected to increase further. I would call this a Covid proof business, given the nature of what they do. It has the highest margins and is the most diversified in terms of the number of crops. Its R&D and distribution gives it the ‘right to win’ in multiple crops. At the same time, it is high on FCF and ROCE, with a clean balance sheet. Only slight overhang remains an audit, that was conducted a few years ago. Even after the good run it has had, given that the valuations still look low, I think it has some way to go

Disclosure: Invested

13 Likes

KAVERI Q1 FY 21 CONCALL NOTES. (thanks @rishit.05 for keeping the interest in this company alive.)

CONCALL ANSWERED BY MITHUN CHAND.

Revenue growth 15%, EBIDTA growth 39%, PAT growth 29%.

EPS for the quarter 49.67, a growth of 36.57 %.

Cash and equivalents at end of quarter 524 crores.

New hybrids continue to be the focus area for the company.

GROWTH PLANS FOR NEXT 3-5 YEARS.

Good product line to achieve good growth. Continuous effort to introduce new hybrids and enter new geographies.

Have a portfolio of many crops and achieve leadership in them.

Increase R&D spend.

Growth in central and northern region.

RICE HYBRIDS

Every year, acreages in hybrid rice are going up.

Central and eastern region main growth in hybrid rice.

Industry wise there is 4-5% growth in hybrid rice.

Company has gained significant market share and grown at 35-45% CAGR in last 3 years.

Company competes with MNC in hybrid rice. In selection rice it is market leader.

Proportion of rice as a percentage of revenues can be more than cotton in next 3-5 years.

RABI CROP

More cautious on second half but Kaveri not likely to be affected much as it is present in many crops and various geographies.

If exports of maize start, sentiments towards it can improve.

VEGETABLE.

Okra, tomato, chilli are major contributors. Company is now into hot pepper, eggplant, cabbage, cauliflower etc.

Very good and highly profitable segment. Margins are better than field crops.

Company expects good prospects for next few years.

Last year sales was 20 crores, in fy 21 likely to be 30 crores.

ILLEGAL SEEDS BUSINESS

This has affected most companies because of transportation problems faced by the companies.

But both state and central govt are acting strictly against these.

Likely to come down going forward.

EXPORTS

20 crores exports in fy 20. This year, plan is to grow higher.

Company will focus on areas which are similar to India in climate conditions.

Company has listed 7 countries as focus areas for exports.

Plan is to double exports over next 5 years.

CAPITAL ALLOCATION

Keep 300 crores as war chest and distribute rest to shareholders in form of dividends and buybacks.

MY IMPRESSION.

Company plans to grow at consistent 10-15% CAGR.

With reduction of cotton percentage in overall revenues , margins are likely to improve and hence profit growth will be higher.

Rice segment needs to be watched as the next engine of growth.

Company generates lot of cash and can continue buybacks on a regular basis. Hence on reduced equity, earnings can grow higher.

disc: invested post q1 fy 21 results.

24 Likes

Hey rikirana. The only thing that’s happened is you have a fantastic company available at an even bigger discount price. Nothing changed today. Everything is the same since the last data point ie Q1 which was fantastic. If buying an undervalued stock sometimes you have to wait for the market to catch up with you which may take months or even years. If you beleive in the management and trust their vision and earnings view for the next 5 years this is nothing but another buying opportunity. The stock price is under pressure due to the well publicised selling by pabhrai too. Even looking at it technically the volumes were low today and it closed near its support. Impossible to tell what will happen daily though. Patience is key

Update: Prabhai has sold around 30 lakh shares last few months. Considering the average volume per day for Kaveri is around 1 to 2 lakhs you can imagine how much the selling pressure has been last few months. All of these shares have been absorbed keeping Kaveri above the 200 DMA line though. Infact no Mutual funds have sold since Feb and in august was the highest number of mutual funds buying this year(all sources above are via trendlyne). The only question is when will Prabhai be done? He has already sold nearly half his holdings… hopefully the selling pressure is now going to be reduced but either way this just looks like a buying opportunity considering the selling negated the Q1 results trigger. The next question one may ask is why is Prabhai selling half his holdings when he is known for patience and people suspected just a little re jigging and profit booking and not him selling half his holdings (and maybe more). A lot of people began trusting the management after they passed his checklist after the issues in 2015 to 2017… That question cannot be answered yet

3 Likes

Firstly, I like Kaveri seeds and it clicks most of the right boxes. But one of the reasons it has de-rated was over dependence on cotton seeds. Cotton seed prices are controlled by the government since 2015 and they have been heading down putting pressure on margins.

1 Like

You are right. And that’s the reason it is available on sale right now. Read the fantastic posts above, the latest concalls and annual report and you’ll see how management has planned lower dependance on cotton and growth drivers in rice/maize etc and how they will never have this problem with one product dependance again. It will take some time for a re rating since the carnage of 2018 is still fresh in the mind. If you trust the management to do what they say(and I see no reason not to) then this new version of kaveri is a better , secular version than the one from 2011 to 2015 and I can see them going on a similar run again… only this time without any product dependancy issues and this will lead to sustainable earnings and a re rating in the future for this cash rich company. Cheers.

Disc: Invested(sold off due to huge red flags during its previous runup back in 2016 and bought again last month after I was convinced these red flags were no more)

3 Likes

Hi I have just started reviewing this stock, could you please recap some of the red flags that the company suffered from during 2016?

Lol where to begin. It all started when the government began price controlling cotton. It was all but obvious that the profits would be hit long term but the management kept talking about things getting better soon even though they only got worse. In hindsight they probably lived in hope too since they had a decade long brilliant run before that… but the results just kept getting worse and worse. This was due to their dependancy on cotton… something I’m glad to see isn’t there on any more. Diversification and multiple growth drivers is necessary for a company like this so that’s one thing taken care off. Then began the fights with Monsanto regarding royalty… ended up being taken to court. I can’t even remember why anymore but I remember already panicking. Then came the final nail in the coffin for me… a forensic audit from sebi vs the company (along with another seed company I remember). At that point I’d had enough and sold. You only get to know how good a management and company actually is in tough times … and man it felt like all the cock roaches were out. I’m glad to see how well they’ve fared for themselves since… it’s almost like they hit the reset button and started over and now those problems look behind them. The icing on the cake was when Mohnish Prabhai bought a huge stake a few years ago. This took care of my fear of the management… why would Prabhai buy if the audit issues were still a huge threat. So I’ve decided to hop on board again post Q1 when I saw the result and the posts by Hitesh sir, rishit and prasanna since I’ve seen how powerful the ride can be before… however, this time il have my eyes more open. The irony is part of the reason I bought is due to Prabhai trusting the management… however, the shares I bought are probably from his stake that he sold a few months ago … I dunno why he is leaving in such a hurry since he has sold nearly half his stake(Things like this can sometimes causes irrational fears of the audit to pop up again lol). However, I trust that the earnings will be fantastic next few years and that’s all that matters for now. I honestly cannot see how the next 5 years won’t be fantastic for the company considering the tailwinds and diversification + growth drivers so I’m willing to overlook irrational fears for this 5 year period atleast

11 Likes

Thank you so much for this fantastic overview. I have done some quick research and it seems there are only two main seed companies in India, Kaveri Seed and Bombay Burmah. Why have you decided to choose Kaveri Seed despite the possible management red flags that exist?

There is Nath Bio-Genes too

I am not a farmer, but I have a little kitchen garden and my thinking would be on the lines of why would Kaveri get repeat biz? I plant a crop and then get tons of seeds for free from the produce, for myself and to share with friends and family, even do some illegal sales perhaps. If I keep planting the same set of crops then I never need to buy from Kaveri on a repeat basis unless they come up with some better variety.

Disc: not invested

1 Like

It doesn’t work that way… It is about genetics … There is F1 generation seed which is what is sold to you and you won’t get the same seed attributes for the entire crop if you plan the F2 generation seed… output will decrease, disease/pest resistance will decrease and in some cases, crop itself will not come up properly

7 Likes