Revenue of the company was up 10 percent at Rs 949.1 crore against Rs 863.2 crore.

EBITDA for Q1 FY20 stood at Rs219cr, at 23.3% of revenue.

Net profit was down 0.9 percent at Rs 71.5 crore against Rs 72.1 crore in the same quarter last fiscal.

Same store sales growth (SSG) for the quarter stood at 4.1 percent.

Like for Like Sales growth, i.e., sales growth of stores that were not split since 1st April, 2018 came in higher at 5.8%.

Opened 26 new Domino’s stores during the quarter, taking the total store count up to 1,249 across 276 cities.

Advertising and promotional spends increased significantly, as also continued investments in technology.

“We have started the year on an encouraging note. Domino’s has been a very strong brand franchise and our strategic focus remains in brand building and innovation through high quality products, continued value for money, improved customer experience and an omnipresent network. Our recent launch in Bangladesh and our entry in Chinese food category through Hong’s Kitchen have received overwhelming response from our customers and should be long term growth drivers in the future.”

– according to Shyam S. Bhartia, Chairman and Hari S. Bhartia, Co-Chairman, Jubilant FoodWorks

Given below are my notes and observations from the Annual Report of the company for FY2018-19. Please note this is not a formal research note on the stock but just a collection of a few points which I felt were noteworthy to be paid attention to:

It was good year for the company with strong sales and profit growth, expansion of the breadth & depth of offerings and geographical expansion. Main highlights of the year include launch of Hong’s Kitchen, entry into Bangladesh, Dunkin Donuts achieving break even and doubling of dividend.

Sales growth was decent. SSSG for the Domino’s pizza was 16.4%, claims the company.

Sales break up (Rs. Crs.)

FY19

% to total

FY18

% to total

YoY %

Pizza

2,736.77

77.51%

2,334.31

78.32%

17.24%

Other manufactured

534.60

15.14%

383.13

12.85%

39.54%

Beverages, Dips, Desserts etc.

253.42

262.34

-3.40%

Other operating Income

5.88

0.66

Total

3,530.67

2,980.44

18.46%

Cheese is the most important Raw Material consumed constituting 40% of the total RM cost (42% last year) of Rs.785 crores.

Company’s physical reach has increased further, with total number of stores now crossing 1200:

Physical reach

FY19

FY18

Cities

273

266

Restaurants

1259

1171

Out of this, Domino’s

1227

1134

Dunkin Donuts

31

37

Hong’s Kitchen

1

0

Commissaries

8

11

Company has two subsidiaries – one in Sri Lanka and one in Bangladesh. Sizes of the subsidiaries are currently insignificant compared to the parent.

Rs. Crores

Standalone

Consolidated

Standalone as % of Consol

Sales revenue

3,530.67

3,563.14

99.09%

PBT

494.48

489.67

100.98%

PAT

322.80

317.98

101.52%

CFO

433.88

425.65

101.93%

Receivables

32.68

27.44

119.13%

LT Debt

-

-

There are no guarantees / indemnities / letters of comfort issued on behalf of any subsidiary for which the parent would be liable. So my approach here would be to look at the Standalone statements primarily and then look at the subsidiaries separately vis-a-vis the amounts invested in them.

Company has invested Rs.92 crore in Sri Lanka (loss making 100% subsidiary), of which Rs.10 crore was invested in the current year. Revenue from Sri Lanka is just Rs.33 crore (100% subsidiary) from 22 restaurants Vs. 24 previous year. Rs.7.93 crore was written off as impairment during the year.

Bangladesh (51% subsidiary) became operational this year and earned is Rs.2 crore from 1 outlet. Rs.4.5 crore was invested in Bangladesh subsidiary this year. Bangladesh economy is doing well and grew 7.8% - its highest ever this year. So this foray holds potential.

During the year, increase in cash and liquid is around Rs.278 crore which is very healthy considering the PAT of Rs.322 crore, capex of Rs.Rs.167 crore and Dividend payout of Rs.40 crore. Conversion of PAT to cashflows is good. Cash balance has increased from Rs.391 crore to Rs.670 crore.

Cash and Liquid (Rs. Crs)

FY19

FY18

MF (Liquid & Bond Fund)

180.80

263.02

Cash & Bank balance

24.84

78.53

Bank FD

464.22

50.00

Total

669.85

391.54

Addition of Gross Block is Rs.161 crore and Disposal / transfer is Rs.42 crore. Last year also disposal was Rs.40 crore. Given its (disposals) recurring nature, this seems to be on the higher side to the overall scheme of things. Need more information on what exactly this pertains to.

There is plenty of litigation. No provision is made against the anti-profiteering case pending in the courts. Liability on this is Rs.41 crore as per the NAA order. There are also various other tax litigation totalling to around Rs.100 crore pending. Besides, 38 consumer cases are pending in courts against the company but here financial liability will be much smaller I think.

As per the Master Franchise Agreement with Domino’s and Dunkin Donuts, the company is committed to open a specified number of restaurants from time to time. But how many restaurants is not given. Dunkin’s is a 15-year contract. Not clear when it expires and what happens after that. No such information given for Domino’s.

Total number of employees was 28,286 as of 31-Mar-2019 against 27,539 last year. Employee cost was up 11% from Rs.604 crore to Rs.672 crore in FY19. Percentage increase in median remuneration of employees was 13.15% as against 8.25% last year. We can call this the Swiggy – Zomato effect.

Gratuity liability has doubled from Rs.2.2 crore in FY18 to Rs.5.65 crore in FY19. Though this is currently small in absolute terms, the company has a large employee base and this will increase exponentially in the long run as wages rise and more & more employees complete 5 years of service. (Note: Gratuity is paid @ 15 days last drawn salary for every year of completed service after completion of 5 years of service). If it doubles every year, where will it be in 10 years?

Company has ESOPs. However no fresh shares were issued under ESOP during the year. Options pending to be exercised at the end of the year were around 1.5 lacs, which is 0.1% potential dilution to the 13.20 crore shares issued. Not that high. Of these, 70% of the options have exercise price linked to market price but remaining are at Rs.10 per share.

Managerial remuneration, CEO salary and Director’s remuneration seem reasonable. Independent Directors are getting commission. Mr. Pota got Rs.1.5 crore as performance linked incentive which is okay.

Promoter stake was down from 45% to 42% during the year due to sale of 3% stake. There are also frequent pledging of shares. During the year, promoter attempted to impose a brand royalty but withdrew the proposal later. I think promoter is the biggest risk factor in this company.

Related Party Transactions exist but amounts are not very large. The largest is purchase of goods from a promoter owned company to the tune of Rs.31 crore (Rs.26 crore last year). The promoter is not taking any remuneration (salary, sitting fees, commission etc.) so I guess he must be making some money here.

What else? Among other things,

The company remains debt free.

Dividend has been doubled to Rs.5 per share from Rs.2.50 per share (Rs.5 pre-bonus) last year but there is potential to increase it even further. Free cash flows seem far beyond the capex needs.

Advertisement expenses grew faster than sales, up 20% to Rs.170 crore from Rs.142 crore from last year.

Company has foreign exchange exposure and spent Rs.107 crore for the year (Rs.85 crore last year). I think this is on account of some raw material imports (but not cheese, since expenditure on cheese is much higher).

Conclusion

No major negatives found. It was a good year for the company. The main risks seem to be regulatory cases and promoter quality. There is also a question mark over the Sri Lankan operation which is almost 10 year old but so far there is very little to show for it.

Company had shown a sharp improvement in the year FY17-18 and I had wondered whether this could be sustained or it was a one-off. The improvement seems to have sustained in FY18-19.

SSSG slowdown: Domino’s Pizza US facing a slowdown in same-store sale growth rates in the US.

DPZ SSSG at 3% in the US and 2.4% globally:

DPZ SSS lowest in 7 years:

Delivery: ET Prime’s article on delivery by Dominos via Zomato and Swiggy. http://bit.ly/2ZVL2TF

Important points:

Revenue share of delivery in F&B has gone up 3.5 times, most of this is via mobile.

SSSG for Domino’s has fallen globally and in India.

JUBLFOOD will partly morph into a tech company.

Domino’s doesn’t want to share customer data with Zomato/Swiggy, so only pays 3-5% to appear on the platforms, and manages delivery by itself.

Going to open stores near existing ones to reduce delivery time.

It still has a 72% market share in the organised pizza market.

Noteworthy: Domino’s delivery is active >90% of the time via Domino’s app, Swiggy and Zomato. This is not true for any other restaurant. They immediately stop taking orders when it starts raining, or when in-store traffic is high like weekends and holidays.

Average delivery time or Zomato on many restaurant’s deliveries has gone down to 30 minutes or less. Zomato sends a notification to the user when the delivery has been quick (<30 minutes). This takes away the appeal of the 30-minute delivery that Domino’s enjoyed or a long time.

Cloud Kitchen: Important points:

The business model isn’t as profitable in reality as it looks from the outside. Cloud kitchens alone won’t be able to compete with established restaurants. So there is a low chance of a single business scaling up and providing big competition to incumbents.

At best they will compete in small micro-markets. An entrepreneur is better off buying a franchise of an established player who has a cloud kitchen model within its business.

The chains having presence and experience in food delivery will benefit a lot by opening cloud kitchens in addition to existing restaurants.

Reference articles:

Litigations: (mentioned earlier by @Chandragupta) The pending anti-profiteering case and other tax litigations total to the liability of ₹141 Cr. As of 2019, 38 consumer cases are pending. Although settlements are less, this is concerning wrt to the brand image, especially when put together with promotor concerns.

Expenses: Mainly increased ad, tech, and new stores.

Promotor concerns: Reduction in stake by Jubilant Consumer Pvt Ltd., pledging, and the recent brand royalty proposal and subsequent withdrawal.

Demand and competition: Does the edge lie in the habits, taste or delivery? The ease of delivery can be taken away if delivery apps become sustainable. Does the overall experience of buying from Domino’s (taste + delivery) create enough stickiness to warrant repeat orders?

Inversion exercise: What if, finally after all these years, Pizza Hut can make progress in gaining market share due to help from Zomato/Swiggy? What if delivery and higher price were the only missing components in a future dominated by Pizza Hut? They already have experience in superior dine-in service, that combined with an evolving menu, and delivery taken care of, pricing is the only real difference between Domino’s and PH. So for example, does Domino’s cost-saving on store interiors help it more than PH is harmed by its extra expense for fine dining?

I was trying to gauge the size of opportunity for domino’s in India (Which is the main driver for Jubilant). Would like to have your inputs -

The scale of opportunity is a function of

Same store sales growth (SSSG) without destroying profitability

Number of profitable stores that could be opened up in the future

SSSG - To get a rough idea for reference, an average US domino’s makes about Rs 7 Cr ($1 million) annually. Based on 2019 AR, approx sales per Indian store are around Rs 2.9 Cr.

Note - US is a saturated market with a high demand compared to other international markets, plus the price of pizzas is almost double to that of India’s. Hence, there might not be much room for SSSG more than what inflation permits. Another way could be to compare the avg number of pizzas sold per store annually. (Yet to get data)

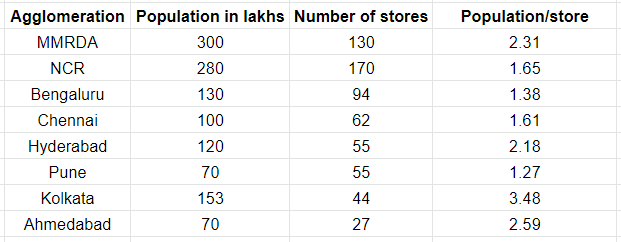

Number of new stores - Here, I have tried to see the current distribution of domino’s across the big cities.

I have tried to get the store density in lakhs/store. Please note -

Populations are a rough estimate and may not be accurate. I have tried to use at least two sources. Variability in actuals is highly possible.

NCR here consists of Delhi city, Noida, Gurgaon, Faridabad and Ghaziabad.

I have taken the store counts based on store locator on Domino’s website.

Looking at this, where there is a major IT hub, the density of stores is quite high.

I have tried to estimate the urban population where Domino’s might open up stores.

For the top 300 cities in 2011 (Population of at least more than 1 lakh), the total population came to around 20 Cr. Assuming the 2001 to 2011 urban growth rate, the population in these cities could be approx 26-30 cr (avg 2800 Lakhs) by 2021.

With a bullish consideration that on average, overall there would be 1 store for every 2 lakh population, the number of stores comes to around 2800/2 = 1400 stores (currently 1200).

Note-

Usually, even in lesser known cities where domino’s has a store, the population is almost always above 1 lakh. Except for touristy places like Shirdi or if that city is present on a major national highway, this has been true.

I have assumed the density factor of ‘2 lakh persons per store’ based on the assumption that the current average density factor in IT hubs is the upper limit that Domino’s could achieve in non-IT hubs in the future.

I have considered that Domino’s will be the dominant market player in QSR pizza segment and will have the current market share going forward. (Roughly the ratio for domino’s to pizza huts across Indian metros has been similar)

Sure the number 1400 is not accurate and has a lot of assumptions, but I don’t see a ‘5-10 times store growth possibility’ scenario. The Indian market seems fairly saturated as of now.

A side-note : I randomly searched for domino’s centres for lesser known cities (tier 3-4), many had 1k plus google reviews Maybe I am downplaying the popularity of Domino’s in upcoming cities, though I still don’t find sufficient room for growth.

Another input - Both Papa John’s and Domino’s have a franchisee-oriented model.

For the 5900 stores in US, only 400 are company-owned for Domino’s.

The revenue majorly consists of sales of raw material for the pizza, equipment and other operational necessities sold to the franchisees + approx 6%(for domestic) royalty fee on franchisee revenues.

The royalty fee revenue goes straight to the bottom line. Basically, this allows Domino’s to scale with a light asset model at the cost of earning lesser margins if it had owned all stores.

Currently as per my understanding Jubilant owns all India stores. Wonder if they would change that going forward for scalability. My guess is that they would not, as cashflows aren’t an issue and they have expanded without debt(while Domino’s US is troubled with it).

I have this company on a very preliminary tracker. Haven’t analyzed anything yet, and then the “royalty” incident really put me off. So I’ve ignored this company and there’s a good chance I’ll never pick it up.

But your comment was interesting. An asset-light model (US) runs into debt trouble, while the asset-heavy version (India) throws out cash! Seemed a little counter-intuitive on the surface. Why do you think this is happening? Is it simply reflective of the penetration and shift in preferences of these two markets - which overwhelms the asset-light / asset-heavy factor?

I don’t have much skill in understanding financials of foreign firms but regarding the debt part, maybe because the cost of capital is lesser and hence they are lenient in taking it.

In Domino’s USA case, they have negative equity since the last 10 years at least and they have still done recapitalization in 2015. As per my limited understanding, they are running a poor business.

Again as per my limited understanding, the most value in a brand franchise like domino’s is usually made at the consumer end, so if you are owning the entire value chain, it brings in wonderful cash flows. The trade-off is always that you initially need much more capital to scale but you can reap the cash flows later on after the break even ( 3 years for Domino’s India).

In the smaller towns, Zomato and Swiggy’s popularity is increasing compared to Dominos. However Dominos is still the leader albeit declining in popularity.

Some steps to counter the 3rd party aggregators thread by Dominos in India

Also read somewhere that they have doen away with Rs. 300 minimum order quantity but cant find the link. Anyways when i checked in my Dominos app didnt find anything like that.

3rd party aggregators currently offer…Anything. Anytime. Anywhere. Any amount.

while Dominos offers Pizza. Anytime.Anywhere.

Don’t see any problem of Domino’s from Zomato/Swiggy. Even if people install just one food delivery app, e.g. Zomato or Swiggy, then also people can order Domino’s. The threat can be from Pizza Hat and similar Pizza players should they also choose to use Zomato/Swiggy, if they haven’t already.

You may not see problem from Zomato/Swiggy but the company does.

Otherwise they won’t have

Go figure!

The larger point is that Swiggy/Zomato gives more culinary choice…in the past if people didnt felt like ordering food Dominos was the only option so it had to be pizza.

Now they can order anything under the sun…and even for pizza they have options other than Dominos

I don’t think there was a significant lot who used to order pizza reluctantly just because there was nothing else to order online, unless the order was needed in rush or in case of late night orders. Many Local restautants or takeaways used to have [still has] their own delivery persons [though delivered late] and the contact numbers of those restaurants were available via Justdial or Google. Delivery apps just made the later task easy and more versatile and thus those late night or rushed orders are no longer exclusive for Domino’s.

Now, that their rushed and late night deliveries are no longer exclusive, the order of pizza is now only been made by those who need a pizza. For those peoples, Domino’s is benefitted by their presence on ZOMATO/SWIGGY.

Pizza isn’t native to Indian taste bud and has been mostly a fashionable acquired taste. The earlier strong growth of Dominos was mainly due to low base, and now that their turnover has doubled in the last 5 years, they have to do something unique to maintain their growth rate on a higher base.

20 minutes delivery is one such steps by Domino’s India. They have been running pilots for quite long. [HDFC Sec reported this earlier this year.] Domino’s Australia already has 20 mins delivery promise.

This link is for Domino’s USA, but is relevant.

Here the brand and taste specific stickiness will help. But they will have to keep on their promotional activities.

2.8% YoY decline in Q2 consolidated profit at ₹73.4 cr due to one-time loss of ₹12.5 cr. Consolidated revenue grew 12.2% YoY to ₹998 cr. The one-time loss represented provision created against investments made by Jubilant FoodWorks Employee Provident Fund Trust in the corporate bonds of DHFL, Reliance Capital and IL&FS, and was fully provided for on account of prevailing uncertainties.

HDFC Sec Report

Healthy SSG Growth: SSG grew at 4.9% (exp 3.5%) while like-like SSG (adj. for splitting stores) stood at 6.5% (exp of 5%). Robust growth in delivery and price hikes (3-3.5%) compensated for dine-in pressure and slowdown in smaller towns.

Net revenues grew by 12% (vs. exp of 9.5%) as ex-SSG growth accelerated.

15 quarter high store expansion: In 2Q, JFL opened 40 stores with new store design. Management upgraded their store guidance to 120 stores in FY20 vs. 100 earlier.

Robust app downloads: App downloads grew at 101/17% YoY/QoQ (25mn app downloads) led by in-store activations, indicating its success in new customer acquisition despite competition from aggregators.

Gross Margin expanded by 67bps to 75.3% (vs. exp 75.8%) despite steep dairy inflation. PepsiCo deal, optimisation in promotions and price hikes supported margin expansion.

Employee costs grew by 16% (in-line) owing to min. wage hike, store expansion and investments in tech team.

Saw Dominos outlets in Chittorgarh (pop. 1.16 lacs) and Mount Abu (pop. 22.9 K)…Mount Abu sees a good influx of visitors from Gujarat over weekends. Didn’t visit any of the outlets but saw good crowd at the Mt. Abu outlet during dinner time.

Hi everyone. I was just curious as to how do people estimate future revenue for Jubilant Foodworks at the consolidated level. The company just discloses SSSG for Domino’s Pizza (and I believe this is just India Dominos and not Sri Lanka’s). The company does not disclose Dunkin Donuts revenue and given its past history, it may not disclose the same or Hong’s Kitchen’s revenue for a long time.

In this scenario, as the moving parts like DD, Hong’s Kitchen become bigger, how does one account for these in your future models? Domino’s India revenue for now should be 99% Jubilant’s standalone revenue. Sri Lanka revenue is disclosed annually as its a wholly owned subsidiary (and from this year every quarter’s performance can be derived by deducting standalone revenue from consolidated). Bangladesh performance would be a single line item at the Associate profit/loss level I assume.

Little Caesar’s Pizza - supposedly the third largest pizza chain in the world, after Pizza Hut & Domino’s - enters India:

Meanwhile, as per this report (citing unnamed officials), Jubilant is contemplating getting into Cloud Kitchens. Does anyone have any independent confirmation or denial on this? There was no talk of this in the concall atleast:

Key concall highlights

Addition of 47 stores in Q3FY20; Domino’s opened its third store in Bangladesh.

Hong’s Kitchen opened its second store in Delhi. Company now expects to open

140-150 new stores vs 120 planned earlier.

Dairy prices impacted gross margin negatively by 220bps.

Delivery mix, investments in digital, and marketing campaign have higher impact

on manufacturing and operating expenses.

Domino’s mobile ordering app download reached 4.1mn during the quarter.

The company is trying pilot with smaller size Dunkin Donut store with size of

~100 sq.ft.

Is this news report really true? When Hong’s Kitchen was launched, company made a formal intimation to the stock exchanges. Then why there is no such intimation now even though the outlet has already opened? On Google Maps, one can see there is indeed a restaurant Biryani’s of India at the mentioned address. A photo of the menu card is also there, with the phone number. I called it up yesterday but no one picked up. The number is listed as Domino’s Unity Mall on Truecaller. Jubilant website makes no mention of Biryani’s of India. So who owns it?