Can somebody please explain how much is the risk that Jubilant’s master franchise agreement is not extended beyond 2024. This risk is not even mentioned in the credit ratings of Jubilant

It is mentioned in their DHRP. But, it won’t happen unless the case is as serious as McDonald vs Vikram Bakshi. A Nationwide franchisee like Jubilant Foodworks enjoys various advantages like know-how of local market (taste buds, supply chain etc.), and they’ve been top-notch in execution so far.

With dine-ins closed delivery is also limited…also limited menu on offer in their app

This is a good move by Jubilant, to deploy delivery staff profitably. Just like the foray into Chinese, this opens up a whole new revenue stream for the company even in normal times . Demand for pizza delivery is not uniform throughout the day, with peak hours mainly in the evening / Fridays to Sundays. At times when the load is low, delivery boys can be deployed for other tasks like these. What appears as an expense in the P &L becomes an asset for the company.

1 Like

News like these will be bad for QSR home delivery industry

Anybody tracking the qsr space ? How had it impact on their operation in the lockdown period and post lockdown , won’t they be the first one to come out of the crisis and see traction in terms of business stabilizing. Also apart from jubilant foodworks , what are the plays that one can play in this segment ?

one is Westlife Development . Is someone tracking this one also ? Why does Jubilant Foodworks has better roce ? Which one is the better business and on what basis ? Also what price should one pay for these kind of business ?New to the community , if some question seems trivial please forgive. @hitesh2710 @desaidhwanil @ashwinidamani

1 Like

The story behind the new ad campaign:

1 Like

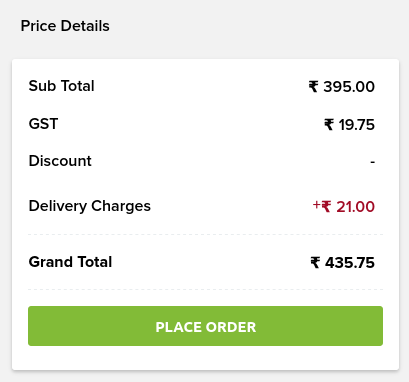

A business news channel reported this morning that Domino’s Pizza is going to start charging somewhere around 20-35 rs for delivery.

Showing 21 rs delivery charges for my nearest store:

They are doing ir from last 2 months in my town

I see. I am assuming they started it on experimental basis in few cities and based on the response they are now doing the same for a larger number of cities.

This move may provide a certain aspect of stability to the operating margins of the company

Jubilant FoodWorks has entered the Rs 500 crore ready-to-cook segment with the launch of its new brand ‘ChefBoss’. It will have a range of sauces and pastes that includes eight different products across two types of cuisines – Indian and Chinese. The products within the Indian cuisine range include Hyderabadi Biryani paste, Lucknowi Biryani paste, Makhani gravy and Bhuna gravy. On the other hand, products in the Chinese cuisine range include Manchurian cooking sauce, Schezwan cooking sauce, Hot Garlic cooking sauce and Honey Chilli stir fry sauce and dip.

.

All these products are easy to make and need two to three steps and take anywhere between 5-15 minutes. Consumers only have to add vegetables, paneer, or chicken at the end. These packs come in sizes of 150gm to 200gm and competitively priced between Rs.75 to Rs. 100 per pack.

.

As per the company’s press release, ChefBoss products will initially be exclusively available for consumers across e-commerce portals. The online sale of products will shortly start with Amazon (National), Flipkart Supermart (NCR, Mumbai and Bangalore) and Milkbasket (NCR).

“This brand is based on our sound understanding of the Indian consumers’ taste preferences and our commitment to provide the best quality products.”

4 Likes

*Jubilant Foodworks Q1FY21 Conference call key takeaways

- Store Guidance: Will close 105 stores this year (closed 5 in the quarter)/approx. 66% sales through dine in and balance through delivery in these stores/Almost half of these stores were mall stores and stores in techparks/ company will open stores with more capabilities for delivery and takeaway and smaller in size/will open 100 stores (net store additions will be (-)5)

- Delivery Charge: was implemented for the first time/started with Rs. 20 per order and subsequently increased it to Rs. 30/company believes delivery charge has become a norm in current times and thus believes the charge to be sustainable/Value for money offers did not suffer due to the charge and in fact witnessed growth

- International Market: Sri Lanka (22 stores) saw 80% revenue recoveries & Bangladesh (4 stores) saw 58% revenue recoveries in Q1FY21/ Company has guided for 5 store additions each in the two geographies

- Employee Costs: have moved to a “Flexi timing” system where in pay is dependent on the time of attendance at work. This has helped company reduce employee costs by 18.7% YoY and benefits will continue to accrue

- Raw Material costs saw a reduction in the quarter on a YoY basis on back of lower key material prices/company sees this to continue going forward

- rent waivers: have received Rs. 294mn in the quarter/ negotiations for wavier or reductions for coming quarters is still going on

4 Likes

Any idea what is the corresponding figure at the company level? Pre-covid, what was the proportion of sales through dine-in Vs. delivery?

2 Likes

Since our regulators are prone to copy-paste what happens in the west, this may come to India as well one day:

1 Like

You never know.

I remember Kerala had imposed around 14% of ‘Fat Tax’ on pizzas, burgers, and junk food back in 2016. Not sure if it still there or they discontinued it.

In the recent FY21 Q1 concall of the company, Mr.Hari Bhartia said we see a possibility of growth to 3000 stores.

But in the analyst presentation of Domino’s Pizza Inc. USA, the company says they see India potential store count at 1800. How to reconcile this.

https://ir.dominos.com/static-files/c6d4f683-a02a-4cb9-a234-6d44eabc1b37

1 Like

I think the 3,000 number is a future potential count, while 1,800 is the current potential.

First Hong’s Kitchen to position itself in the white space offered between unorganized sector and Mainland China type of restaurants and now the entry into the Biryani segment

2 Likes

Dominos launches “The Unthinkable Pizza” plant protein based chicken pizza

1 Like