Kaveri seeds Q320 very rough call notes

we have grown 55% revenue growth…its from volumes…mainly from hybrid …price increases are 1-2% annually only.

have increased market share…hybrids grown well

we focus on south and rain fed conditions. we are only Indian company…we are competing with MNC cos

slowly getting into Rabi products in last 7 years…gaining slowly

profit is 50-100 rs higher per packet

we were selling 1 cr packets earlier…now we selling much lower

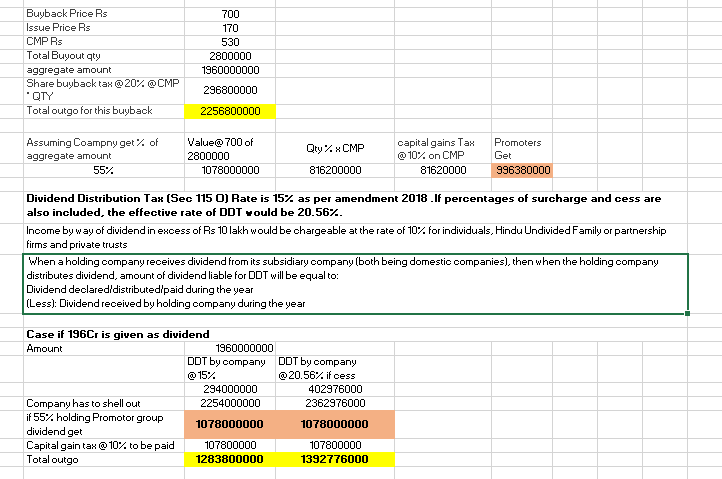

last 3 years been doing buyback

we need 300 cr cash of warchest over that will want to do buyback/dividend…nothing else to deploy…in few cr capex…20-30 cr annually…we can grow 15-20%…

maintain 15% growth…(cotton 10-15%…non cotton 20-25%) growth

rice hybrid market is …43 mn hectares…rice cultivation….3.5 mn is hybrid…10% penetration….

hybrid vegattable seed market 2500 cr market…many players many small players….much lower hybridization…

3-4 years ago…cotton seed …we were taking advances from dealers…as cash discount. farmer was picking up. we have postponed tking advances…now we have restarted…taking advances…industry also doing now… this is only in cotton. ; prices are down so much and production cost gone up…even though our margins are higher than industry….we give low dealer margins versus competition… as we have high demand for our seeds. Dealer is happy to take our seeds without paying advances

Kharif was poor…this year but Rabi has started well…as enough water. sentiment is v good, dams are full. end of day…monsoons arrival…depending for next kharif…if monsoon delayed…will depend on monsoon next year

some cos saying…enough water. for timely sowing of .kharif season as well; Kharif is rain fed… (water is good for Rice as that’s well related cultivation0; cotton …maize…crops need monsoon…most Indian crops are under rain fed

Production cost for cotton …shouldn’t go up…we have changed some techniques…

cost of goods includes …write offs : 4-5 cr in this quarter…regular…and comparable previously.

Cotton inventory : we have enough inventory…9-10 lac/mn packets inventory. Pink ball worm….farmers are v much aware and are spraying pesticdes for the same

employee costs is up…due to one time…this qyarter…we give incentives instead of other…going forward should be 15 cr…we have added more people…that 19 cr…should be 15 cr

Industry wants to increase cotton price…and govt wants to decrease…always…remain such

cost per packet…GMS technologies…pollination new techniques…educating farmers…choosing of locations so that we get good yield…slowly translate…into cost reduction…in 2-3 years…

350-400 rs …cost of produciton ( go down 10-15 rs…)

revenue mix : 50: 50 cotton : non cotton…going forward…40% cotton…in 2-3 years……non cotton : hybrid…Rice, vegatbles…maize, bajra

20-30 cr capex for next 2-3 years