Cash may be in the books of Jubilant Pharma which is 100% subsidiary of Jubilant life and registered in Singapore…equally debt is also in books of Jubilant Pharma…

Extract from Today’s TOI:

Recently, noted pulmonologist Dr Jalil Parkar, who spent five days in intensive care, criticised the government’s lackadaisical approach in streamlining the availability of drugs such as Remdesivir. He believes he would “not have made it” if not for his colleagues and wellwishers who arranged for the immunosuppressor Tocilizumab and the anti-Ebola drug Remdesivir. Doctors across private hospitals have urged the state government to speed up availability of Remdesivir.

Posted here just to highlight efficacy of Tocilizumab and Remdesivir against Covid19.

2 Likes

Demerger scheme vote as per NCLT

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b6695d0b-bd6d-45df-9363-27be80a69feb.pdf

1 Like

Jubilant received permission for remdesivir ::

1 Like

@ORION

Hi Sir,

I have 2 queries about Jubilant life-

-

What’s the status of Ruby fill litigation as you mentioned that Bracco has appealed in federal circuit in Washington against Jubilant life?

-

What’s the current status of Demerger and how exactly it will benefit the existing shareholder by value unlocking?

It will be great if you can share your thoughts & knowledge.

Thanks for the guidance!

Regarding your first query,Bracco appealed to the federal court in Feb 2020 and the Jubilant management guided then that it will take about one and half year for the outcome.As its duopoly market, Bracco maybe using litigation as a tool to hinder Jubilant… remember,U.S. International Trade Commission and USA patent office has already ruled in favour of Jubilant. Bracco has very slim chances now IMO. Jubilant increasing investment in Ruby Fill and they are launching it in Europe also…

Regarding second query, Radiopharmaceuticals is a niche business having good margin and stability whereas life sciences business is commoditised and cyclical… this maybe the reason for low pe…

Disclosure: Holding Dangerously high percentage of portfolio… views maybe biased…

4 Likes

Dear Orion

Thanks for an update!

Can you please respond to the following query too raised by Livog…

“What’s the current status of Demerger and how exactly it will benefit the existing shareholder by value unlocking?”

Disclo: Invested and was thinking of adding more at current level !

During recent concall, management indicated:

NCLT approval for demerger of pharma and LSI businesses has been

delayed due to lockdown. The company expects approval by October-

November 2020

Shareholding in the hive offed company will mirror existing one…

1 Like

Dear Orion

May I request you to make me understand

Post demerger, as a current share holder of Jubilant life science , what business I would be owning ? Is it Pharma or Life science ?

Thank you once again…as for the first time I would be facing Demerger issue in a stock I own…

For every 100 shares of existing Jubilant Life sciences, post demerger, you are entitled to 100 shares of Jubilant pharma and 100 shares of Jubilant life…

2 Likes

Today Jubilant Q1 2021 was to be announced…

Request if anyone can post the results!

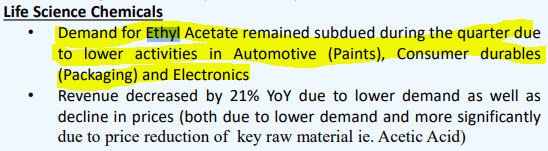

Ethyl Acetate : Leading producers & 7th largest global suppliers (IOLCP are having huge demand on line) since due to the affect of corona their profits have been hit due to this majorly. Post lockdown we could see markets opening up and demand rising - only way to find out is Q120

Remdesivir : Jubilant Generics Ltd entered into a non-exclusive licencing agreement with US-based Gilead Sciences Inc to manufacture and sell the potential COVID-19 drug Remdesivir in 127 countries, including India. : Gilead sign licensing deal for Remdesivir with three Indian companies - The Economic Times

ANDA USA : 63 Approved ANDA in USA

ANDA EUROPE : 33 Approved ANDA in Europe

ANDA CANADA : 23 Approved ANDA in Canada

Disc : Invested mainly due to covid story (remedisivir | radio pharma | API) & stock split

Interested space in Pharma - Life Sciences likely to keep well as its their backward integration

June 2020 :

Life Science Ingredients - (10%) YoY - Slight decline in Life science sector

Pharmaceuticals - 7% YoY

Drug Discovery & Development Solutions - 21% YoY

2 Likes

Jubilant life science seems to have a diversified portfolio… appears to be interesting

However, would be thankful if someone who is tracking closely this stock could clarify few issues,

From screener data , I find the past record has not been so good though it has started doing well last few quarters !

ROCE@ 10%, seems inferior than Granules and Aarti drug @ 17%, however expensive than Granules and Aarti drug …

Q1 , 2021 not yet declared… I searched BSE website … The company is yet to notify to BSE the date to declare Q12021 results …

Now it is a well known fact that since there is a celebrity who has picked up a 6% stake post Q4/2020 results, the share price went up substantially due to heavy buying by the celebrity and his followers…Now even before Q1 2021 results the share price is going up though there is no fresh triggers. Is it possible to find out if any insider is buying in bulk before result is declared…can we find out this data…

The small investors like you and me should not get trapped in the process of bulk buying…those people would exit at a profit and the share price falling thereafter…

Discl: Tracking position

3 Likes

Yes, you are right…we should not give much weightage to celebrity buying or selling…rather than should

bouild own conviction…anyways,the said celebrity holding jubilant since 2016-17(AR 16-17 his holding 27.5 lac shares).

Regarding valuation, portfolio of jubilant is vastly different than others…nuclear/radiopharma with second largest radiopharmacy network in North America is something unique…anyways this kind of valuation is 1/2 month phenomenon due to rwecent rally…maybe demerger is the driver…

3 Likes

National Company Law Tribunal approved the proposed Composite Scheme of Arrangement with the requisite majority…

1 Like

Jubilant Life Sciences presents 1,000 vials of remdesivir to UP CM Yogi Adityanath…

CSR activity…It would also enhance brand value

2 Likes

Jubilant life AR:

#Pharmaceuticals segment, which reported EBITDA of ` 15,555 million, a growth of 13% YoY with a margin of 27.2%. The Pharmaceuticals segment accounted for 78% of the overall EBITDA for the Company during the year.

#Life Science Ingredients reported EBITDA of ` 4,310 million translating to EBITDA margin of 13.6%.

#Discovery & Development Solutions segment EBITDA was at ` 734 million translating to EBITDA margin of 28.1%.

#We are the third largest player in the nuclear medicine industry and the leading player in the US based on market share of certain products, namely, MAA and DTPA.

#We believe we are well-positioned in the high-value niche business of Radiopharmaceuticals, offering quality diagnostic imaging and therapeutic radiopharmaceutical products. We specialise in lung, thyroid, bone and cardiac imaging products as well as thyroid disease therapy

#For diagnostics, our key products include MAA and DTPA, for both of which we have leadership position in the US. For therapeutics, our key products include Iodine-131 (‘I-131’), of which we are one of only three US FDA approved manufacturers globally.

#We are the second largest centralised commercial radiopharmacy network partner in the United States with over 50 radiopharmacies across 22 states.

#We are the second largest player in the allergenic extract market in the United States and are currently the sole producer and supplier of venom products for the treatment of allergies in the United States.

#Contract Manufacturing of Sterile Injectables and Non-Sterile Produc: We serve seven of the top 20 pharmaceutical companies globally.

#Active Pharmaceutical Ingredients (APIs ): We develop and produce APIs in the therapeutic areas of the Cardiovascular System (CVS), Central Nervous System (CNS), Gastrointestinal (GI), Anti-infectives and Anti-depressants. We have forward integration with our Solid Dosage Formulations business line.

#Solid Dosage Formulation : We believe we have a strong product portfolio and are currently leaders in the US for Prochlorperazine, Methylprednisolone and Terazosin and we rank among the top three in the US for a few other products. We focus primarily on the manufacture and sale of solid dosage formulations for Cardiovascular System (CVS), Central Nervous System (CNS), Gastrointestinal (GI) and Anti-allergy therapeutic categories.

#Over 70% of our assets are based in North America. This includes our four manufacturing facilities (CMO Spokane facility, CMO Montreal facility, radiopharmaceuticals Montreal facility and Solid Dosage Formulations Salisbury facility), our network of over 50 Radiopharmacies in North America and our highly differentiated Allergy Therapy Products business backed by one of the oldest and most trusted brands in the US.

#Diverse sources of revenue with a de-risked business model: : As on 31st March, 2020, we had a diversified product portfolio including diagnostic and therapeutic radiopharmaceuticals, a broad range of sterile injectables and non-sterile products, over 200 different allergens and standard allergy vaccine mixtures, 56 commercialised generic solid dosage formulations and 44 commercialised APIs sold across markets globally. As a result of our diversified product portfolio, we benefit from diversified revenues between three differentiated businesses.

#top 10 customers (excluding GPOs but including customers purchasing goods and services through such GPOs) contributing 31% to the total Pharma revenues as on 31st March, 2020.

Strong product pipeline : Our Radiopharmaceuticals business line is in the process of developing certain products such as I-131 meta-Iodobenzylguanidine (‘mIBG’) for which we plan to make a New Drug Application (‘NDA’) filing.

In addition, we have seven other products in different stages of development for which we may consider making 505(b) (2) filings.

USFDA Inspection: The Nanjangud plant was a coinspection by US FDA and Health Canada. During this financial year, Health Canada removed the OAI classification for the Nanjangud plant and we expect favourable resolution from the US FDA as well. Regarding the Roorkee facility, we have submitted comprehensive responses to the US FDA and have completed remediation activities by consulting with third party consultants and are hopeful of clearance from US FDA once they re-inspect the plant.

Life Science Ingredients (LSI): The Company is a global leader in Pyridine and its derivatives (Speciality Ingredients), Vitamin B3, Acetic Anhydride and Ethyl Acetate.

We are the world’s largest producer of Bio-based Acetaldehyde.

Nutritional Produc: One of our key products in this segment is Vitamin B3 (Niacinamide and Niacin) for which we hold a global leadership position. Our Vitamin B3 is fully backward integrated with feedstock raw material (i.e. Beta Picoline and 3-Cyanopyridine) which is produced by our Specialty Intermediates business as a by-product.

#We are the market leader in India and globally #4 in Acetic Anhydride merchant market.

#we have become one of the largest Ethanol supplier to Oil Marketing Companies (OMCs) among standalone distilleries. Moreover, a price increase based on Government’s new policy has improved our business margins.

Disc.:Invested.

7 Likes

hi orion

nice to see ur msg on jubiliant. I m heavily invested in jubiliant n ready to wait till at least 5 years. whats ur view on AGM n result in early September

Hi,

AGM’s are routine procedure,involving passing of resolutions with chance for participants to interact with management.Good thing is that AGM is through video conferencing and you can join and interact with management.You have to send them questionnaire 5 days before AGM date.Details are provided

in the notice below:

As far as quarterly results are concerned they have never been consistent…upto ebitda they were great but there were n number of one offs every quarter leading to volatile bottom line.Latest quarter was exception and hope they have cleaned the mess completely.

What will be interesting to watch for is radio/nuclear pharma growth and margin,Ruby Fill expansion,

DDS and CDMO business and demerger timeline.

thanks dear orion for ur reply.i just wanted to know whether demerger can happen at agm. also I think they have 3000 cr net debt n having cash of 2300 cr on books. don’t u think at conservative eps of 60+ this is cheap?? Also can u tell me impact od antidumping duty of vit.b4/ choline chloride on sells of company??

r u positive on long term in script??. thanks in advance.