Many one off this quarter…topline is okay but IFC loan settlement charges of 234 Cr alongwith product recall charges ,legal battle fees(Bracco filed patent infringement suit for RUBY FILL, Co.'s one of the most coveted product) and adverse product mix in radiopharma business dent the margin.Also,they have appointed 3rd party consultant for USFDA remediation process which too affected this quarter profitability…Margin crashed to 15 from 20%.

Concall guided though most of the one off charged in Q4,

still some remains for Q1.

Lower acetic acid prices led to higher supplies in the market, which impacted profitability.Prices dropped from 600 USD to around 450 USD.

Co. guided normalised margin for next year but lot depend on USFDA resolution and Ruby Fill suit.

RUBY FILL SUIT STATUS:

On 6th March 2019 co. filed final Offering Memorandum with Singapore stock exchange related to Issuance of rated unsecured bonds of US$200 million. Extract of this document mentions:

“These design changes

have been introduced into the USITC proceeding. On February 8, 2019, the ALJ entered an order that the

currently approved RUBY system infringes the three patents, but that the new redesigned RUBY systems do not

infringe any of the three patents. The ALJ’s order concerning these issues is subject to review by the full

Commission of the USITC. The ALJ has not yet ruled on our other defenses in the action, which will be

presented at the upcoming evidentiary hearing. The final USITC decision is expected in or around November

2019.”

What is important is ALJ assertion that redesigned product doesn’t infringe the patent…offsourse all this process will take time and concall guided q4 of this FY for the final verdict on this suit.

So all these headwinds affecting the stock price and don’t see early resolution either of the issue…will watch closely all these moving levers and take decesion accordingly.

Disclosure: Invested large part of the portfolio.

Seeking opinions from more experienced members.

-

The stock has corrected by over 40%. Generally this happens in commodities or cases of serious issues like Fraud etc… The current price is ~30 month low, not just 52 week. Not sure how to analyse the same technically. If it is a case of liquidity.

-

The issues highlighted in the con-call was apart from one off IFC convertible loan settlement, acetic acid price drop. The Ruby Fill patent issue is been around for 1 year. At 7500 Cr market cap, the stock seems to be trading at < 10x FY 20 Earnings.

-

The employee trust sold off significant shares ( 250 Cr) at a price of 780. This was highlighted in the forum earlier as well.

Please help understand if there are further serious issues/red flags which I am missing here.

1.Fraud: Difficult to draw conclusion just because price correction…IPCA Labs also corrected more than 50% few years back due to USFDA issue…remember it took 2/3 years to resolve the issue and to crawl back to current price.

Remember they have also Jubilant Foodworks which has given fantastic returns.

2.Along with IFC and Acetic acid price drop, there was issue of IPO fees,legal fees,USFDA resolution expences,adverse product mix in radiopharma business,product recall expences etc. the management mentioned.

Ruby-fill:Legal battle final outcome expected in q4 current FY.(Con-call extract)

3.Employee Trust sell off: It was mandatory before 31 march 2019.Only

concern is share price rose to 900/- just before sell off and crashed afterward.

USFDA,Ruby-fill,Acetic acid price will have bearing on the price apart from anything else.

The first voice of heart after reading concall was promoters are less investor friendly and they are just using market as self rewarding tool periodically so game over

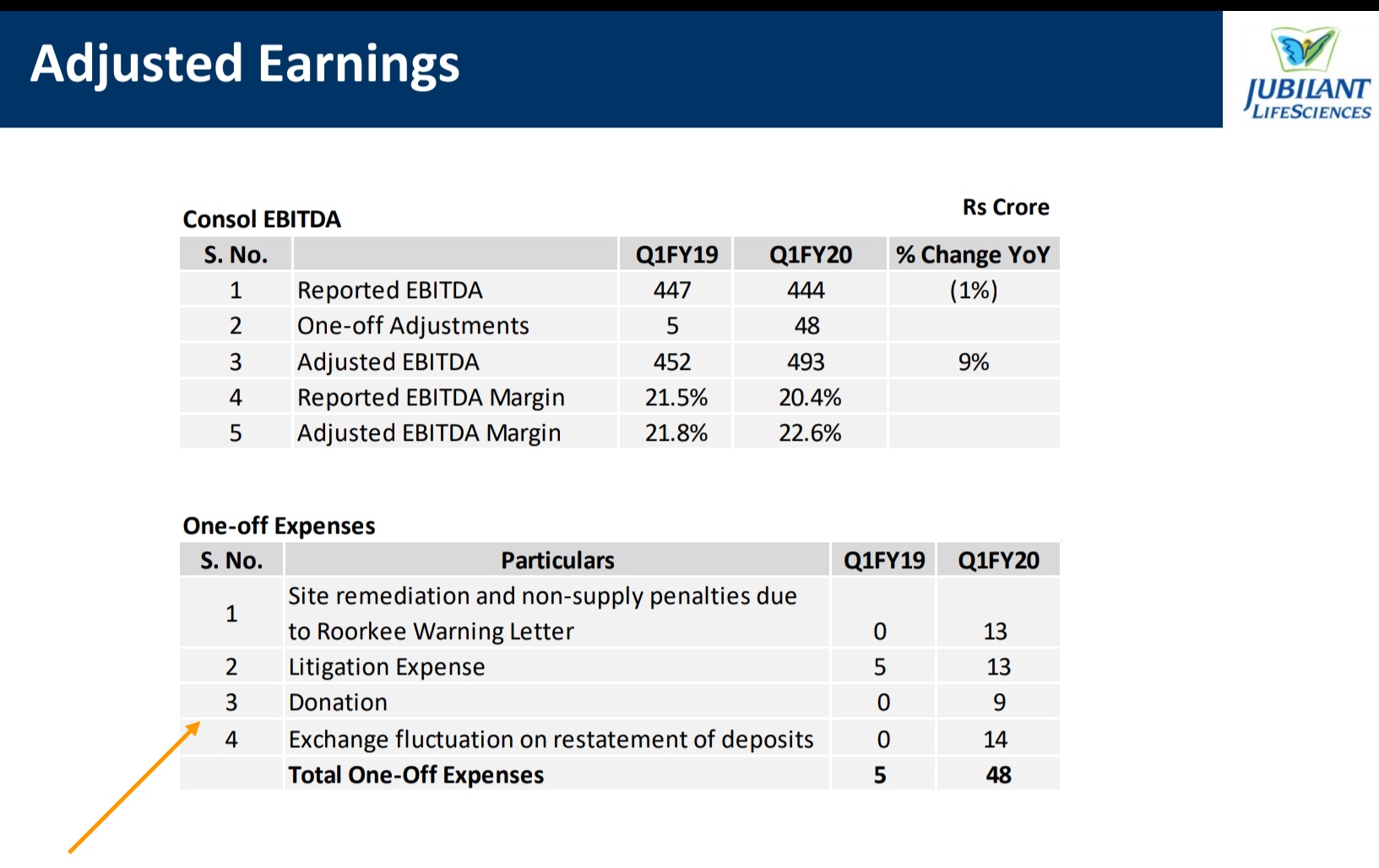

Q1-FY20 Results:

Pharmaceutical segment revenues have been higher by 12% YoY led by growth in CMO, Radiopharma and Allergy Therapy Products businesses. Pharma segment EBITDA was 3% lower YoY with higher profitability in CMO, Allergy and Generic businesses offset by lower API volumes and one-off expenses. Adjusted for the one-off expenses, Pharma EBITDA was higher YoY.

In Life Science Ingredients segment, revenues have been 5% YoY lower mainly due to decline in input

prices that affected selling prices in the Life Science Chemicals business. Profitability improved due to

volume and value increase in Specialty Intermediates and Nutritional Product businesses.

Is it par of mandatory CSR activity?Not sure…Key positive is 196Cr debt reduction this quarter and Received CE certificate allowing Ruby-Fill® to be introduced

in the EU market. Price erosion is LSI business arrested.Effect of demerger exercise difficult to guage at this stage…Ruby Fill litigation and USFDA both hangover on the price and management guided to resolve both at the end of this FY.

Discl.: Sold 10% holding around 500/- as crash in the market emerged with many opportunities elsewhere.

Rakesh Jhunjhunwala’s Rare Enterprises buys 1% stake in Jubilant Life.

Rare Enterprises acquired 2,013,626 shares of the pharma firm at Rs 436.23 per share and sold 263,626 shares at Rs 435.75 per share. Therefore, the net acquisition of Rare Enterprises is 17.5 lakh shares representing 1.098 percent of total paid-up equity.

Rakesh Radheshyam Jhunjhunwala already held 1.90 percent stake in Jubilant, as per the shareholding pattern of June 2019.

East Bridge Capital Master Fund also increased its stake in the company by acquiring 1,250,000 shares at Rs 435 per share.

The above acquisition of shares is on top of 4.63 percent stake already held by East Bridge Capital in the company as of June 2019.

Big positive in USITC case regarding Ruby Fill patent infringement court ruled No Violation.https://www.docketalarm.com/cases/International_Trade_Commission/337-1110/Certain_Strontium-Rubidium_Radioisotope_Infusion_Systems_and_Components_Thereof_Including_Generators/

Public Interest Statement of Venkatesh L. Murthy,Howard C. Lewin,James Ballow & April Mann(All renowned cardiologist and nuclear medicine

physician with experience of more than 20 years) Gave following testimonials before United States International Trade Commission which says:

If the RUBY is excluded from the market, public health would be negatively affected

because we would have to revert back to the 30-year old Model 510, which does not allow for

customized dosing or computer monitoring and control. The ALJ recommended that any

exclusion order be delayed at least 12 months. While I disagree that an exclusion order should

issue, if the Commission decides to issue an exclusion order, I agree with this delay because,

based upon the time required to establish new supply contracts and train staff, it would likely

take 6-12 months to revert back to the Model 51 O.

I hope Jubilant is on solid footing in legal battle with Bracco.

Discl.: Invested.

Finally, Jubilant won legal battle with Bracco…https://www.usitc.gov/secretary/fed_reg_notices/337/337_1110_notice12022019sgl.pdf

Any updates on Jubilant ?

Q3 Concall Extract:

Participents:

Nomura,Nirmal Bang,Motilal Oswal,Allegro,HDFC Asset Management,Fortune Financial,Macquarie,Elixir etc.

Q3 Sales flat… Pharmaceuticals business revenues and EBITDA higher by 2% and 6% YoY respectively.Pharmacy(Triad) business still bleeding though management didn’t

quantify the actual loss and hope to turn profitable next year,its strategic acquisition

and have ready distribution network, will launch new product in near future,currently 13 products and 8 at different stages of development.Ruby Fill:since we launched this product 2 years ago, we started, of course, with a small base. So YoY, we are growing this business almost in the range of 2-3 times. And even the same was the trend in the last quarter also.

Ruby Fill Litigation: Both administrative judge and full bench commission ruled in favour of the company but Bracco has taken a decision to file an appeal against that in Federal Circuit in Washington. There, the case will go on for another about 1.5 years.

On the contrary LSI business has shown mixed performance during the quarter. Revenues and EBITDA are lower 11% and 21% YoY but are higher by 6% and 10% QoQ respectively.Life Science Chemical business’ revenue was lower by 30% YoY with demand in acetyls affected by significantly lower input prices of Acetic Acid and Ethanol business affected by substantially higher molasses prices.

USDFA Status:

Nanjangud : this was a concurrent inspection by US FDA as well as Health Canada. And they issued an OAI. We immediately got engaged with them with all the corrective and preventive actions. We feel that authorities were satisfied with that. And because of that, they did not accelerate OAI status. So we still remain engaged with the authorities. In the last quarter, TGA Australia inspected this plant who have a mutual collaboration with Health Canada. And TGA Australia went back very satisfied, in fact they issued us A1 GMP rating. So, we feel that the plant is out of the trouble. We are now expecting Health Canada and US FDA either to take a decision or maybe USFDA can come for the inspection. And we are hopeful that we will be able to convert OAI into Voluntary Action post that inspection.

Roorkee: it is not under OAI, it is under warning letter. So USFDA inspected the plant last quarter. And that was a regular as per scheduled inspection, and they have looked at our remediation plans. They have reviewed that. They issued six observations. However, we don’t see that they are the critical ones. We have already given very detailed corrective preventive action plans on the six of the observations, and we are awaiting to hear from FDA as of now. But the kind of remediation plans we have put in place, we feel that as and when FDA will come for the inspection again anytime, this plant should also be out of the water.

Profit impacted by exceptional item(exceptional is regular feature for Jubilant it seems)…total 35 odd Cr…23 Cr charges for early redemption of 100 Million senior notes and 11 Cr for property,plant and equipment written off…

DEBT PROFILE:in the last 3 years, we have almost reduced 1800 crore of the total debt. So that way because last 2-2.5 years, there was a very strict control on capital expenditure. But now this year, because of the essential CAPEX which are required for either debottlenecking or growth plans.

Stock price is very volatile one can easily loose patience…also, stock has given negative return for last three years…

Coronavirus cluster in Karnataka and Jubilent life

Jubilant Life Sciences Limited enters into Licensing Agreement with Gilead for Remdesivir, a potential therapy for Covid-19

Disc - invested

results released by the company

After so many quarters good result because there was no negative surprise…no penalty,debt prepayment fee,no assets write off etc. and lower legal fee.Management sounded a bit of confident too.

Jubilant Concall brief :

- Judicious capex this year due to covid 19 scenario…last year capex 520 Cr.

*Ruby-Fill commercial launch in Europe planned in FY21

- Net debt lower by Rs 514 Crore during FY20

*Debt equity ratio 0.71

- Interest service coverage ratio 3.09

*Rakesh Jhunjhunwala asked why dividend payout ratio only about 10% and why company holding so much cash of around 1200 Cr…management reasoned demerger,debt obligation…reducing debt is priority the management said but no clear picture how much reduction…said the cash is in US and is against foreign bond debt.

*Company signed Licensing Agreement with Gilead Sciences to register, manufacture and sell Gilead’s investigational drug, remdesivir, a potential therapy

for Covid-19 in 127 countries including India, and is working towards launching the drug in July 2020.

*Health Canada converted OAI status of Nanjangud plant to GMP

compliant status.

- Company working diligently with US FDA regarding

resolution of the OAI status in Nanjangud.

*CMO Business: robust outlook due to strong order book,Initiatives taken to increase total capacity by over 30% with annual

potential revenues of around USD 30 million

*Good traction in Drug Discovery & Development Solutions (DDDS) segmant…Q4 YoY revenue up 85 Cr from 68 Cr and ebita 30Cr from 13 Cr.

*Hedging policy: foreign debt and foreign revenue provides natural hedge.

Disc.: Invested,views maybe biased,misinterpretation.

Disclosure of Rakesh Jhunjhunwala as per SEBI guidelines if holding exceeds 5% or more. Wife of RK acquired 600800 shares yesterday.

Hi, are Indian companies allowed to hold cash in $ outside India? Aren’t they supposed to convert this back to INR by the end of the month?

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=7483&Mode=0